Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeMulti-Label Learning to Rank through Multi-Objective Optimization

Jul 08, 2022

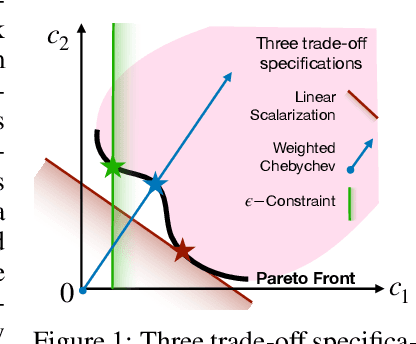

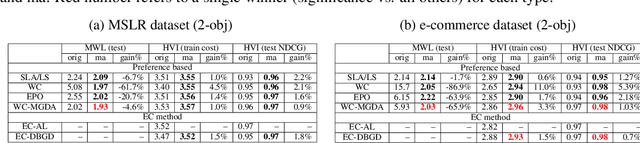

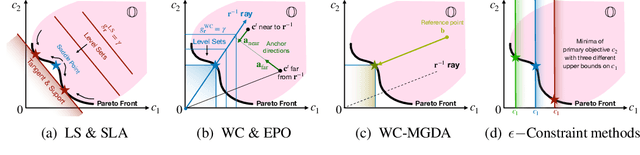

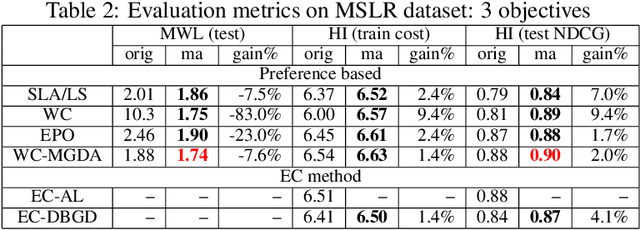

Learning to Rank (LTR) technique is ubiquitous in the Information Retrieval system nowadays, especially in the Search Ranking application. The query-item relevance labels typically used to train the ranking model are often noisy measurements of human behavior, e.g., product rating for product search. The coarse measurements make the ground truth ranking non-unique with respect to a single relevance criterion. To resolve ambiguity, it is desirable to train a model using many relevance criteria, giving rise to Multi-Label LTR (MLLTR). Moreover, it formulates multiple goals that may be conflicting yet important to optimize for simultaneously, e.g., in product search, a ranking model can be trained based on product quality and purchase likelihood to increase revenue. In this research, we leverage the Multi-Objective Optimization (MOO) aspect of the MLLTR problem and employ recently developed MOO algorithms to solve it. Specifically, we propose a general framework where the information from labels can be combined in a variety of ways to meaningfully characterize the trade-off among the goals. Our framework allows for any gradient based MOO algorithm to be used for solving the MLLTR problem. We test the proposed framework on two publicly available LTR datasets and one e-commerce dataset to show its efficacy.

