Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeTuning Mixed Input Hyperparameters on the Fly for Efficient Population Based AutoRL

Jun 30, 2021

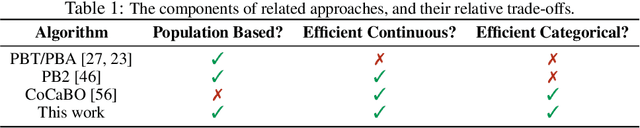

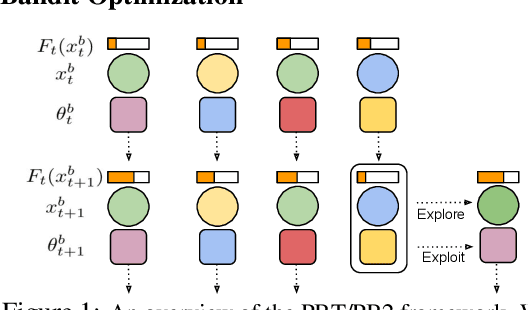

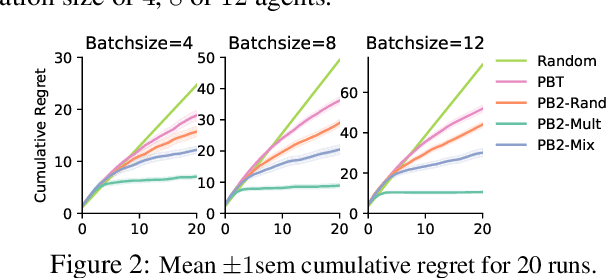

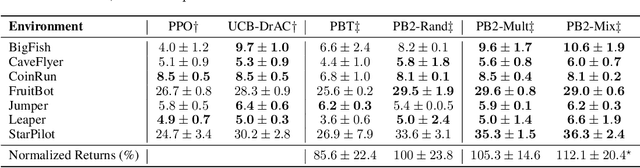

Despite a series of recent successes in reinforcement learning (RL), many RL algorithms remain sensitive to hyperparameters. As such, there has recently been interest in the field of AutoRL, which seeks to automate design decisions to create more general algorithms. Recent work suggests that population based approaches may be effective AutoRL algorithms, by learning hyperparameter schedules on the fly. In particular, the PB2 algorithm is able to achieve strong performance in RL tasks by formulating online hyperparameter optimization as time varying GP-bandit problem, while also providing theoretical guarantees. However, PB2 is only designed to work for continuous hyperparameters, which severely limits its utility in practice. In this paper we introduce a new (provably) efficient hierarchical approach for optimizing both continuous and categorical variables, using a new time-varying bandit algorithm specifically designed for the population based training regime. We evaluate our approach on the challenging Procgen benchmark, where we show that explicitly modelling dependence between data augmentation and other hyperparameters improves generalization.

Slow Momentum with Fast Reversion: A Trading Strategy Using Deep Learning and Changepoint Detection

Jun 18, 2021Momentum strategies are an important part of alternative investments and are at the heart of commodity trading advisors (CTAs). These strategies have however been found to have difficulties adjusting to rapid changes in market conditions, such as during the 2020 market crash. In particular, immediately after momentum turning points, where a trend reverses from an uptrend (downtrend) to a downtrend (uptrend), time-series momentum (TSMOM) strategies are prone to making bad bets. To improve the response to regime change, we introduce a novel approach, where we insert an online change-point detection (CPD) module into a Deep Momentum Network (DMN) [1904.04912] pipeline, which uses an LSTM deep-learning architecture to simultaneously learn both trend estimation and position sizing. Furthermore, our model is able to optimise the way in which it balances 1) a slow momentum strategy which exploits persisting trends, but does not overreact to localised price moves, and 2) a fast mean-reversion strategy regime by quickly flipping its position, then swapping it back again to exploit localised price moves. Our CPD module outputs a changepoint location and severity score, allowing our model to learn to respond to varying degrees of disequilibrium, or smaller and more localised changepoints, in a data driven manner. Using a portfolio of 50, liquid, continuous futures contracts over the period 1990-2020, the addition of the CPD module leads to an improvement in Sharpe ratio of one-third. Even more notably, this module is especially beneficial in periods of significant nonstationarity, and in particular, over the most recent years tested (2015-2020) the performance boost is approximately two-thirds. This is especially interesting as traditional momentum strategies have been underperforming in this period.

