Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeContextual Online Bilateral Trade

Feb 13, 2026We study repeated bilateral trade when the valuations of the sellers and the buyers are contextual. More precisely, the agents' valuations are given by the inner product of a context vector with two unknown $d$-dimensional vectors -- one for the buyers and one for the sellers. At each time step $t$, the learner receives a context and posts two prices, one for the seller and one for the buyer, and the trade happens if both agents accept their price. We study two objectives for this problem, gain from trade and profit, proving no-regret with respect to a surprisingly strong benchmark: the best omniscient dynamic strategy. In the natural scenario where the learner observes \emph{separately} whether the agents accept their price -- the so-called \emph{two-bit} feedback -- we design algorithms that achieve $O(d\log d)$ regret for gain from trade, and $O(d \log\log T + d\log d)$ regret for profit maximization. Both results are tight, up to the $\log(d)$ factor, and implement per-step budget balance, meaning that the learner never incurs negative profit. In the less informative \emph{one-bit} feedback model, the learner only observes whether a trade happens or not. For this scenario, we show that the tight two-bit regret regimes are still attainable, at the cost of allowing the learner to possibly incur a small negative profit of order $O(d\log d)$, which is notably independent of the time horizon. As a final set of results, we investigate the combination of one-bit feedback and per-step budget balance. There, we design an algorithm for gain from trade that suffers regret independent of the time horizon, but \emph{exponential} in the dimension $d$. For profit maximization, we maintain this exponential dependence on the dimension, which gets multiplied by a $\log T$ factor.

Multicalibration yields better matchings

Nov 14, 2025

Consider the problem of finding the best matching in a weighted graph where we only have access to predictions of the actual stochastic weights, based on an underlying context. If the predictor is the Bayes optimal one, then computing the best matching based on the predicted weights is optimal. However, in practice, this perfect information scenario is not realistic. Given an imperfect predictor, a suboptimal decision rule may compensate for the induced error and thus outperform the standard optimal rule. In this paper, we propose multicalibration as a way to address this problem. This fairness notion requires a predictor to be unbiased on each element of a family of protected sets of contexts. Given a class of matching algorithms $\mathcal C$ and any predictor $γ$ of the edge-weights, we show how to construct a specific multicalibrated predictor $\hat γ$, with the following property. Picking the best matching based on the output of $\hat γ$ is competitive with the best decision rule in $\mathcal C$ applied onto the original predictor $γ$. We complement this result by providing sample complexity bounds.

Online Learning with Sublinear Best-Action Queries

Jul 23, 2024In online learning, a decision maker repeatedly selects one of a set of actions, with the goal of minimizing the overall loss incurred. Following the recent line of research on algorithms endowed with additional predictive features, we revisit this problem by allowing the decision maker to acquire additional information on the actions to be selected. In particular, we study the power of \emph{best-action queries}, which reveal beforehand the identity of the best action at a given time step. In practice, predictive features may be expensive, so we allow the decision maker to issue at most $k$ such queries. We establish tight bounds on the performance any algorithm can achieve when given access to $k$ best-action queries for different types of feedback models. In particular, we prove that in the full feedback model, $k$ queries are enough to achieve an optimal regret of $\Theta\left(\min\left\{\sqrt T, \frac Tk\right\}\right)$. This finding highlights the significant multiplicative advantage in the regret rate achievable with even a modest (sublinear) number $k \in \Omega(\sqrt{T})$ of queries. Additionally, we study the challenging setting in which the only available feedback is obtained during the time steps corresponding to the $k$ best-action queries. There, we provide a tight regret rate of $\Theta\left(\min\left\{\frac{T}{\sqrt k},\frac{T^2}{k^2}\right\}\right)$, which improves over the standard $\Theta\left(\frac{T}{\sqrt k}\right)$ regret rate for label efficient prediction for $k \in \Omega(T^{2/3})$.

The Role of Transparency in Repeated First-Price Auctions with Unknown Valuations

Jul 14, 2023

We study the problem of regret minimization for a single bidder in a sequence of first-price auctions where the bidder knows the item's value only if the auction is won. Our main contribution is a complete characterization, up to logarithmic factors, of the minimax regret in terms of the auction's transparency, which regulates the amount of information on competing bids disclosed by the auctioneer at the end of each auction. Our results hold under different assumptions (stochastic, adversarial, and their smoothed variants) on the environment generating the bidder's valuations and competing bids. These minimax rates reveal how the interplay between transparency and the nature of the environment affects how fast one can learn to bid optimally in first-price auctions.

