Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeORACLE-SWE: Quantifying the Contribution of Oracle Information Signals on SWE Agents

Apr 09, 2026Recent advances in language model (LM) agents have significantly improved automated software engineering (SWE). Prior work has proposed various agentic workflows and training strategies as well as analyzed failure modes of agentic systems on SWE tasks, focusing on several contextual information signals: Reproduction Test, Regression Test, Edit Location, Execution Context, and API Usage. However, the individual contribution of each signal to overall success remains underexplored, particularly their ideal contribution when intermediate information is perfectly obtained. To address this gap, we introduce Oracle-SWE, a unified method to isolate and extract oracle information signals from SWE benchmarks and quantify the impact of each signal on agent performance. To further validate the pattern, we evaluate the performance gain of signals extracted by strong LMs when provided to a base agent, approximating real-world task-resolution settings. These evaluations aim to guide research prioritization for autonomous coding systems.

RepoLaunch: Automating Build&Test Pipeline of Code Repositories on ANY Language and ANY Platform

Mar 05, 2026Building software repositories typically requires significant manual effort. Recent advances in large language model (LLM) agents have accelerated automation in software engineering (SWE). We introduce RepoLaunch, the first agent capable of automatically resolving dependencies, compiling source code, and extracting test results for repositories across arbitrary programming languages and operating systems. To demonstrate its utility, we further propose a fully automated pipeline for SWE dataset creation, where task design is the only human intervention. RepoLaunch automates the remaining steps, enabling scalable benchmarking and training of coding agents and LLMs. Notably, several works on agentic benchmarking and training have recently adopted RepoLaunch for automated task generation.

The Adaptive Multi-Factor Model and the Financial Market

Aug 19, 2021

Modern evolvements of the technologies have been leading to a profound influence on the financial market. The introduction of constituents like Exchange-Traded Funds, and the wide-use of advanced technologies such as algorithmic trading, results in a boom of the data which provides more opportunities to reveal deeper insights. However, traditional statistical methods always suffer from the high-dimensional, high-correlation, and time-varying instinct of the financial data. In this dissertation, we focus on developing techniques to stress these difficulties. With the proposed methodologies, we can have more interpretable models, clearer explanations, and better predictions.