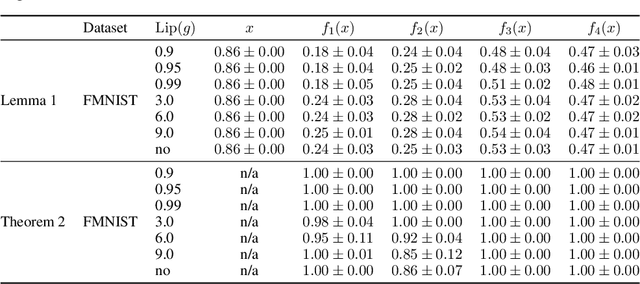

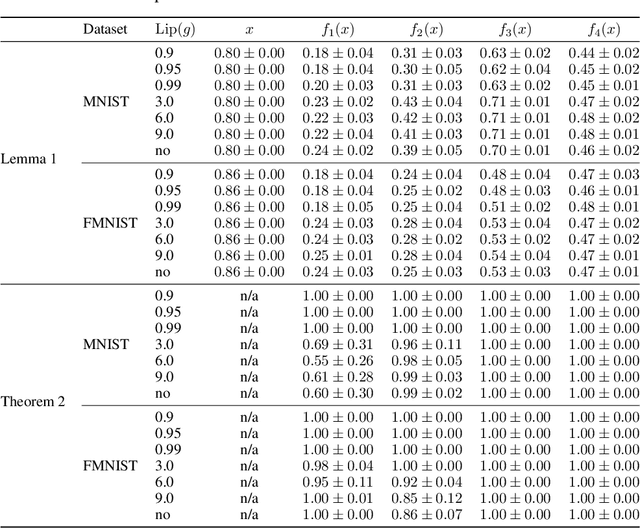

Can convolutional ResNets approximately preserve input distances? A frequency analysis perspective

Jun 17, 2021

ResNets constrained to be bi-Lipschitz, that is, approximately distance preserving, have been a crucial component of recently proposed techniques for deterministic uncertainty quantification in neural models. We show that theoretical justifications for recent regularisation schemes trying to enforce such a constraint suffer from a crucial flaw -- the theoretical link between the regularisation scheme used and bi-Lipschitzness is only valid under conditions which do not hold in practice, rendering existing theory of limited use, despite the strong empirical performance of these models. We provide a theoretical explanation for the effectiveness of these regularisation schemes using a frequency analysis perspective, showing that under mild conditions these schemes will enforce a lower Lipschitz bound on the low-frequency projection of images. We then provide empirical evidence supporting our theoretical claims, and perform further experiments which demonstrate that our broader conclusions appear to hold when some of the mathematical assumptions of our proof are relaxed, corresponding to the setup used in prior work. In addition, we present a simple constructive algorithm to search for counter examples to the distance preservation condition, and discuss possible implications of our theory for future model design.