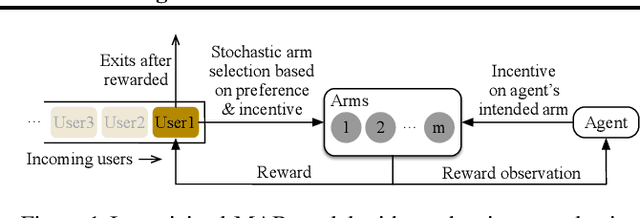

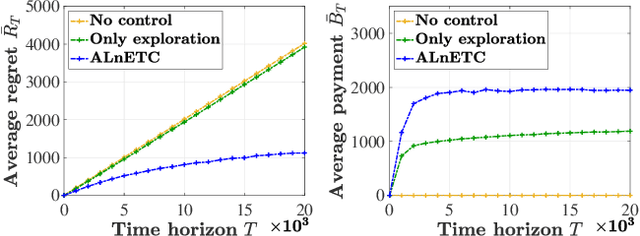

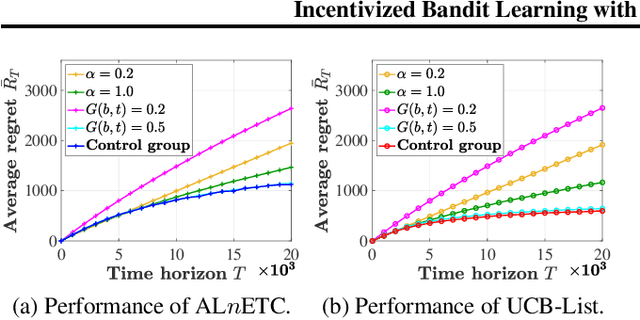

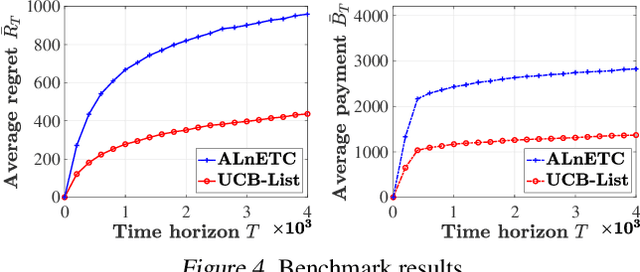

Incentivized Bandit Learning with Self-Reinforcing User Preferences

May 31, 2021

In this paper, we investigate a new multi-armed bandit (MAB) online learning model that considers real-world phenomena in many recommender systems: (i) the learning agent cannot pull the arms by itself and thus has to offer rewards to users to incentivize arm-pulling indirectly; and (ii) if users with specific arm preferences are well rewarded, they induce a "self-reinforcing" effect in the sense that they will attract more users of similar arm preferences. Besides addressing the tradeoff of exploration and exploitation, another key feature of this new MAB model is to balance reward and incentivizing payment. The goal of the agent is to maximize the total reward over a fixed time horizon $T$ with a low total payment. Our contributions in this paper are two-fold: (i) We propose a new MAB model with random arm selection that considers the relationship of users' self-reinforcing preferences and incentives; and (ii) We leverage the properties of a multi-color Polya urn with nonlinear feedback model to propose two MAB policies termed "At-Least-$n$ Explore-Then-Commit" and "UCB-List". We prove that both policies achieve $O(log T)$ expected regret with $O(log T)$ expected payment over a time horizon $T$. We conduct numerical simulations to demonstrate and verify the performances of these two policies and study their robustness under various settings.

