Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeAlmost Optimal Variance-Constrained Best Arm Identification

Jan 25, 2022

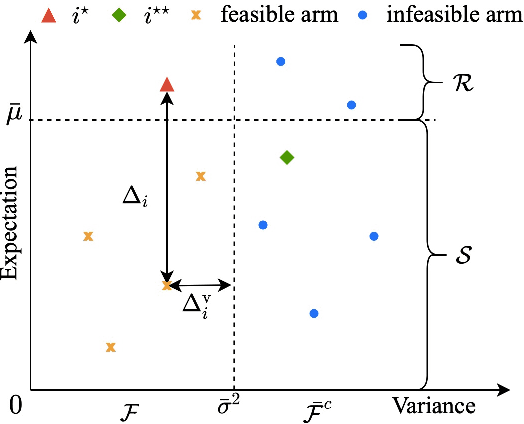

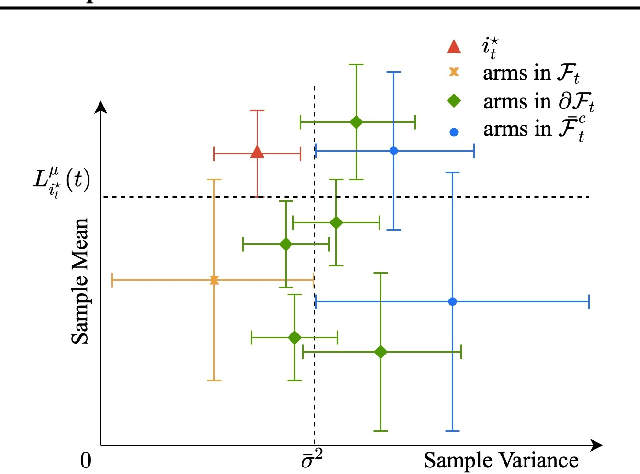

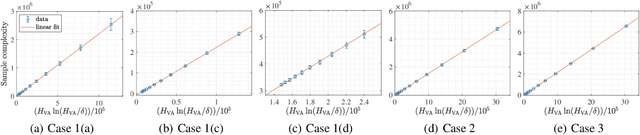

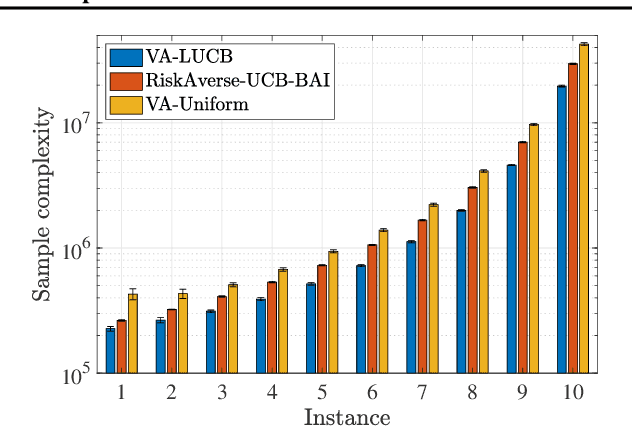

We design and analyze VA-LUCB, a parameter-free algorithm, for identifying the best arm under the fixed-confidence setup and under a stringent constraint that the variance of the chosen arm is strictly smaller than a given threshold. An upper bound on VA-LUCB's sample complexity is shown to be characterized by a fundamental variance-aware hardness quantity $H_{VA}$. By proving a lower bound, we show that sample complexity of VA-LUCB is optimal up to a factor logarithmic in $H_{VA}$. Extensive experiments corroborate the dependence of the sample complexity on the various terms in $H_{VA}$. By comparing VA-LUCB's empirical performance to a close competitor RiskAverse-UCB-BAI by David et al. (2018), our experiments suggest that VA-LUCB has the lowest sample complexity for this class of risk-constrained best arm identification problems, especially for the riskiest instances.