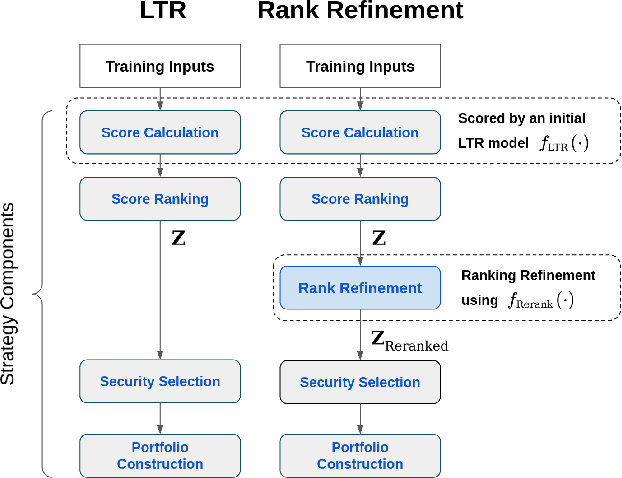

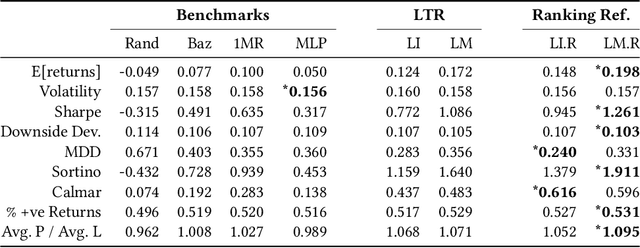

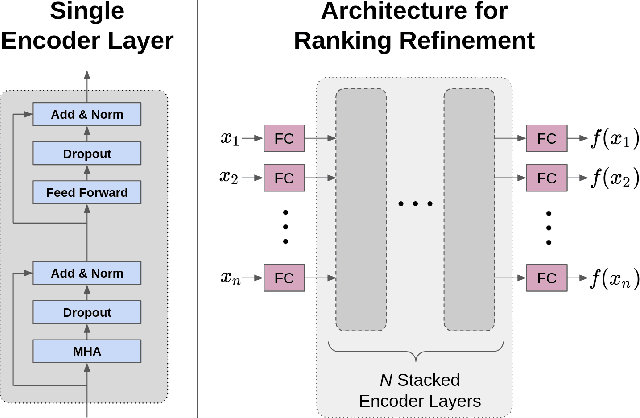

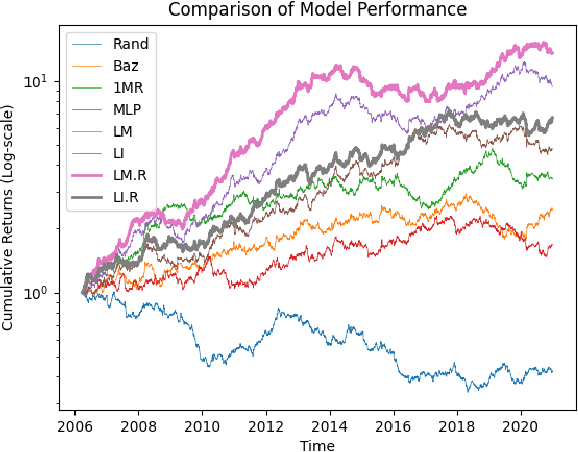

Enhancing Cross-Sectional Currency Strategies by Ranking Refinement with Transformer-based Architectures

May 20, 2021

The performance of a cross-sectional currency strategy depends crucially on accurately ranking instruments prior to portfolio construction. While this ranking step is traditionally performed using heuristics, or by sorting outputs produced by pointwise regression or classification models, Learning to Rank algorithms have recently presented themselves as competitive and viable alternatives. Despite improving ranking accuracy on average however, these techniques do not account for the possibility that assets positioned at the extreme ends of the ranked list -- which are ultimately used to construct the long/short portfolios -- can assume different distributions in the input space, and thus lead to sub-optimal strategy performance. Drawing from research in Information Retrieval that demonstrates the utility of contextual information embedded within top-ranked documents to learn the query's characteristics to improve ranking, we propose an analogous approach: exploiting the features of both out- and under-performing instruments to learn a model for refining the original ranked list. Under a re-ranking framework, we adapt the Transformer architecture to encode the features of extreme assets for refining our selection of long/short instruments obtained with an initial retrieval. Backtesting on a set of 31 currencies, our proposed methodology significantly boosts Sharpe ratios -- by approximately 20% over the original LTR algorithms and double that of traditional baselines.

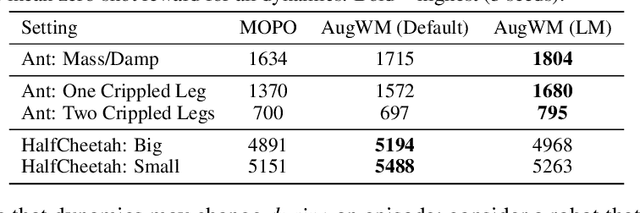

Augmented World Models Facilitate Zero-Shot Dynamics Generalization From a Single Offline Environment