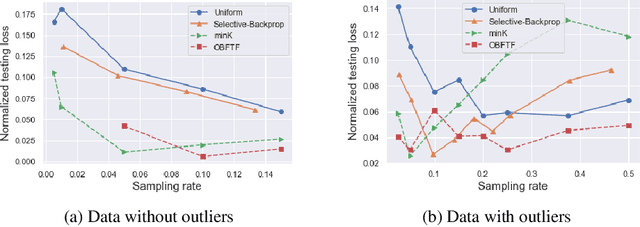

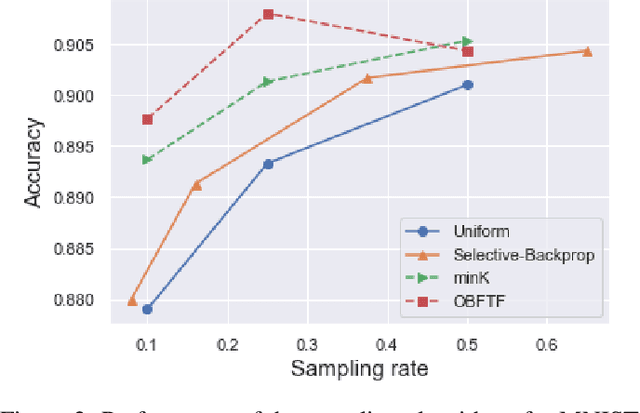

One Backward from Ten Forward, Subsampling for Large-Scale Deep Learning

Apr 27, 2021

Deep learning models in large-scale machine learning systems are often continuously trained with enormous data from production environments. The sheer volume of streaming training data poses a significant challenge to real-time training subsystems and ad-hoc sampling is the standard practice. Our key insight is that these deployed ML systems continuously perform forward passes on data instances during inference, but ad-hoc sampling does not take advantage of this substantial computational effort. Therefore, we propose to record a constant amount of information per instance from these forward passes. The extra information measurably improves the selection of which data instances should participate in forward and backward passes. A novel optimization framework is proposed to analyze this problem and we provide an efficient approximation algorithm under the framework of Mini-batch gradient descent as a practical solution. We also demonstrate the effectiveness of our framework and algorithm on several large-scale classification and regression tasks, when compared with competitive baselines widely used in industry.