Towards Adversarially Robust Deep Image Denoising

Jan 13, 2022

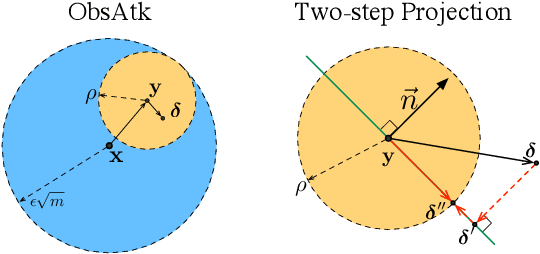

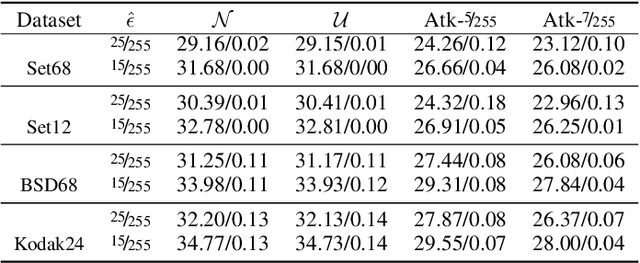

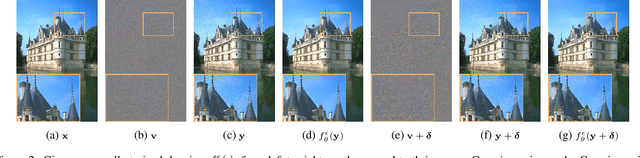

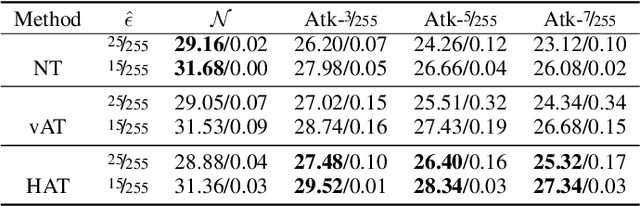

This work systematically investigates the adversarial robustness of deep image denoisers (DIDs), i.e, how well DIDs can recover the ground truth from noisy observations degraded by adversarial perturbations. Firstly, to evaluate DIDs' robustness, we propose a novel adversarial attack, namely Observation-based Zero-mean Attack ({\sc ObsAtk}), to craft adversarial zero-mean perturbations on given noisy images. We find that existing DIDs are vulnerable to the adversarial noise generated by {\sc ObsAtk}. Secondly, to robustify DIDs, we propose an adversarial training strategy, hybrid adversarial training ({\sc HAT}), that jointly trains DIDs with adversarial and non-adversarial noisy data to ensure that the reconstruction quality is high and the denoisers around non-adversarial data are locally smooth. The resultant DIDs can effectively remove various types of synthetic and adversarial noise. We also uncover that the robustness of DIDs benefits their generalization capability on unseen real-world noise. Indeed, {\sc HAT}-trained DIDs can recover high-quality clean images from real-world noise even without training on real noisy data. Extensive experiments on benchmark datasets, including Set68, PolyU, and SIDD, corroborate the effectiveness of {\sc ObsAtk} and {\sc HAT}.

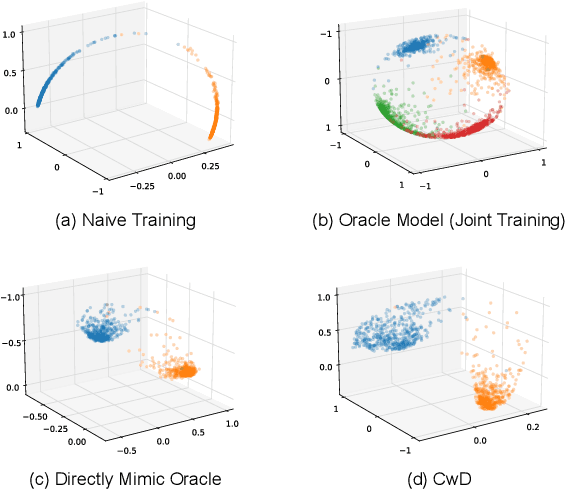

Mimicking the Oracle: An Initial Phase Decorrelation Approach for Class Incremental Learning

