Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeFinRL: A Deep Reinforcement Learning Library for Automated Stock Trading in Quantitative Finance

Nov 19, 2020

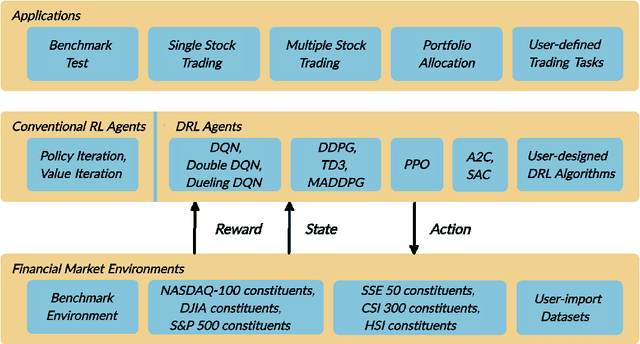

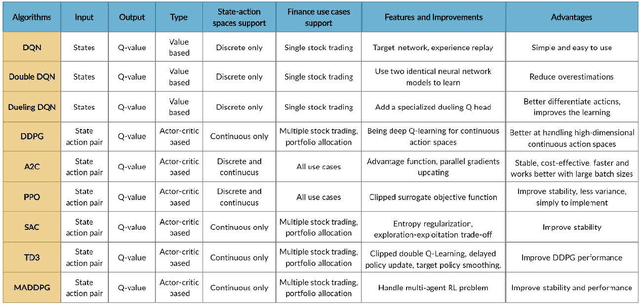

As deep reinforcement learning (DRL) has been recognized as an effective approach in quantitative finance, getting hands-on experiences is attractive to beginners. However, to train a practical DRL trading agent that decides where to trade, at what price, and what quantity involves error-prone and arduous development and debugging. In this paper, we introduce a DRL library FinRL that facilitates beginners to expose themselves to quantitative finance and to develop their own stock trading strategies. Along with easily-reproducible tutorials, FinRL library allows users to streamline their own developments and to compare with existing schemes easily. Within FinRL, virtual environments are configured with stock market datasets, trading agents are trained with neural networks, and extensive backtesting is analyzed via trading performance. Moreover, it incorporates important trading constraints such as transaction cost, market liquidity and the investor's degree of risk-aversion. FinRL is featured with completeness, hands-on tutorial and reproducibility that favors beginners: (i) at multiple levels of time granularity, FinRL simulates trading environments across various stock markets, including NASDAQ-100, DJIA, S&P 500, HSI, SSE 50, and CSI 300; (ii) organized in a layered architecture with modular structure, FinRL provides fine-tuned state-of-the-art DRL algorithms (DQN, DDPG, PPO, SAC, A2C, TD3, etc.), commonly-used reward functions and standard evaluation baselines to alleviate the debugging workloads and promote the reproducibility, and (iii) being highly extendable, FinRL reserves a complete set of user-import interfaces. Furthermore, we incorporated three application demonstrations, namely single stock trading, multiple stock trading, and portfolio allocation. The FinRL library will be available on Github at link https://github.com/AI4Finance-LLC/FinRL-Library.