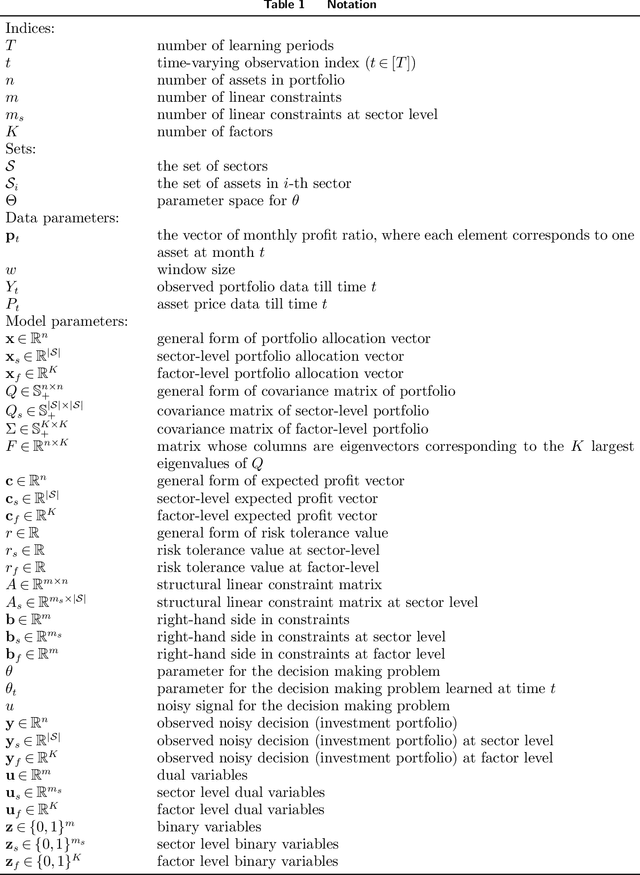

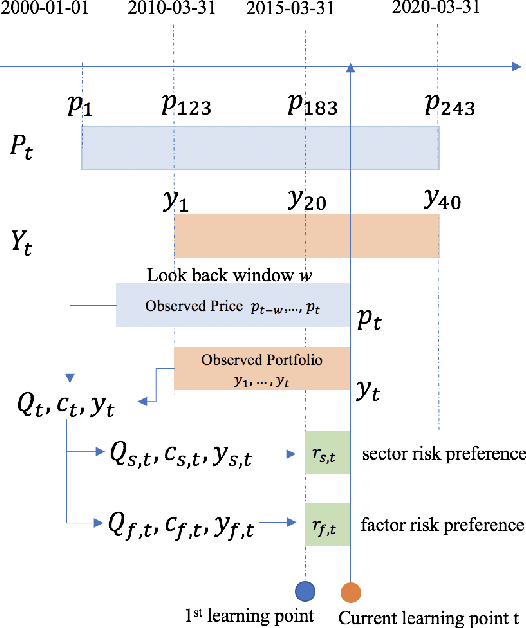

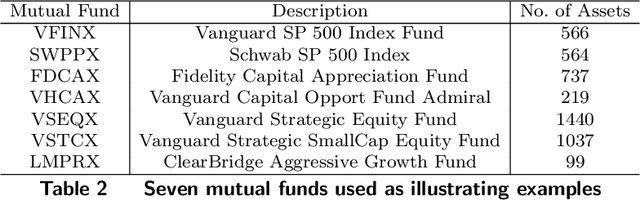

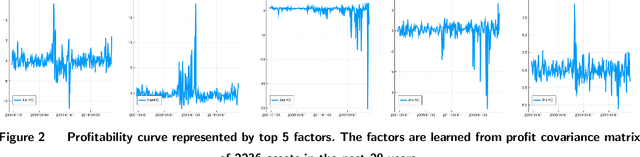

Learning Time Varying Risk Preferences from Investment Portfolios using Inverse Optimization with Applications on Mutual Funds

Oct 22, 2020

The fundamental principle in Modern Portfolio Theory (MPT) is based on the quantification of the portfolio's risk related to performance. Although MPT has made huge impacts on the investment world and prompted the success and prevalence of passive investing, it still has shortcomings in real-world applications. One of the main challenges is that the level of risk an investor can endure, known as \emph{risk-preference}, is a subjective choice that is tightly related to psychology and behavioral science in decision making. This paper presents a novel approach of measuring risk preference from existing portfolios using inverse optimization on the mean-variance portfolio allocation framework. Our approach allows the learner to continuously estimate real-time risk preferences using concurrent observed portfolios and market price data. We demonstrate our methods on real market data that consists of 20 years of asset pricing and 10 years of mutual fund portfolio holdings. Moreover, the quantified risk preference parameters are validated with two well-known risk measurements currently applied in the field. The proposed methods could lead to practical and fruitful innovations in automated/personalized portfolio management, such as Robo-advising, to augment financial advisors' decision intelligence in a long-term investment horizon.

Inverse Multiobjective Optimization Through Online Learning

Oct 12, 2020

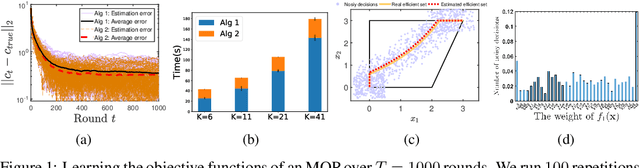

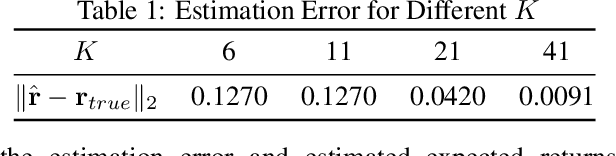

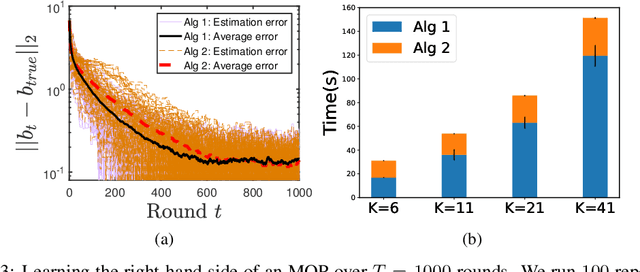

We study the problem of learning the objective functions or constraints of a multiobjective decision making model, based on a set of sequentially arrived decisions. In particular, these decisions might not be exact and possibly carry measurement noise or are generated with the bounded rationality of decision makers. In this paper, we propose a general online learning framework to deal with this learning problem using inverse multiobjective optimization. More precisely, we develop two online learning algorithms with implicit update rules which can handle noisy data. Numerical results show that both algorithms can learn the parameters with great accuracy and are robust to noise.