Jan 03, 2022

Class Incremental Learning (CIL) aims at learning a multi-class classifier in a phase-by-phase manner, in which only data of a subset of the classes are provided at each phase. Previous works mainly focus on mitigating forgetting in phases after the initial one. However, we find that improving CIL at its initial phase is also a promising direction. Specifically, we experimentally show that directly encouraging CIL Learner at the initial phase to output similar representations as the model jointly trained on all classes can greatly boost the CIL performance. Motivated by this, we study the difference between a na\"ively-trained initial-phase model and the oracle model. Specifically, since one major difference between these two models is the number of training classes, we investigate how such difference affects the model representations. We find that, with fewer training classes, the data representations of each class lie in a long and narrow region; with more training classes, the representations of each class scatter more uniformly. Inspired by this observation, we propose Class-wise Decorrelation (CwD) that effectively regularizes representations of each class to scatter more uniformly, thus mimicking the model jointly trained with all classes (i.e., the oracle model). Our CwD is simple to implement and easy to plug into existing methods. Extensive experiments on various benchmark datasets show that CwD consistently and significantly improves the performance of existing state-of-the-art methods by around 1\% to 3\%. Code will be released.

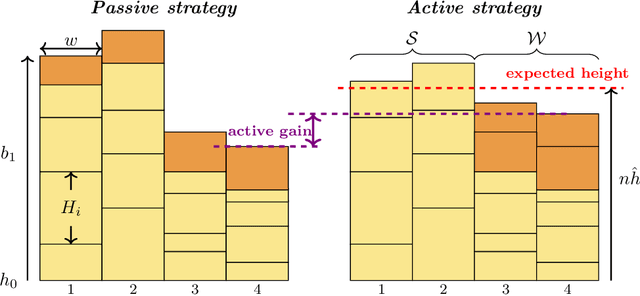

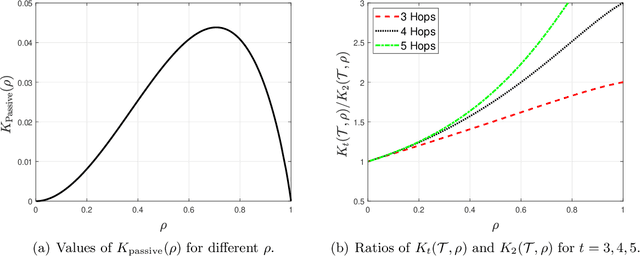

Active-LATHE: An Active Learning Algorithm for Boosting the Error Exponent for Learning Homogeneous Ising Trees

Oct 28, 2021

The Chow-Liu algorithm (IEEE Trans.~Inform.~Theory, 1968) has been a mainstay for the learning of tree-structured graphical models from i.i.d.\ sampled data vectors. Its theoretical properties have been well-studied and are well-understood. In this paper, we focus on the class of trees that are arguably even more fundamental, namely {\em homogeneous} trees in which each pair of nodes that forms an edge has the same correlation $\rho$. We ask whether we are able to further reduce the error probability of learning the structure of the homogeneous tree model when {\em active learning} or {\em active sampling of nodes or variables} is allowed. Our figure of merit is the {\em error exponent}, which quantifies the exponential rate of decay of the error probability with an increasing number of data samples. At first sight, an improvement in the error exponent seems impossible, as all the edges are statistically identical. We design and analyze an algorithm Active Learning Algorithm for Trees with Homogeneous Edge (Active-LATHE), which surprisingly boosts the error exponent by at least 40\% when $\rho$ is at least $0.8$. For all other values of $\rho$, we also observe commensurate, but more modest, improvements in the error exponent. Our analysis hinges on judiciously exploiting the minute but detectable statistical variation of the samples to allocate more data to parts of the graph in which we are less confident of being correct.