* PhD thesis

Clustering Structure of Microstructure Measures

Jul 05, 2021

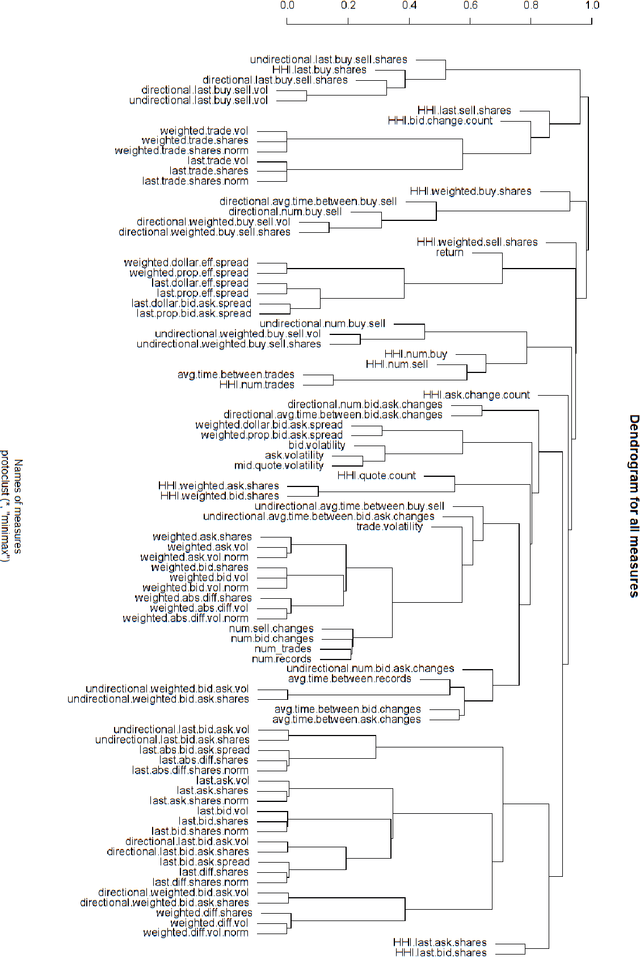

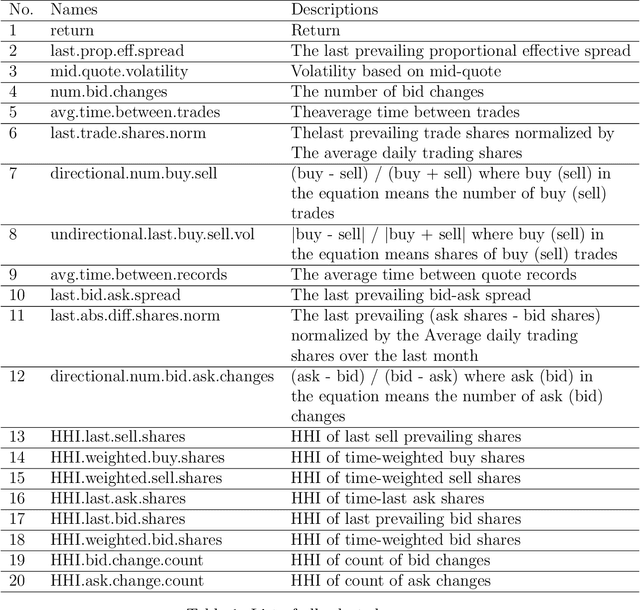

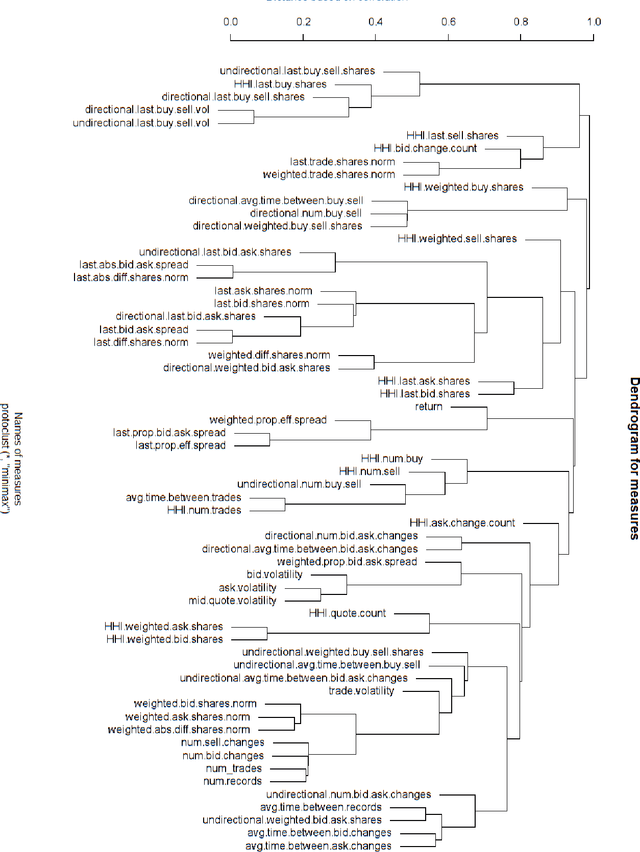

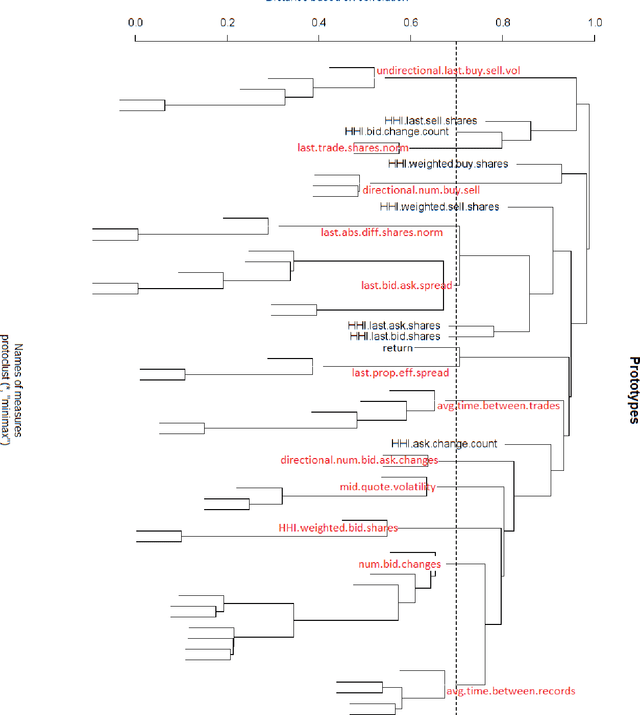

This paper builds the clustering model of measures of market microstructure features which are popular in predicting the stock returns. In a 10-second time frequency, we study the clustering structure of different measures to find out the best ones for predicting. In this way, we can predict more accurately with a limited number of predictors, which removes the noise and makes the model more interpretable.