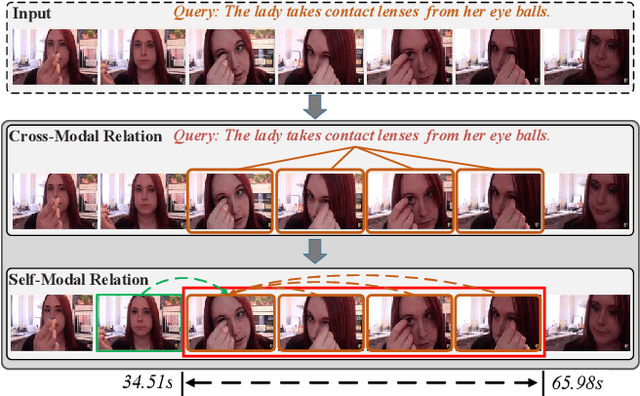

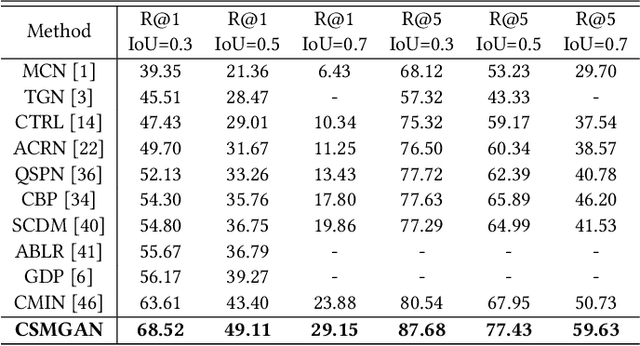

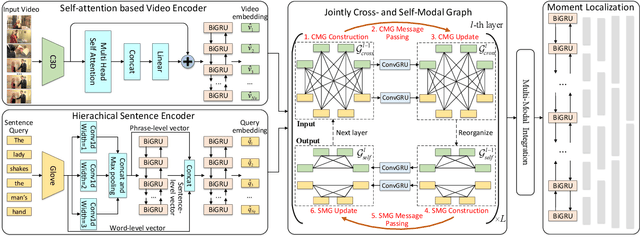

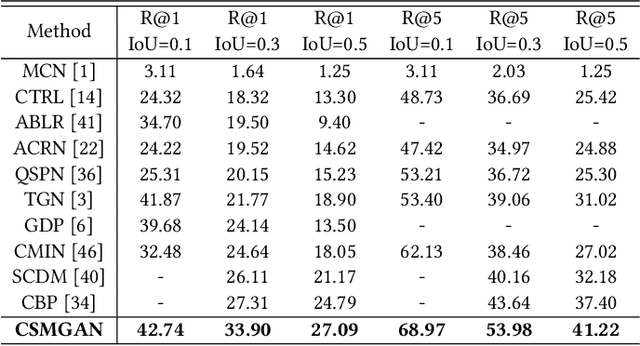

Jointly Cross- and Self-Modal Graph Attention Network for Query-Based Moment Localization

Aug 13, 2020

Query-based moment localization is a new task that localizes the best matched segment in an untrimmed video according to a given sentence query. In this localization task, one should pay more attention to thoroughly mine visual and linguistic information. To this end, we propose a novel Cross- and Self-Modal Graph Attention Network (CSMGAN) that recasts this task as a process of iterative messages passing over a joint graph. Specifically, the joint graph consists of Cross-Modal interaction Graph (CMG) and Self-Modal relation Graph (SMG), where frames and words are represented as nodes, and the relations between cross- and self-modal node pairs are described by an attention mechanism. Through parametric message passing, CMG highlights relevant instances across video and sentence, and then SMG models the pairwise relation inside each modality for frame (word) correlating. With multiple layers of such a joint graph, our CSMGAN is able to effectively capture high-order interactions between two modalities, thus enabling a further precise localization. Besides, to better comprehend the contextual details in the query, we develop a hierarchical sentence encoder to enhance the query understanding. Extensive experiments on four public datasets demonstrate the effectiveness of our proposed model, and GCSMAN significantly outperforms the state-of-the-arts.