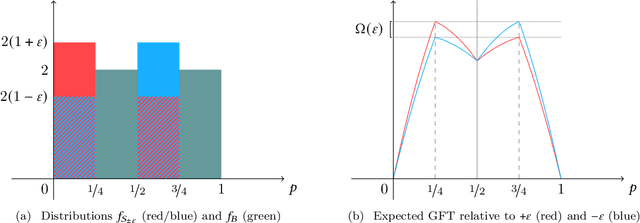

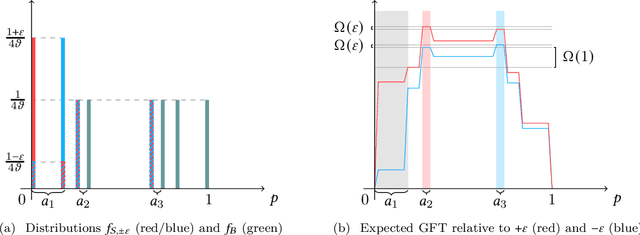

Repeated Bilateral Trade Against a Smoothed Adversary

Feb 21, 2023We study repeated bilateral trade where an adaptive $\sigma$-smooth adversary generates the valuations of sellers and buyers. We provide a complete characterization of the regret regimes for fixed-price mechanisms under different feedback models in the two cases where the learner can post either the same or different prices to buyers and sellers. We begin by showing that the minimax regret after $T$ rounds is of order $\sqrt{T}$ in the full-feedback scenario. Under partial feedback, any algorithm that has to post the same price to buyers and sellers suffers worst-case linear regret. However, when the learner can post two different prices at each round, we design an algorithm enjoying regret of order $T^{3/4}$ ignoring log factors. We prove that this rate is optimal by presenting a surprising $T^{3/4}$ lower bound, which is the main technical contribution of the paper.

Fully Dynamic Online Selection through Online Contention Resolution Schemes

Jan 08, 2023

We study fully dynamic online selection problems in an adversarial/stochastic setting that includes Bayesian online selection, prophet inequalities, posted price mechanisms, and stochastic probing problems subject to combinatorial constraints. In the classical ``incremental'' version of the problem, selected elements remain active until the end of the input sequence. On the other hand, in the fully dynamic version of the problem, elements stay active for a limited time interval, and then leave. This models, for example, the online matching of tasks to workers with task/worker-dependent working times, and sequential posted pricing of perishable goods. A successful approach to online selection problems in the adversarial setting is given by the notion of Online Contention Resolution Scheme (OCRS), that uses a priori information to formulate a linear relaxation of the underlying optimization problem, whose optimal fractional solution is rounded online for any adversarial order of the input sequence. Our main contribution is providing a general method for constructing an OCRS for fully dynamic online selection problems. Then, we show how to employ such OCRS to construct no-regret algorithms in a partial information model with semi-bandit feedback and adversarial inputs.

AI-based Data Preparation and Data Analytics in Healthcare: The Case of Diabetes

Jun 13, 2022

The Associazione Medici Diabetologi (AMD) collects and manages one of the largest worldwide-available collections of diabetic patient records, also known as the AMD database. This paper presents the initial results of an ongoing project whose focus is the application of Artificial Intelligence and Machine Learning techniques for conceptualizing, cleaning, and analyzing such an important and valuable dataset, with the goal of providing predictive insights to better support diabetologists in their diagnostic and therapeutic choices.

Allocating Indivisible Goods to Strategic Agents: Pure Nash Equilibria and Fairness

Sep 17, 2021We consider the problem of fairly allocating a set of indivisible goods to a set of strategic agents with additive valuation functions. We assume no monetary transfers and, therefore, a mechanism in our setting is an algorithm that takes as input the reported -- rather than the true -- values of the agents. Our main goal is to explore whether there exist mechanisms that have pure Nash equilibria for every instance and, at the same time, provide fairness guarantees for the allocations that correspond to these equilibria. We focus on two relaxations of envy-freeness, namely envy-freeness up to one good (EF1), and envy-freeness up to any good (EFX), and we positively answer the above question. In particular, we study two algorithms that are known to produce such allocations in the non-strategic setting: Round-Robin (EF1 allocations for any number of agents) and a cut-and-choose algorithm of Plaut and Roughgarden [SIAM Journal of Discrete Mathematics, 2020] (EFX allocations for two agents). For Round-Robin we show that all of its pure Nash equilibria induce allocations that are EF1 with respect to the underlying true values, while for the algorithm of Plaut and Roughgarden we show that the corresponding allocations not only are EFX but also satisfy maximin share fairness, something that is not true for this algorithm in the non-strategic setting! Further, we show that a weaker version of the latter result holds for any mechanism for two agents that always has pure Nash equilibria which all induce EFX allocations.