Apr 12, 2021

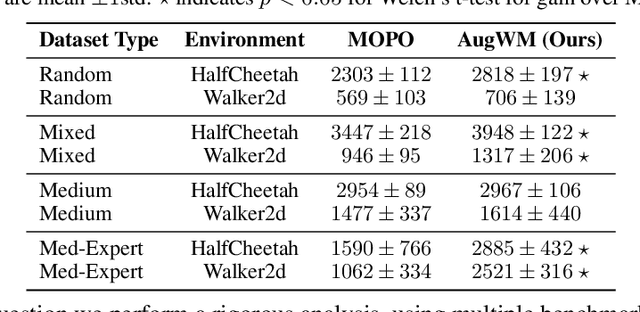

Reinforcement learning from large-scale offline datasets provides us with the ability to learn policies without potentially unsafe or impractical exploration. Significant progress has been made in the past few years in dealing with the challenge of correcting for differing behavior between the data collection and learned policies. However, little attention has been paid to potentially changing dynamics when transferring a policy to the online setting, where performance can be up to 90% reduced for existing methods. In this paper we address this problem with Augmented World Models (AugWM). We augment a learned dynamics model with simple transformations that seek to capture potential changes in physical properties of the robot, leading to more robust policies. We not only train our policy in this new setting, but also provide it with the sampled augmentation as a context, allowing it to adapt to changes in the environment. At test time we learn the context in a self-supervised fashion by approximating the augmentation which corresponds to the new environment. We rigorously evaluate our approach on over 100 different changed dynamics settings, and show that this simple approach can significantly improve the zero-shot generalization of a recent state-of-the-art baseline, often achieving successful policies where the baseline fails.

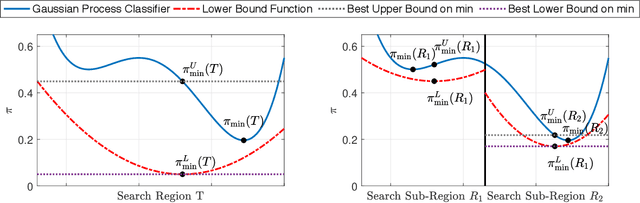

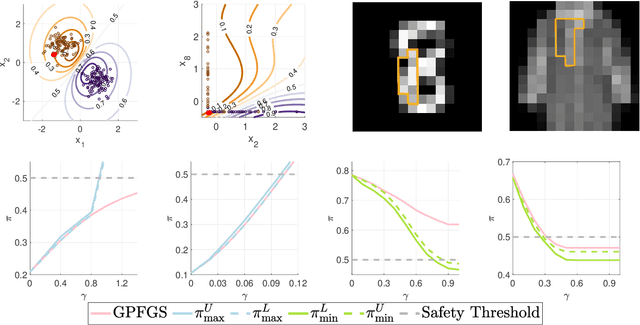

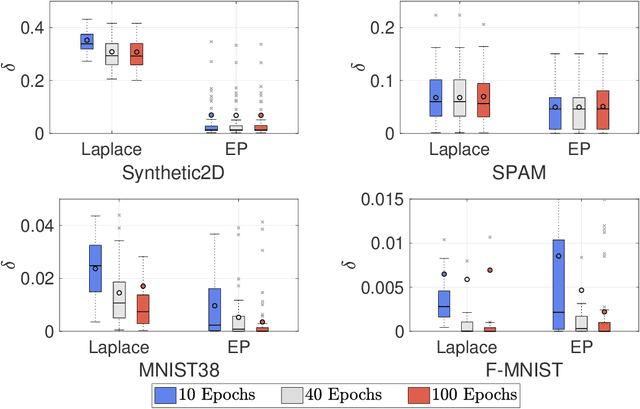

Adversarial Robustness Guarantees for Gaussian Processes

Apr 07, 2021

Gaussian processes (GPs) enable principled computation of model uncertainty, making them attractive for safety-critical applications. Such scenarios demand that GP decisions are not only accurate, but also robust to perturbations. In this paper we present a framework to analyse adversarial robustness of GPs, defined as invariance of the model's decision to bounded perturbations. Given a compact subset of the input space $T\subseteq \mathbb{R}^d$, a point $x^*$ and a GP, we provide provable guarantees of adversarial robustness of the GP by computing lower and upper bounds on its prediction range in $T$. We develop a branch-and-bound scheme to refine the bounds and show, for any $\epsilon > 0$, that our algorithm is guaranteed to converge to values $\epsilon$-close to the actual values in finitely many iterations. The algorithm is anytime and can handle both regression and classification tasks, with analytical formulation for most kernels used in practice. We evaluate our methods on a collection of synthetic and standard benchmark datasets, including SPAM, MNIST and FashionMNIST. We study the effect of approximate inference techniques on robustness and demonstrate how our method can be used for interpretability. Our empirical results suggest that the adversarial robustness of GPs increases with accurate posterior estimation.