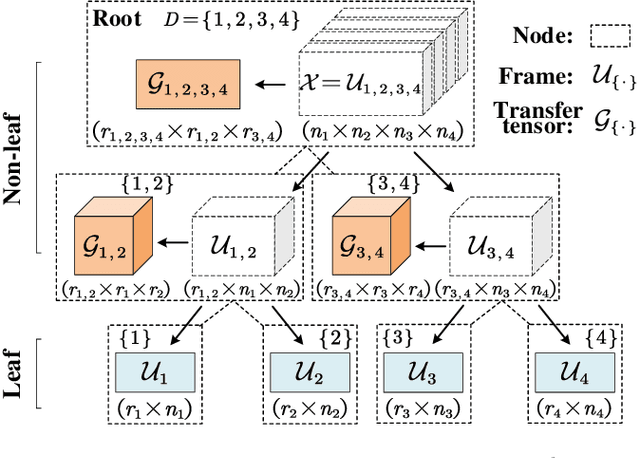

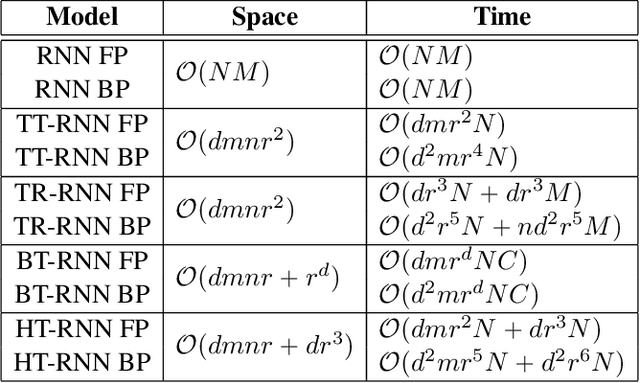

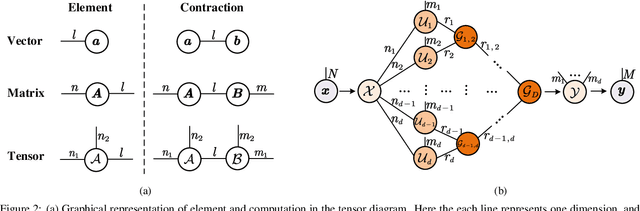

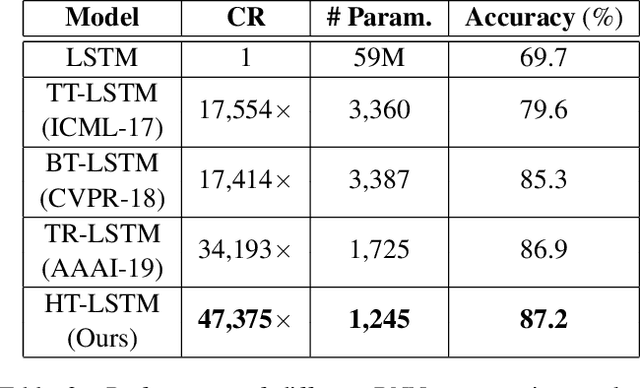

Compressing Recurrent Neural Networks Using Hierarchical Tucker Tensor Decomposition

May 09, 2020

Recurrent Neural Networks (RNNs) have been widely used in sequence analysis and modeling. However, when processing high-dimensional data, RNNs typically require very large model sizes, thereby bringing a series of deployment challenges. Although the state-of-the-art tensor decomposition approaches can provide good model compression performance, these existing methods are still suffering some inherent limitations, such as restricted representation capability and insufficient model complexity reduction. To overcome these limitations, in this paper we propose to develop compact RNN models using Hierarchical Tucker (HT) decomposition. HT decomposition brings strong hierarchical structure to the decomposed RNN models, which is very useful and important for enhancing the representation capability. Meanwhile, HT decomposition provides higher storage and computational cost reduction than the existing tensor decomposition approaches for RNN compression. Our experimental results show that, compared with the state-of-the-art compressed RNN models, such as TT-LSTM, TR-LSTM and BT-LSTM, our proposed HT-based LSTM (HT-LSTM), consistently achieves simultaneous and significant increases in both compression ratio and test accuracy on different datasets.

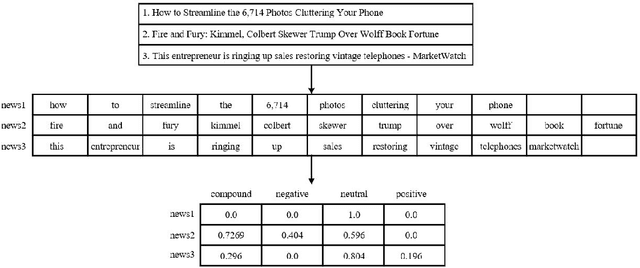

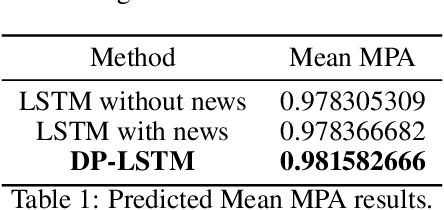

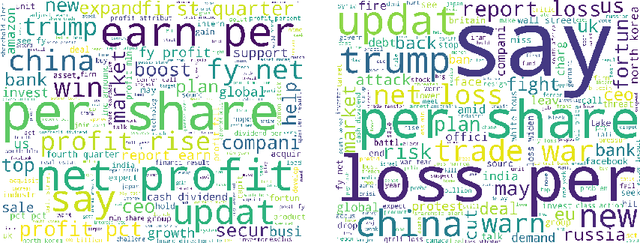

DP-LSTM: Differential Privacy-inspired LSTM for Stock Prediction Using Financial News

Dec 20, 2019

Stock price prediction is important for value investments in the stock market. In particular, short-term prediction that exploits financial news articles is promising in recent years. In this paper, we propose a novel deep neural network DP-LSTM for stock price prediction, which incorporates the news articles as hidden information and integrates difference news sources through the differential privacy mechanism. First, based on the autoregressive moving average model (ARMA), a sentiment-ARMA is formulated by taking into consideration the information of financial news articles in the model. Then, an LSTM-based deep neural network is designed, which consists of three components: LSTM, VADER model and differential privacy (DP) mechanism. The proposed DP-LSTM scheme can reduce prediction errors and increase the robustness. Extensive experiments on S&P 500 stocks show that (i) the proposed DP-LSTM achieves 0.32% improvement in mean MPA of prediction result, and (ii) for the prediction of the market index S&P 500, we achieve up to 65.79% improvement in MSE.