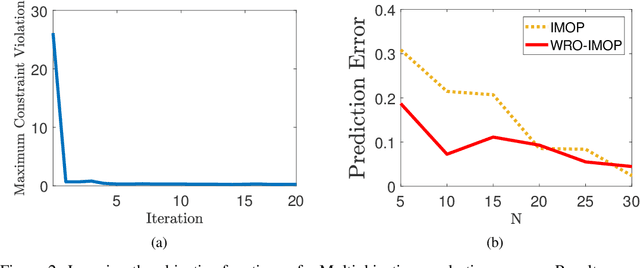

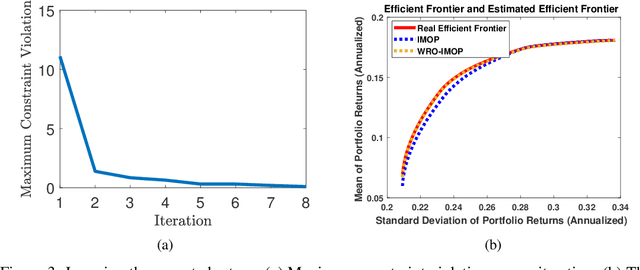

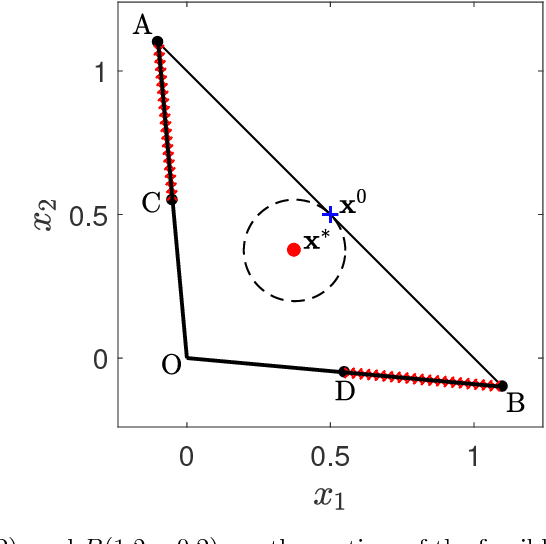

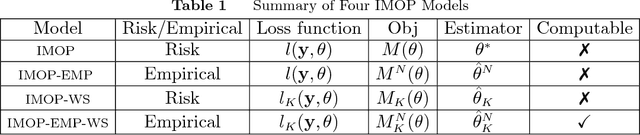

Wasserstein Distributionally Robust Inverse Multiobjective Optimization

Sep 30, 2020

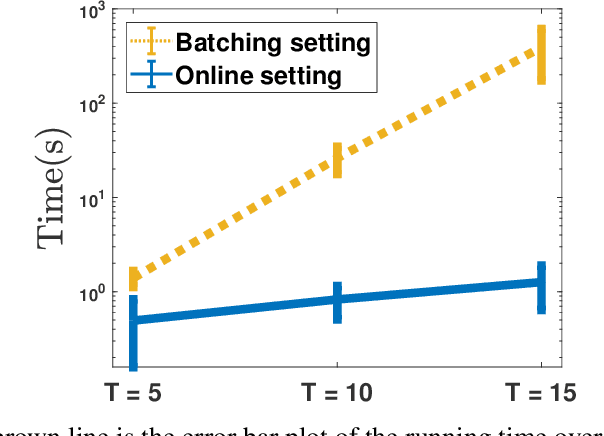

Inverse multiobjective optimization provides a general framework for the unsupervised learning task of inferring parameters of a multiobjective decision making problem (DMP), based on a set of observed decisions from the human expert. However, the performance of this framework relies critically on the availability of an accurate DMP, sufficient decisions of high quality, and a parameter space that contains enough information about the DMP. To hedge against the uncertainties in the hypothetical DMP, the data, and the parameter space, we investigate in this paper the distributionally robust approach for inverse multiobjective optimization. Specifically, we leverage the Wasserstein metric to construct a ball centered at the empirical distribution of these decisions. We then formulate a Wasserstein distributionally robust inverse multiobjective optimization problem (WRO-IMOP) that minimizes a worst-case expected loss function, where the worst case is taken over all distributions in the Wasserstein ball. We show that the excess risk of the WRO-IMOP estimator has a sub-linear convergence rate. Furthermore, we propose the semi-infinite reformulations of the WRO-IMOP and develop a cutting-plane algorithm that converges to an approximate solution in finite iterations. Finally, we demonstrate the effectiveness of our method on both a synthetic multiobjective quadratic program and a real world portfolio optimization problem.