A News-based Machine Learning Model for Adaptive Asset Pricing

Jun 13, 2021

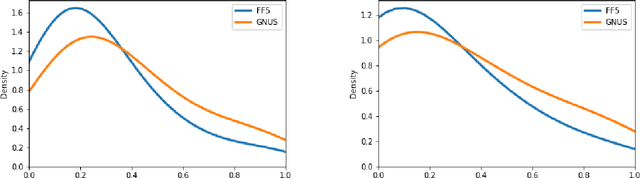

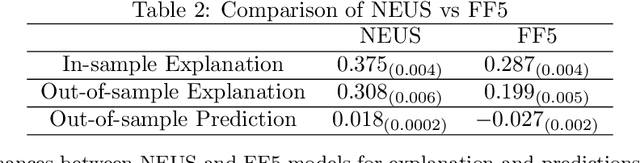

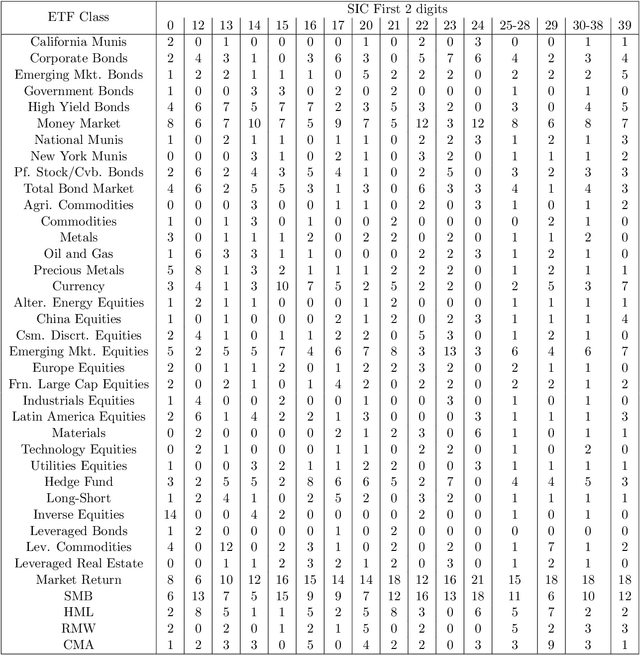

The paper proposes a new asset pricing model -- the News Embedding UMAP Selection (NEUS) model, to explain and predict the stock returns based on the financial news. Using a combination of various machine learning algorithms, we first derive a company embedding vector for each basis asset from the financial news. Then we obtain a collection of the basis assets based on their company embedding. After that for each stock, we select the basis assets to explain and predict the stock return with high-dimensional statistical methods. The new model is shown to have a significantly better fitting and prediction power than the Fama-French 5-factor model.