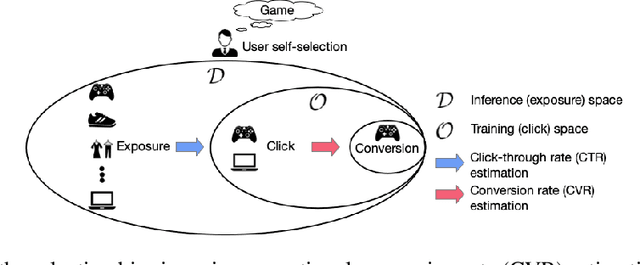

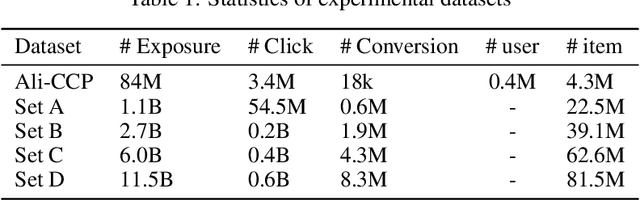

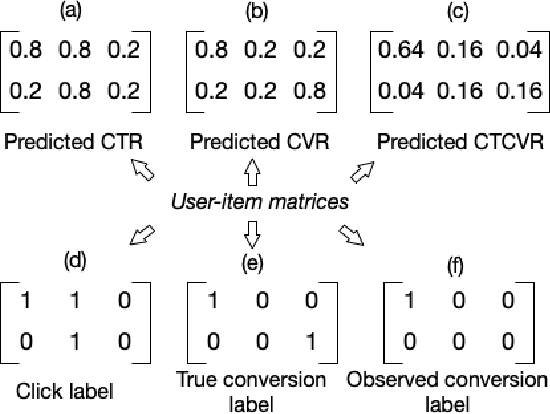

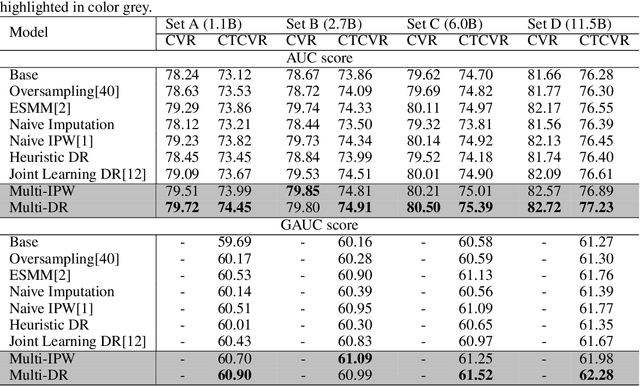

A Causal Perspective to Unbiased Conversion Rate Estimation on Data Missing Not at Random

Oct 16, 2019

In modern e-commerce and advertising recommender systems, ongoing research works attempt to optimize conversion rate (CVR) estimation, and increase the gross merchandise volume. Even though the state-of-the-art CVR estimators adopt deep learning methods, their model performances are still subject to sample selection bias and data sparsity issues. Conversion labels of exposed items in training dataset are typically missing not at random due to selection bias. Empirically, data sparsity issue causes the performance degradation of model with large parameter space. In this paper, we proposed two causal estimators combined with multi-task learning, and aim to solve sample selection bias (SSB) and data sparsity (DS) issues in conversion rate estimation. The proposed estimators adjust for the MNAR mechanism as if they are trained on a "do dataset" where users are forced to click on all exposed items. We evaluate the causal estimators with billion data samples. Experiment results demonstrate that the proposed CVR estimators outperform other state-of-the-art CVR estimators. In addition, empirical study shows that our methods are cost-effective with large scale dataset.