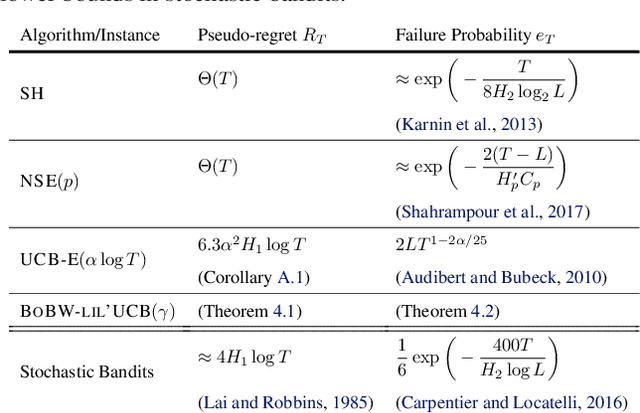

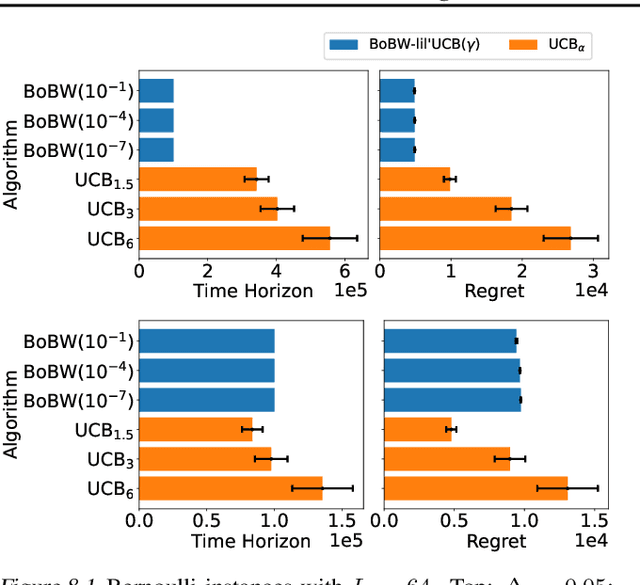

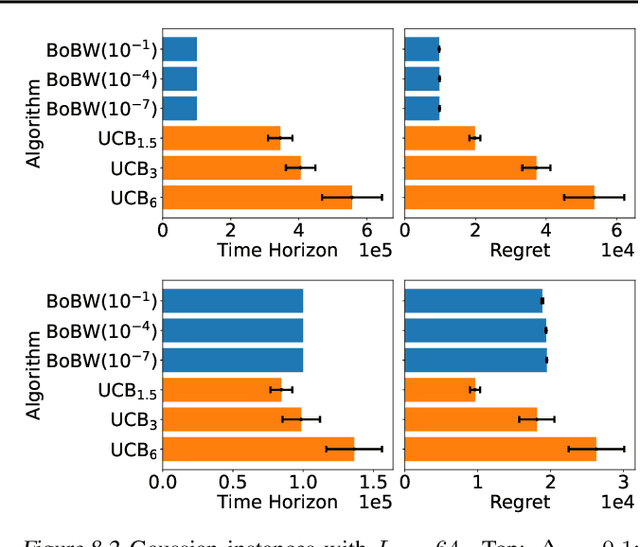

On the Pareto Frontier of Regret Minimization and Best Arm Identification in Stochastic Bandits

Oct 16, 2021

We study the Pareto frontier of two archetypal objectives in stochastic bandits, namely, regret minimization (RM) and best arm identification (BAI) with a fixed horizon. It is folklore that the balance between exploitation and exploration is crucial for both RM and BAI, but exploration is more critical in achieving the optimal performance for the latter objective. To make this precise, we first design and analyze the BoBW-lil'UCB$({\gamma})$ algorithm, which achieves order-wise optimal performance for RM or BAI under different values of ${\gamma}$. Complementarily, we show that no algorithm can simultaneously perform optimally for both the RM and BAI objectives. More precisely, we establish non-trivial lower bounds on the regret achievable by any algorithm with a given BAI failure probability. This analysis shows that in some regimes BoBW-lil'UCB$({\gamma})$ achieves Pareto-optimality up to constant or small terms. Numerical experiments further demonstrate that when applied to difficult instances, BoBW-lil'UCB outperforms a close competitor UCB$_{\alpha}$ (Degenne et al., 2019), which is designed for RM and BAI with a fixed confidence.