Building Cross-Sectional Systematic Strategies By Learning to Rank

Dec 13, 2020The success of a cross-sectional systematic strategy depends critically on accurately ranking assets prior to portfolio construction. Contemporary techniques perform this ranking step either with simple heuristics or by sorting outputs from standard regression or classification models, which have been demonstrated to be sub-optimal for ranking in other domains (e.g. information retrieval). To address this deficiency, we propose a framework to enhance cross-sectional portfolios by incorporating learning-to-rank algorithms, which lead to improvements of ranking accuracy by learning pairwise and listwise structures across instruments. Using cross-sectional momentum as a demonstrative case study, we show that the use of modern machine learning ranking algorithms can substantially improve the trading performance of cross-sectional strategies -- providing approximately threefold boosting of Sharpe Ratios compared to traditional approaches.

Explaining the Adaptive Generalisation Gap

Nov 15, 2020

We conjecture that the reason for the difference in generalisation between adaptive and non adaptive gradient methods stems from the failure of adaptive methods to account for the greater levels of noise associated with flatter directions in their estimates of local curvature. This conjecture motivated by results in random matrix theory has implications for optimisation in both simple convex settings and deep neural networks. We demonstrate that typical schedules used for adaptive methods (with low numerical stability or damping constants) serve to bias relative movement towards flat directions relative to sharp directions, effectively amplifying the noise-to-signal ratio and harming generalisation. We show that the numerical stability/damping constant used in these methods can be decomposed into a learning rate reduction and linear shrinkage of the estimated curvature matrix. We then demonstrate significant generalisation improvements by increasing the shrinkage coefficient, closing the generalisation gap entirely in our neural network experiments. Finally, we show that other popular modifications to adaptive methods, such as decoupled weight decay and partial adaptivity can be shown to calibrate parameter updates to make better use of sharper, more reliable directions.