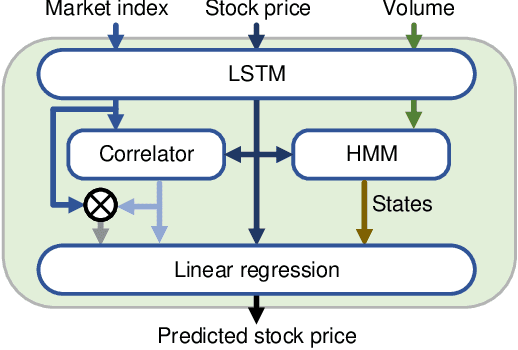

Risk Management via Anomaly Circumvent: Mnemonic Deep Learning for Midterm Stock Prediction

Aug 03, 2019

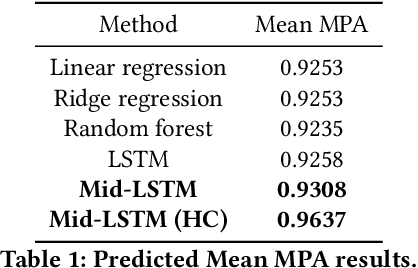

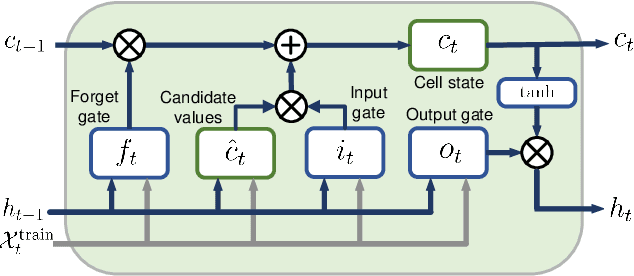

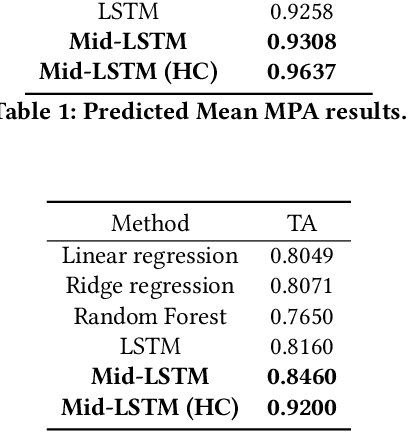

Midterm stock price prediction is crucial for value investments in the stock market. However, most deep learning models are essentially short-term and applying them to midterm predictions encounters large cumulative errors because they cannot avoid anomalies. In this paper, we propose a novel deep neural network Mid-LSTM for midterm stock prediction, which incorporates the market trend as hidden states. First, based on the autoregressive moving average model (ARMA), a midterm ARMA is formulated by taking into consideration both hidden states and the capital asset pricing model. Then, a midterm LSTM-based deep neural network is designed, which consists of three components: LSTM, hidden Markov model and linear regression networks. The proposed Mid-LSTM can avoid anomalies to reduce large prediction errors, and has good explanatory effects on the factors affecting stock prices. Extensive experiments on S&P 500 stocks show that (i) the proposed Mid-LSTM achieves 2-4% improvement in prediction accuracy, and (ii) in portfolio allocation investment, we achieve up to 120.16% annual return and 2.99 average Sharpe ratio.