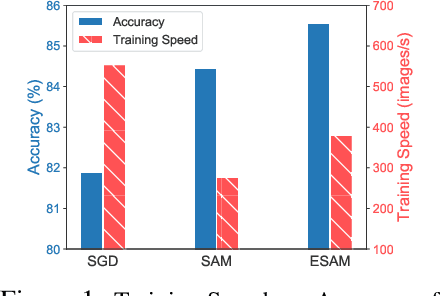

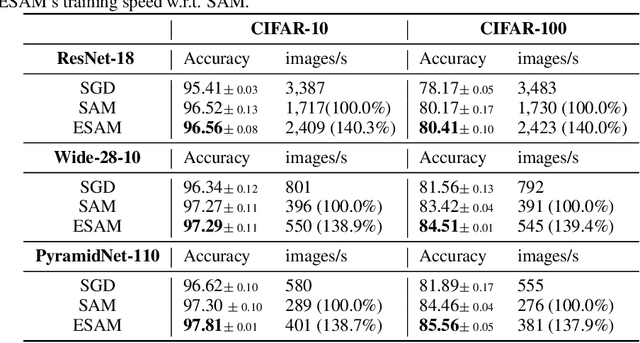

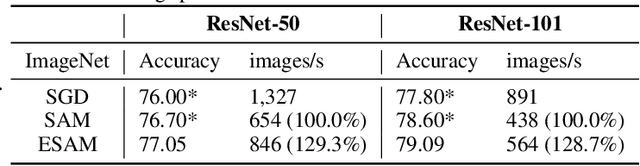

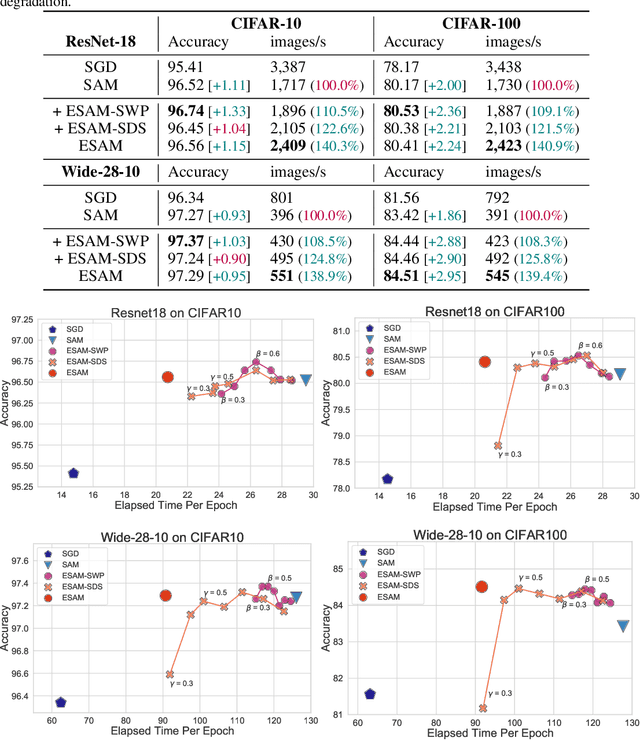

Efficient Sharpness-aware Minimization for Improved Training of Neural Networks

Oct 07, 2021

Overparametrized Deep Neural Networks (DNNs) often achieve astounding performances, but may potentially result in severe generalization error. Recently, the relation between the sharpness of the loss landscape and the generalization error has been established by Foret et al. (2020), in which the Sharpness Aware Minimizer (SAM) was proposed to mitigate the degradation of the generalization. Unfortunately, SAM s computational cost is roughly double that of base optimizers, such as Stochastic Gradient Descent (SGD). This paper thus proposes Efficient Sharpness Aware Minimizer (ESAM), which boosts SAM s efficiency at no cost to its generalization performance. ESAM includes two novel and efficient training strategies-StochasticWeight Perturbation and Sharpness-Sensitive Data Selection. In the former, the sharpness measure is approximated by perturbing a stochastically chosen set of weights in each iteration; in the latter, the SAM loss is optimized using only a judiciously selected subset of data that is sensitive to the sharpness. We provide theoretical explanations as to why these strategies perform well. We also show, via extensive experiments on the CIFAR and ImageNet datasets, that ESAM enhances the efficiency over SAM from requiring 100% extra computations to 40% vis-a-vis base optimizers, while test accuracies are preserved or even improved.