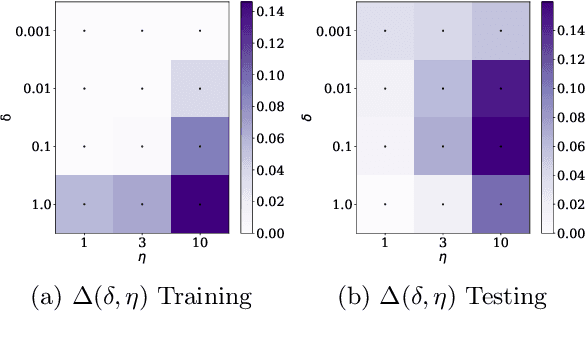

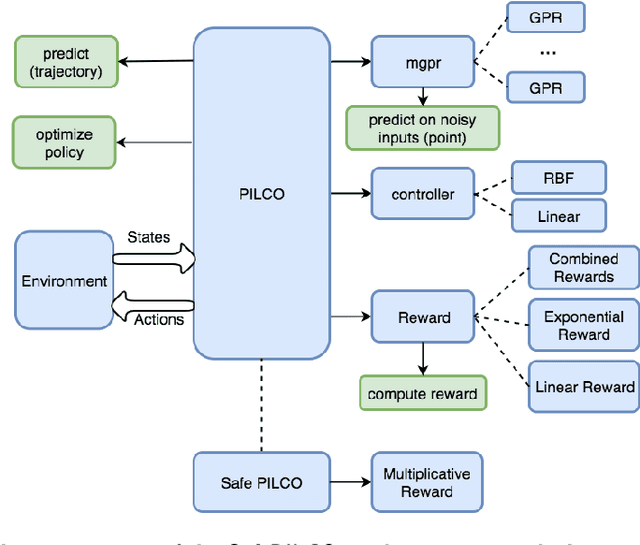

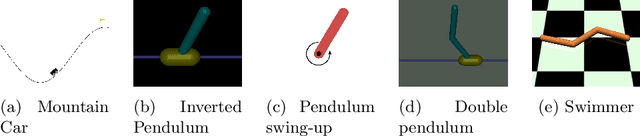

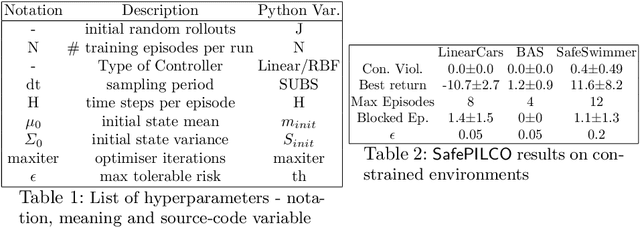

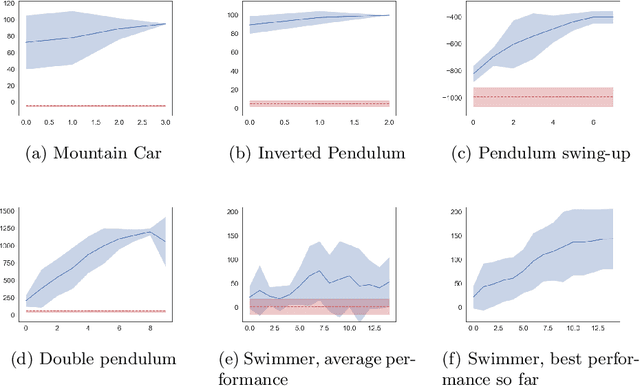

SafePILCO: a software tool for safe and data-efficient policy synthesis

Aug 07, 2020

SafePILCO is a software tool for safe and data-efficient policy search with reinforcement learning. It extends the known PILCO algorithm, originally written in MATLAB, to support safe learning. We provide a Python implementation and leverage existing libraries that allow the codebase to remain short and modular, which is appropriate for wider use by the verification, reinforcement learning, and control communities.

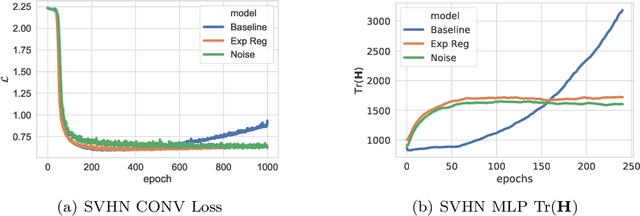

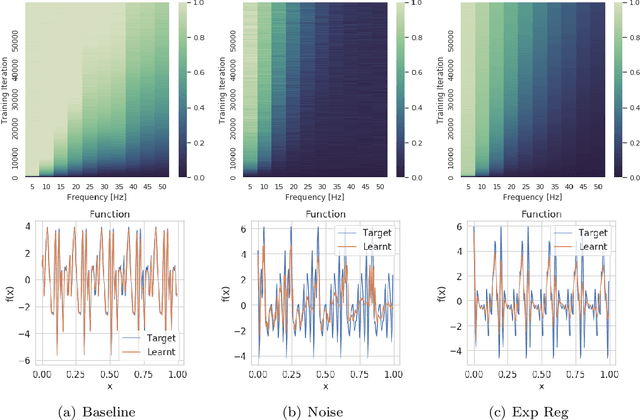

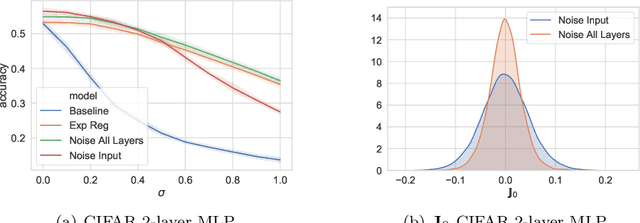

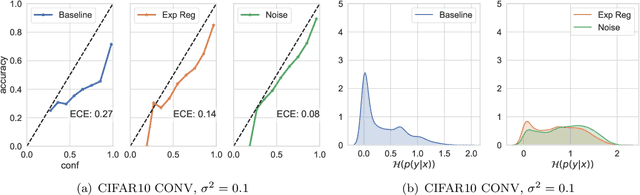

Explicit Regularisation in Gaussian Noise Injections

Jul 14, 2020

We study the regularisation induced in neural networks by Gaussian noise injections (GNIs). Though such injections have been extensively studied when applied to data, there have been few studies on understanding the regularising effect they induce when applied to network activations. Here we derive the explicit regulariser of GNIs, obtained by marginalising out the injected noise, and show that it is a form of Tikhonov regularisation which penalises functions with high-frequency components in the Fourier domain. We show analytically and empirically that such regularisation produces calibrated classifiers with large classification margins and that the explicit regulariser we derive is able to reproduce these effects.