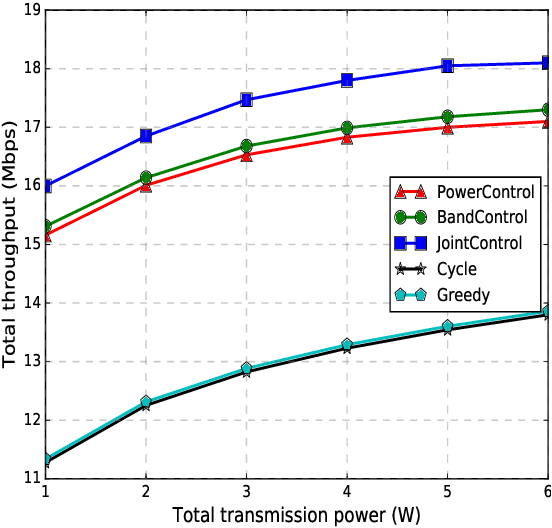

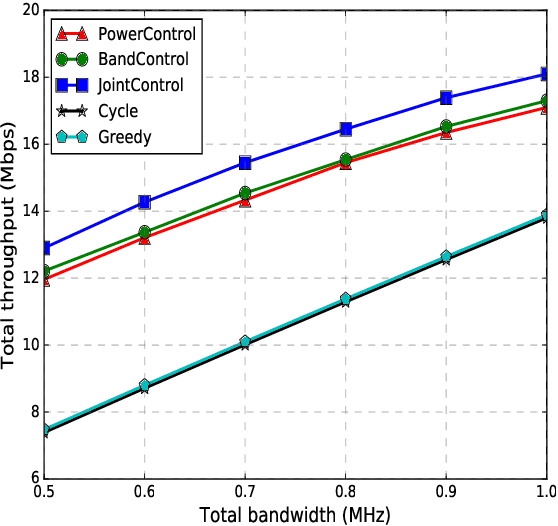

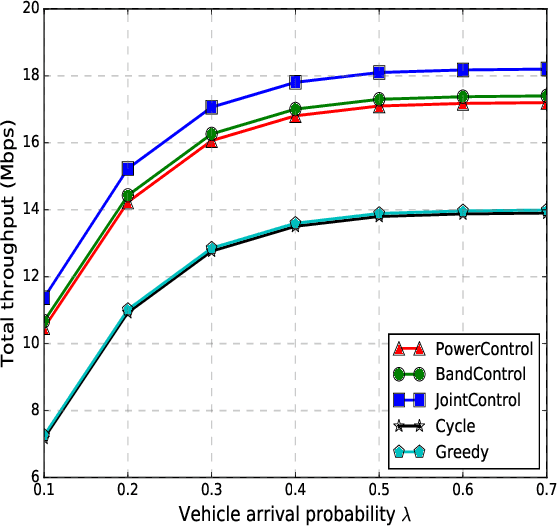

Deep Reinforcement Learning for Unmanned Aerial Vehicle-Assisted Vehicular Networks

Jul 27, 2019

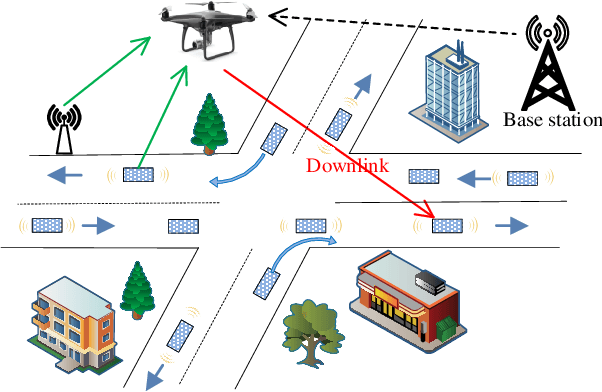

Unmanned aerial vehicles (UAVs) are envisioned to complement the 5G communication infrastructure in future smart cities. Hot spots easily appear in road intersections, where effective communication among vehicles is challenging. UAVs may serve as relays with the advantages of low price, easy deployment, line-of-sight links, and flexible mobility. In this paper, we study a UAV-assisted vehicular network where the UAV jointly adjusts its transmission power and bandwidth allocation under 3D flight to maximize the total throughput. First, we formulate a Markov Decision Process (MDP) problem by modeling the mobility of the UAV/vehicles and the state transitions. Secondly, we solve the target problem using a deep reinforcement learning method, namely, the deep deterministic policy gradient, and propose three solutions with different control objectives. Then we extend the proposed solutions by considering the energy consumption of 3D flight. Thirdly, in a simplified model with small state space and action space, we verify the optimality of proposed algorithms. Comparing with two baseline schemes, we demonstrate the effectiveness of proposed algorithms in a realistic model.