Information-Theoretic Generalization Bounds for Iterative Semi-Supervised Learning

Oct 03, 2021

We consider iterative semi-supervised learning (SSL) algorithms that iteratively generate pseudo-labels for a large amount unlabelled data to progressively refine the model parameters. In particular, we seek to understand the behaviour of the {\em generalization error} of iterative SSL algorithms using information-theoretic principles. To obtain bounds that are amenable to numerical evaluation, we first work with a simple model -- namely, the binary Gaussian mixture model. Our theoretical results suggest that when the class conditional variances are not too large, the upper bound on the generalization error decreases monotonically with the number of iterations, but quickly saturates. The theoretical results on the simple model are corroborated by extensive experiments on several benchmark datasets such as the MNIST and CIFAR datasets in which we notice that the generalization error improves after several pseudo-labelling iterations, but saturates afterwards.

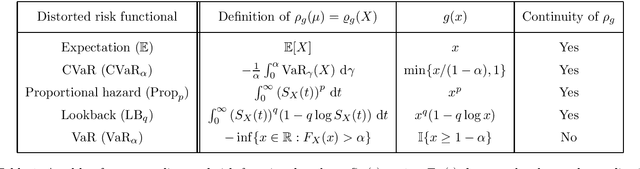

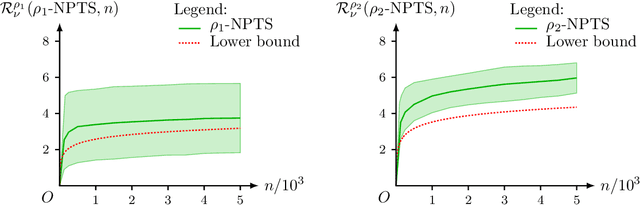

A Unifying Theory of Thompson Sampling for Continuous Risk-Averse Bandits

Aug 25, 2021

This paper unifies the design and simplifies the analysis of risk-averse Thompson sampling algorithms for the multi-armed bandit problem for a generic class of risk functionals \r{ho} that are continuous. Using the contraction principle in the theory of large deviations, we prove novel concentration bounds for these continuous risk functionals. In contrast to existing works in which the bounds depend on the samples themselves, our bounds only depend on the number of samples. This allows us to sidestep significant analytical challenges and unify existing proofs of the regret bounds of existing Thompson sampling-based algorithms. We show that a wide class of risk functionals as well as "nice" functions of them satisfy the continuity condition. Using our newly developed analytical toolkits, we analyse the algorithms $\rho$-MTS (for multinomial distributions) and $\rho$-NPTS (for bounded distributions) and prove that they admit asymptotically optimal regret bounds of risk-averse algorithms under the mean-variance, CVaR, and other ubiquitous risk measures, as well as a host of newly synthesized risk measures. Numerical simulations show that our bounds are reasonably tight vis-\`a-vis algorithm-independent lower bounds.