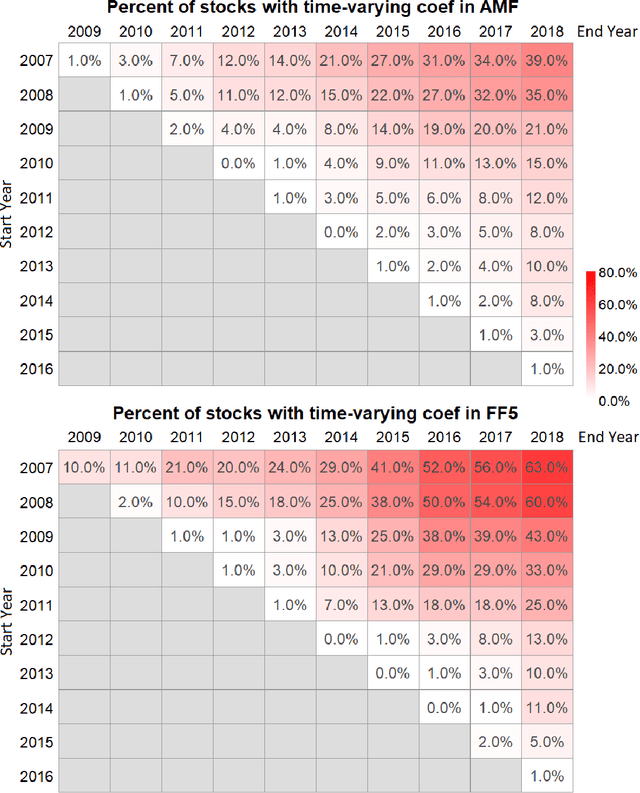

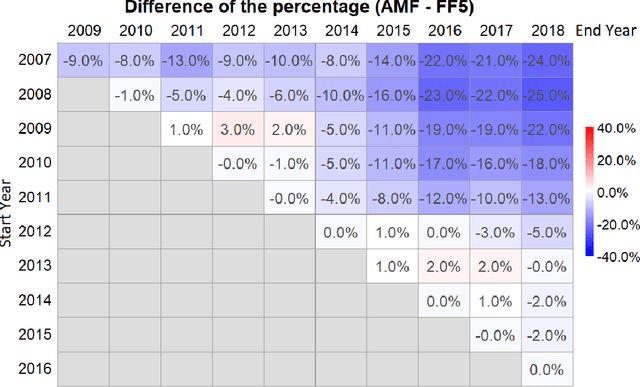

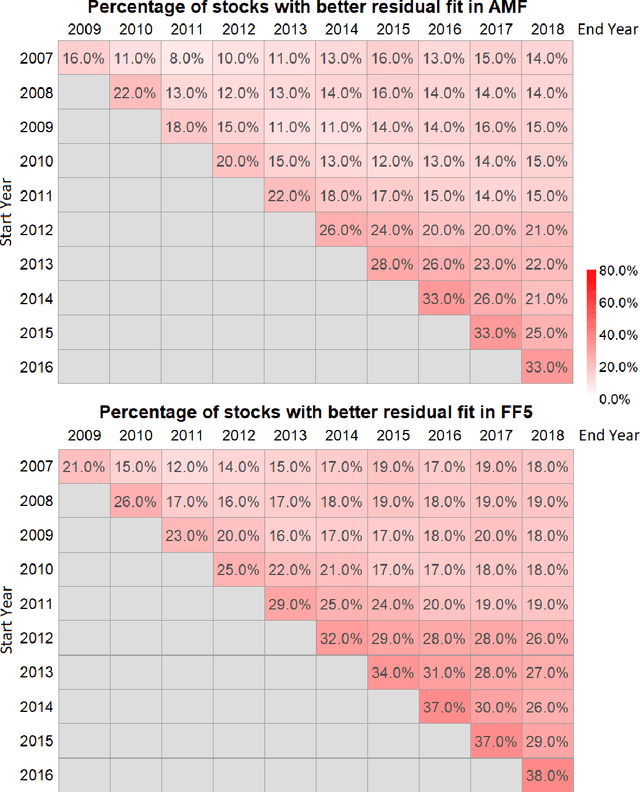

Time-Invariance Coefficients Tests with the Adaptive Multi-Factor Model

Nov 09, 2020

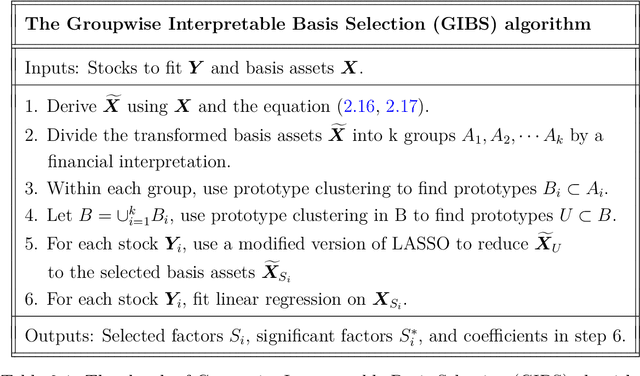

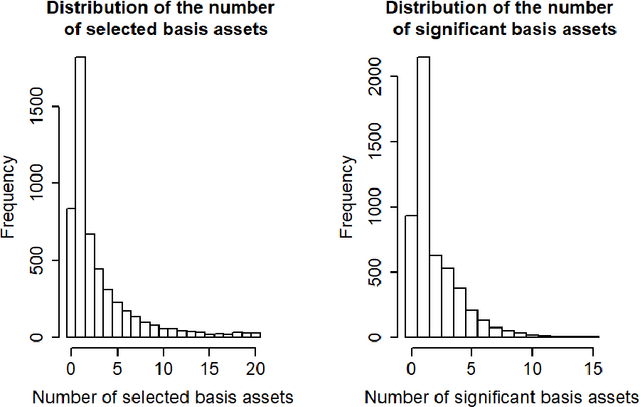

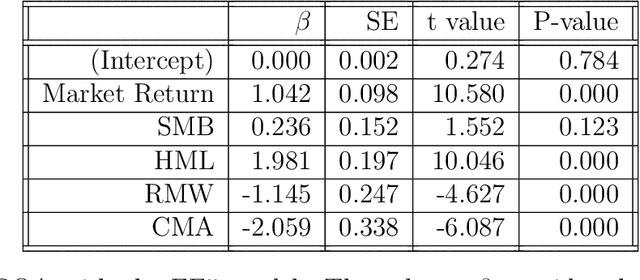

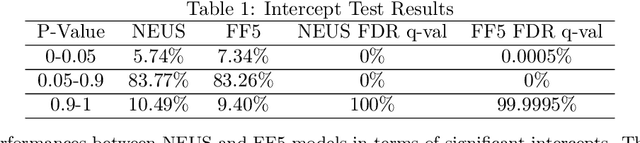

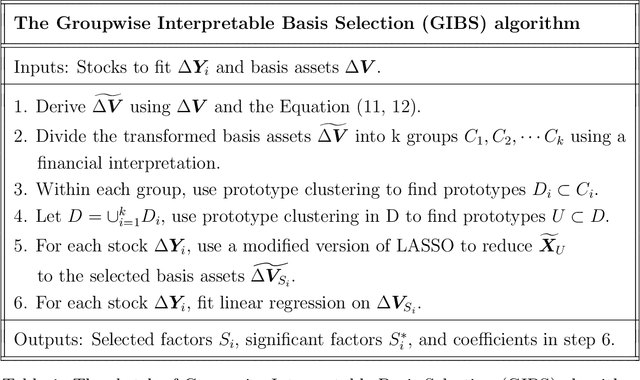

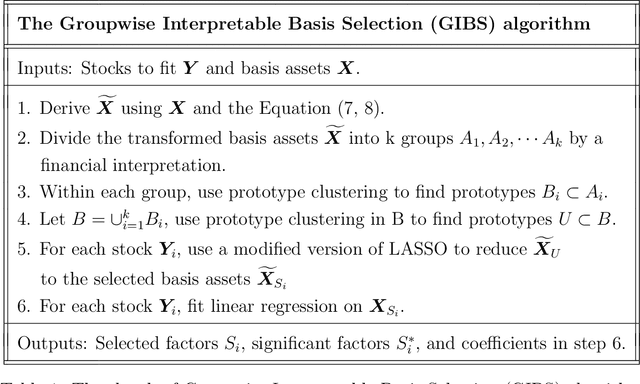

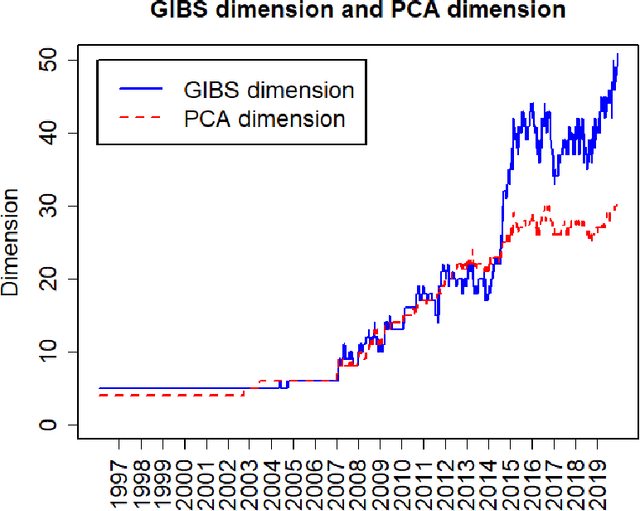

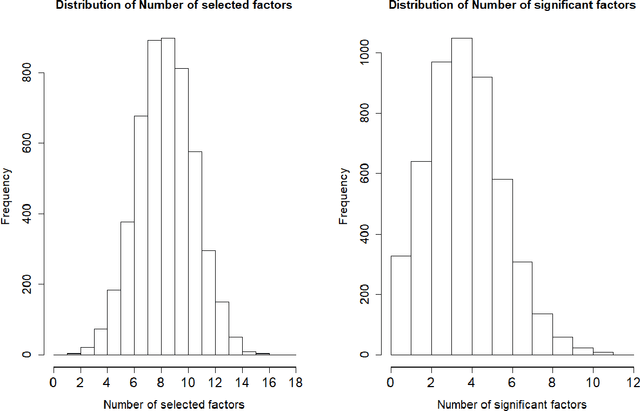

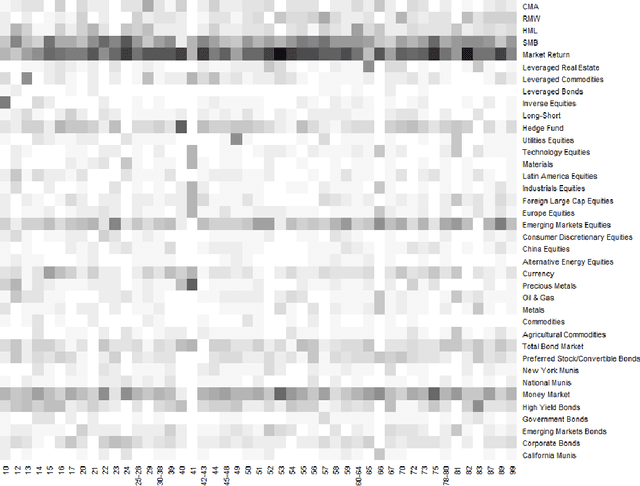

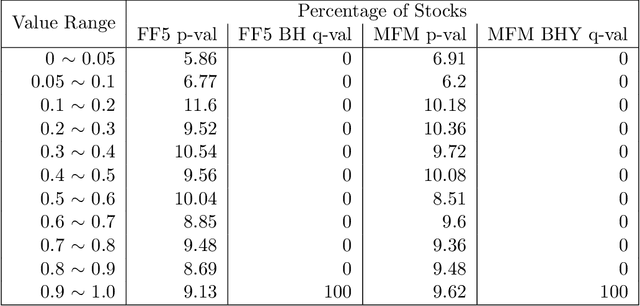

The purpose of this paper is to test the multi-factor beta model implied by the generalized arbitrage pricing theory (APT) and the Adaptive Multi-Factor (AMF) model with the Groupwise Interpretable Basis Selection (GIBS) algorithm, without imposing the exogenous assumption of constant betas. The intercept (arbitrage) tests validate both the AMF and the Fama-French 5-factor (FF5) model. We do the time-invariance tests for the betas for both the AMF model