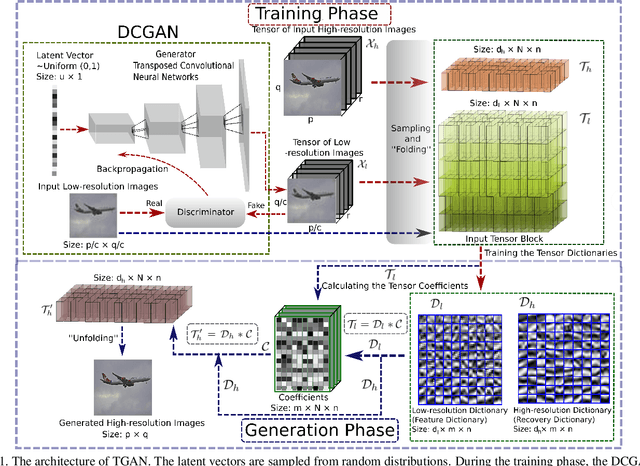

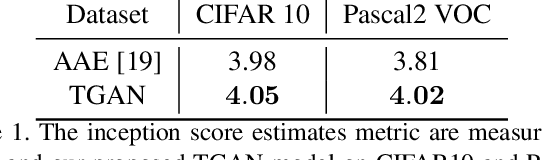

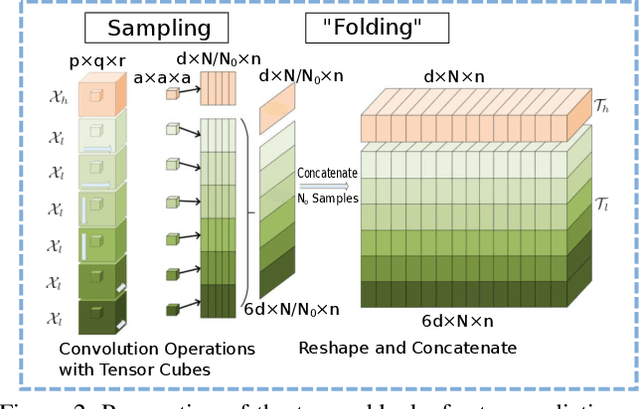

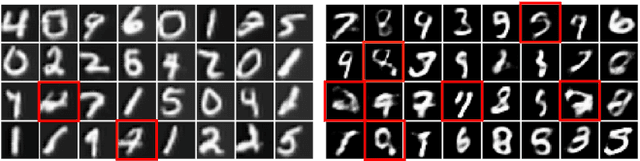

TGAN: Deep Tensor Generative Adversarial Nets for Large Image Generation

Jan 28, 2019

Deep generative models have been successfully applied to many applications. However, existing works experience limitations when generating large images (the literature usually generates small images, e.g. 32 * 32 or 128 * 128). In this paper, we propose a novel scheme, called deep tensor adversarial generative nets (TGAN), that generates large high-quality images by exploring tensor structures. Essentially, the adversarial process of TGAN takes place in a tensor space. First, we impose tensor structures for concise image representation, which is superior in capturing the pixel proximity information and the spatial patterns of elementary objects in images, over the vectorization preprocess in existing works. Secondly, we propose TGAN that integrates deep convolutional generative adversarial networks and tensor super-resolution in a cascading manner, to generate high-quality images from random distributions. More specifically, we design a tensor super-resolution process that consists of tensor dictionary learning and tensor coefficients learning. Finally, on three datasets, the proposed TGAN generates images with more realistic textures, compared with state-of-the-art adversarial autoencoders. The size of the generated images is increased by over 8.5 times, namely 374 * 374 in PASCAL2.