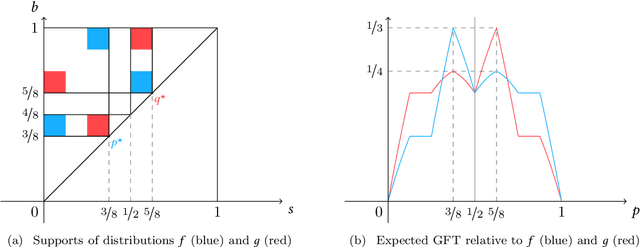

Bilateral Trade: A Regret Minimization Perspective

Sep 08, 2021

Bilateral trade, a fundamental topic in economics, models the problem of intermediating between two strategic agents, a seller and a buyer, willing to trade a good for which they hold private valuations. In this paper, we cast the bilateral trade problem in a regret minimization framework over $T$ rounds of seller/buyer interactions, with no prior knowledge on their private valuations. Our main contribution is a complete characterization of the regret regimes for fixed-price mechanisms with different feedback models and private valuations, using as a benchmark the best fixed-price in hindsight. More precisely, we prove the following tight bounds on the regret: - $\Theta(\sqrt{T})$ for full-feedback (i.e., direct revelation mechanisms). - $\Theta(T^{2/3})$ for realistic feedback (i.e., posted-price mechanisms) and independent seller/buyer valuations with bounded densities. - $\Theta(T)$ for realistic feedback and seller/buyer valuations with bounded densities. - $\Theta(T)$ for realistic feedback and independent seller/buyer valuations. - $\Theta(T)$ for the adversarial setting.

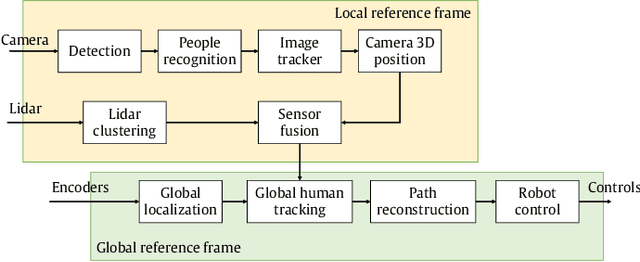

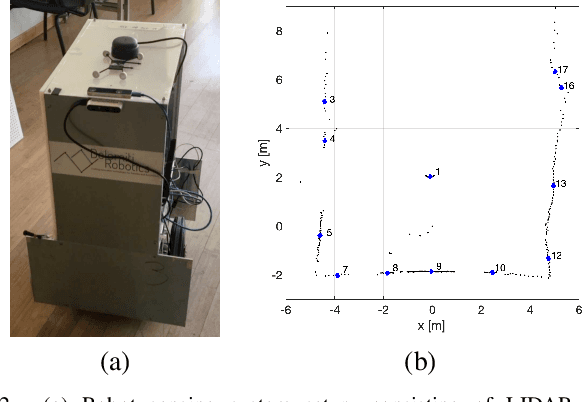

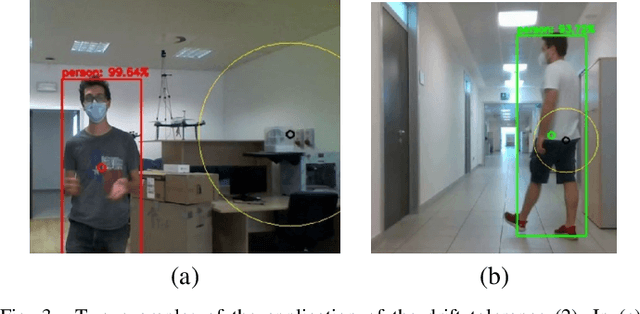

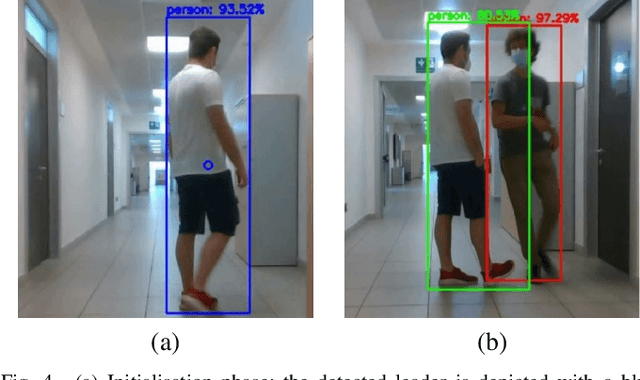

Humans as Path-Finders for Safe Navigation

Jul 07, 2021

One of the most important barriers toward a widespread use of mobile robots in unstructured and human populated work environments is the ability to plan a safe path. In this paper, we propose to delegate this activity to a human operator that walks in front of the robot marking with her/his footsteps the path to be followed. The implementation of this approach requires a high degree of robustness in locating the specific person to be followed (the leader). We propose a three phase approach to fulfil this goal: 1. identification and tracking of the person in the image space, 2. sensor fusion between camera data and laser sensors, 3. point interpolation with continuous curvature curves. The approach is described in the paper and extensively validated with experimental results.