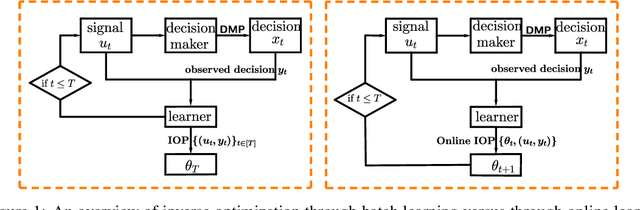

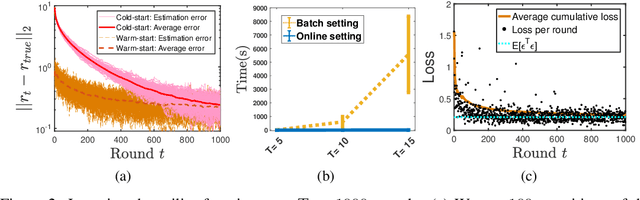

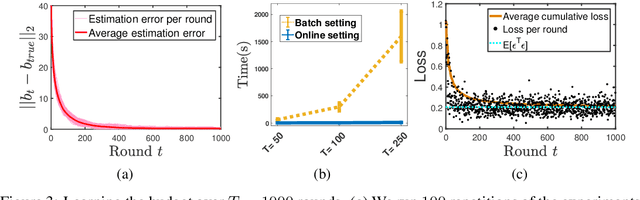

Generalized Inverse Optimization through Online Learning

Nov 02, 2018

Inverse optimization is a powerful paradigm for learning preferences and restrictions that explain the behavior of a decision maker, based on a set of external signal and the corresponding decision pairs. However, most inverse optimization algorithms are designed specifically in batch setting, where all the data is available in advance. As a consequence, there has been rare use of these methods in an online setting suitable for real-time applications. In this paper, we propose a general framework for inverse optimization through online learning. Specifically, we develop an online learning algorithm that uses an implicit update rule which can handle noisy data. Moreover, under additional regularity assumptions in terms of the data and the model, we prove that our algorithm converges at a rate of $\mathcal{O}(1/\sqrt{T})$ and is statistically consistent. In our experiments, we show the online learning approach can learn the parameters with great accuracy and is very robust to noises, and achieves a dramatic improvement in computational efficacy over the batch learning approach.

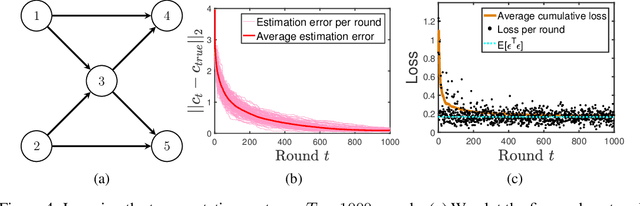

Inferring Parameters Through Inverse Multiobjective Optimization

Aug 02, 2018

Given a set of human's decisions that are observed, inverse optimization has been developed and utilized to infer the underlying decision making problem. The majority of existing studies assumes that the decision making problem is with a single objective function, and attributes data divergence to noises, errors or bounded rationality, which, however, could lead to a corrupted inference when decisions are tradeoffs among multiple criteria. In this paper, we take a data-driven approach and design a more sophisticated inverse optimization formulation to explicitly infer parameters of a multiobjective decision making problem from noisy observations. This framework, together with our mathematical analyses and advanced algorithm developments, demonstrates a strong capacity in estimating critical parameters, decoupling "interpretable" components from noises or errors, deriving the denoised \emph{optimal} decisions, and ensuring statistical significance. In particular, for the whole decision maker population, if suitable conditions hold, we will be able to understand the overall diversity and the distribution of their preferences over multiple criteria, which is important when a precise inference on every single decision maker is practically unnecessary or infeasible. Numerical results on a large number of experiments are reported to confirm the effectiveness of our unique inverse optimization model and the computational efficacy of the developed algorithms.