and the FF5 in various time periods. We show that for nearly all time periods with length less than 6 years, the beta coefficients are time-invariant for the AMF model, but not the FF5 model. The beta coefficients are time-varying for both AMF and FF5 models for longer time periods. Therefore, using the dynamic AMF model with a decent rolling window (such as 5 years) is more powerful and stable than the FF5 model.

Low-volatility Anomaly and the Adaptive Multi-Factor Model

Mar 16, 2020

The paper explains the low-volatility anomaly from a new perspective. We use the Adaptive Multi-Factor (AMF) model estimated by the Groupwise Interpretable Basis Selection (GIBS) algorithm to find the basis assets significantly related to each of the portfolios. The AMF results show that the two portfolios load on very different factors, which indicates that the volatility is not an independent measure of risk, but are related to the basis assets and risk factors in the related industries. It is the performance of the loaded factors that results in the low-volatility anomaly. The out-performance of the low-volatility portfolio may not because of its low-risk (which contradicts the risk-premium theory), but because of the out-performance of the risk factors the low-volatility portfolio is loaded on. Also, we compare the AMF model with the traditional Fama-French 5-factor (FF5) model in various aspects, which shows the superior performance of the AMF model over FF5 in many perspectives.

High Dimensional Estimation and Multi-Factor Models

Jul 16, 2018

This paper re-investigates the estimation of multiple factor models relaxing the convention that the number of factors is small and using a new approach for identifying factors. We first obtain the collection of all possible factors and then provide a simultaneous test, security by security, of which factors are significant. Since the collection of risk factors is large and highly correlated, high-dimension methods (including the LASSO and prototype clustering) have to be used. The multi-factor model is shown to have a significantly better fit than the Fama-French 5-factor model. Robustness tests are also provided.