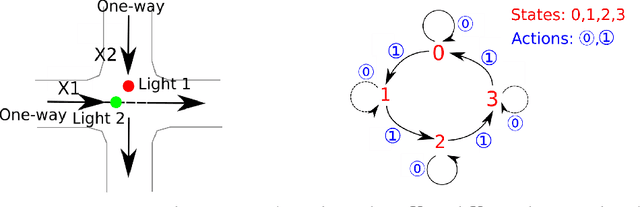

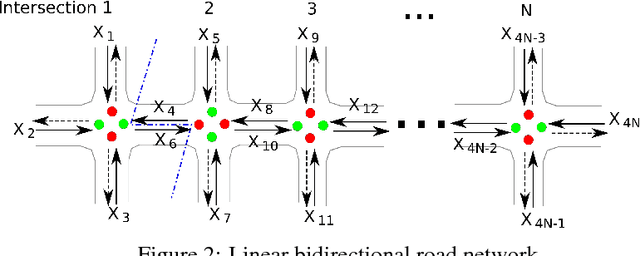

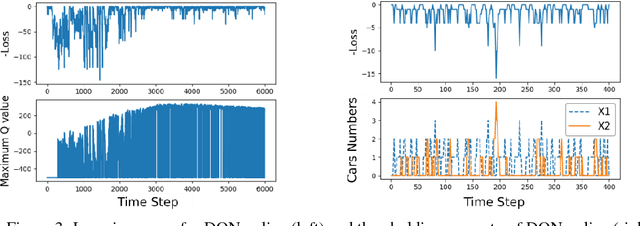

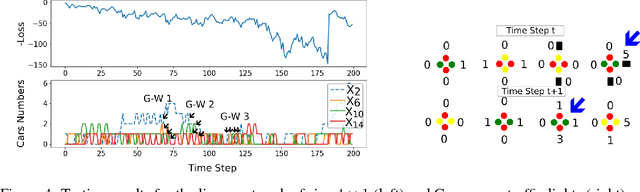

Deep Reinforcement Learning for Intelligent Transportation Systems

Dec 03, 2018

Intelligent Transportation Systems (ITSs) are envisioned to play a critical role in improving traffic flow and reducing congestion, which is a pervasive issue impacting urban areas around the globe. Rapidly advancing vehicular communication and edge cloud computation technologies provide key enablers for smart traffic management. However, operating viable real-time actuation mechanisms on a practically relevant scale involves formidable challenges, e.g., policy iteration and conventional Reinforcement Learning (RL) techniques suffer from poor scalability due to state space explosion. Motivated by these issues, we explore the potential for Deep Q-Networks (DQN) to optimize traffic light control policies. As an initial benchmark, we establish that the DQN algorithms yield the "thresholding" policy in a single-intersection. Next, we examine the scalability properties of DQN algorithms and their performance in a linear network topology with several intersections along a main artery. We demonstrate that DQN algorithms produce intelligent behavior, such as the emergence of "greenwave" patterns, reflecting their ability to learn favorable traffic light actuations.

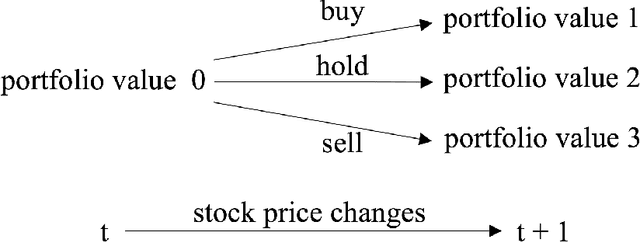

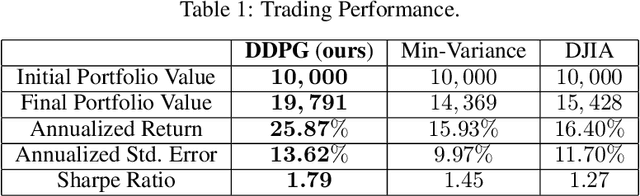

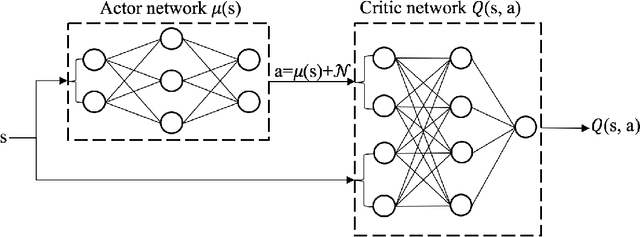

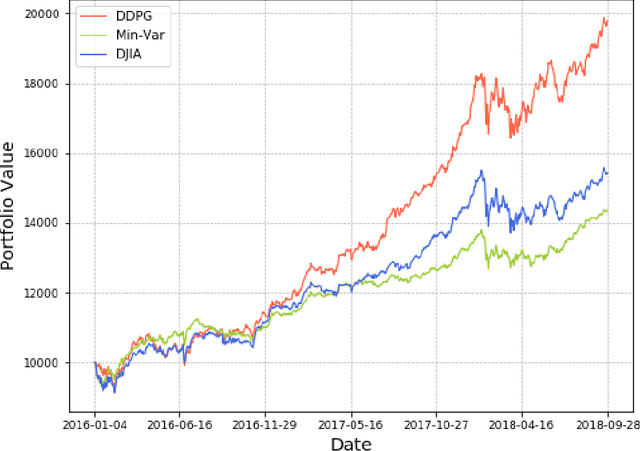

Practical Deep Reinforcement Learning Approach for Stock Trading

Dec 02, 2018

Stock trading strategy plays a crucial role in investment companies. However, it is challenging to obtain optimal strategy in the complex and dynamic stock market. We explore the potential of deep reinforcement learning to optimize stock trading strategy and thus maximize investment return. 30 stocks are selected as our trading stocks and their daily prices are used as the training and trading market environment. We train a deep reinforcement learning agent and obtain an adaptive trading strategy. The agent's performance is evaluated and compared with Dow Jones Industrial Average and the traditional min-variance portfolio allocation strategy. The proposed deep reinforcement learning approach is shown to outperform the two baselines in terms of both the Sharpe ratio and cumulative returns.