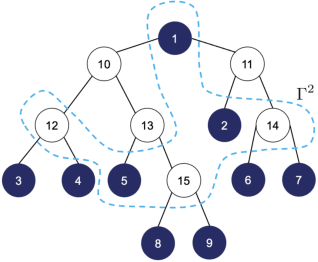

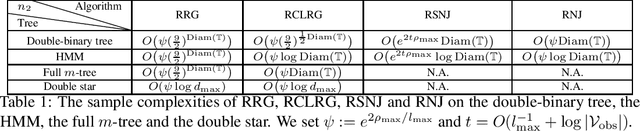

Robustifying Algorithms of Learning Latent Trees with Vector Variables

Jun 03, 2021

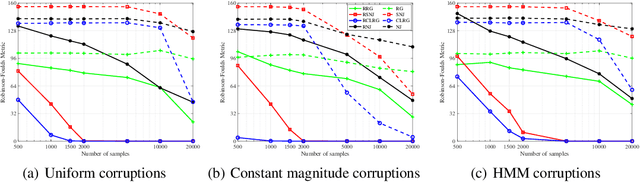

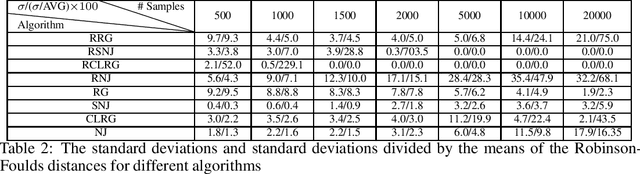

We consider learning the structures of Gaussian latent tree models with vector observations when a subset of them are arbitrarily corrupted. First, we present the sample complexities of Recursive Grouping (RG) and Chow-Liu Recursive Grouping (CLRG) without the assumption that the effective depth is bounded in the number of observed nodes, significantly generalizing the results in Choi et al. (2011). We show that Chow-Liu initialization in CLRG greatly reduces the sample complexity of RG from being exponential in the diameter of the tree to only logarithmic in the diameter for the hidden Markov model (HMM). Second, we robustify RG, CLRG, Neighbor Joining (NJ) and Spectral NJ (SNJ) by using the truncated inner product. These robustified algorithms can tolerate a number of corruptions up to the square root of the number of clean samples. Finally, we derive the first known instance-dependent impossibility result for structure learning of latent trees. The optimalities of the robust version of CLRG and NJ are verified by comparing their sample complexities and the impossibility result.

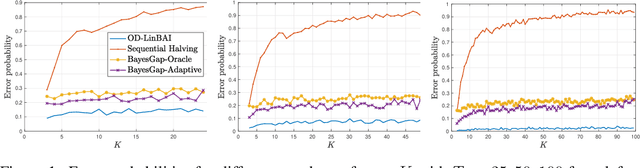

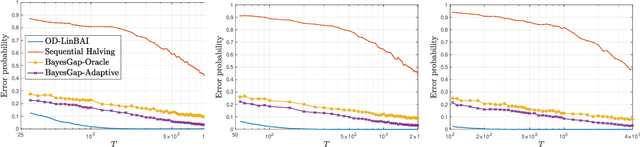

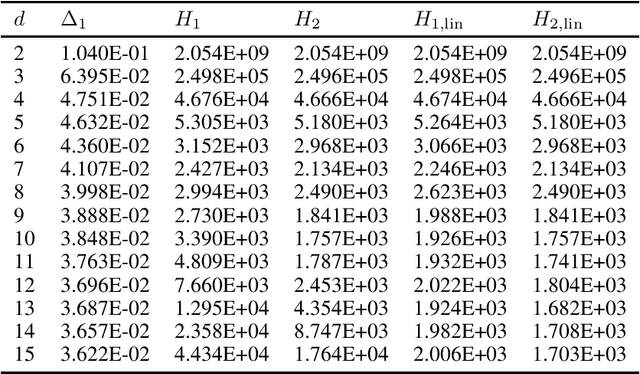

Towards Minimax Optimal Best Arm Identification in Linear Bandits

May 27, 2021

We study the problem of best arm identification in linear bandits in the fixed-budget setting. By leveraging properties of the G-optimal design and incorporating it into the arm allocation rule, we design a parameter-free algorithm, Optimal Design-based Linear Best Arm Identification (OD-LinBAI). We provide a theoretical analysis of the failure probability of OD-LinBAI. While the performances of existing methods (e.g., BayesGap) depend on all the optimality gaps, OD-LinBAI depends on the gaps of the top $d$ arms, where $d$ is the effective dimension of the linear bandit instance. Furthermore, we present a minimax lower bound for this problem. The upper and lower bounds show that OD-LinBAI is minimax optimal up to multiplicative factors in the exponent. Finally, numerical experiments corroborate our theoretical findings.