Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeScalar-Stepsize Nonuniform Monte Carlo Optimistic Policy Iteration: A Certified Counterexample

Jun 14, 2026Tsitsiklis proved convergence of Monte Carlo optimistic policy iteration under a uniform update structure and identified nonuniform update frequencies as a delicate obstruction. We give a certified negative answer for the natural scalar-stepsize, unnormalized asynchronous state-value recursion with fixed nonuniform state-selection probabilities. In a three-state, two-action discounted MDP, the nonuniform update frequencies induce a diagonally scaled greedy-policy mean field with a certified nonconstant attracting hybrid periodic orbit. With a bounded unbiased geometric-horizon estimator and Robbins--Monro stepsizes, the original stochastic recursion remains trapped near the cycle with positive probability and therefore fails to converge. The example pinpoints a geometric obstruction: uniform sampling gives radial residual contraction, whereas scalar nonuniform sampling anisotropically distorts the residual dynamics and can generate switched attracting cycles.

Partial Fairness Awareness: Belief-Guided Strategic Mechanism for Strategic Agents

May 30, 2026Strategic machine learning investigates scenarios where agents manipulate their features to receive favorable decisions from predictive models. To address fairness concerns intrinsic to strategic classification, recent work has introduced group-specific fairness constraints. However, current fairness-aware approaches face a fundamental dilemma in the issue of fairness exposure: making these constraints public enables strategic manipulation and can lead to fairness reversal, while keeping them hidden may reduce social welfare and discourage genuine improvement. To fill this gap, we subsequently propose the problem of partial fairness awareness (PFA), as our theoretical analysis informs that such a dilemma can be mitigated by releasing the candidate set of fairness constraints and concealing the grounding constraint. To be specific, we introduce a belief-guided strategic mechanism, wherein agents iteratively interact with the decision system and maintain a belief distribution over the candidate set of fairness constraints. This belief-guided process enables agents, through iterative interaction and feedback, to update their belief distribution over the candidate set, thereby gradually aligning their belief with the grounding fairness constraint employed by the system. Extensive experiments on real-world and synthetic datasets demonstrate that PFA achieves lower group fairness gaps, higher acceptance of truly qualified individuals, and more stable outcomes compared to fully public or private fairness regimes.

Beyond Independent Manipulation: Individual Fairness-aware Strategic Classification with Peer Imitation

May 30, 2026Strategic classification (SC) investigates scenarios where agents manipulate their features to obtain favorable decisions from predictive models. Existing fairness-aware SC approaches primarily focus on group fairness and typically assume that agents respond independently. However, when individual fairness is required, ensuring similar individuals receive similar outcomes, agents' manipulation becomes interdependent: an agent's preferred manipulation depends on the neighborhoods' outcomes. This induces a mismatch between classical SC formulations and fairness-aware decision settings, where independent models no longer accurately characterize strategic manipulations. To address this issue, we introduce individual fairness-aware strategic classification (IFSC), a framework that models peer-driven manipulation arising from individual fairness, where agents imitate nearby positively decided peers to obtain favorable outcomes. IFSC characterizes strategic manipulation as similarity-based imitation toward visible accepted peers and learns classifiers under the resulting post-manipulation distributions. To account for uncertainty in peer observability, IFSC employs a robust learning process that introduces stochastic perturbations during manipulation simulation. Experiments on synthetic and real-world datasets demonstrate that IFSC improves individual-fairness consistency and mitigates imitation-induced distortions.

When Tabular Foundation Models Meet Strategic Tabular Data: A Prior Alignment Approach

May 19, 2026Tabular foundation models based on pretrained prior-data fitted networks~(PFNs) have shown strong generalization on diverse tabular tasks, but they are typically designed for \emph{non-strategic} settings where data distributions are independent of deployed classifiers. In many real-world decision scenarios, however, individuals may strategically modify their features after deployment to obtain favorable outcomes, inducing a post-deployment distribution shift. This paper studies whether PFN-style tabular foundation models can generalize to such \emph{strategic} tabular data. We show that strategic manipulation creates a mismatch between the non-strategic prior learned during pretraining and the post-manipulation strategic prior, which leads to systematic prediction bias. To address this issue, we propose \textbf{Strategic Prior-data Fitted Network}~\textit{(SPN)}, an inference-time strategy-aware framework that adapts tabular foundation models to strategic environments without retraining. SPN constructs strategic in-context examples to approximate post-manipulation inputs and aligns PFN predictions with the induced strategic distribution. Experiments on real-world and synthetic tabular datasets show that SPN consistently improves robustness and predictive performance under strategic manipulation compared with both tabular foundation models and classical tabular methods.

Beyond Rational Illusion: Behaviorally Realistic Strategic Classification

May 19, 2026Strategic classification(SC) studies the interaction between decision models and agents who strategically manipulate their features for favorable outcomes. Existing SC frameworks typically rely on the idealized assumption that agents are strictly rational. However, evidence from behavioral economics and psychology consistently shows that real-world decision-making is often shaped by cognitive biases, deviating from pure rationality. To formalize this limitation, we identify and define a new problem setting, termed the behaviorally realistic strategic classification problem, where agents' strategic manipulations deviate from full rationality due to psychological biases. Motivated by the identified limitation, we propose the Prospect-Guided Strategic Framework (Pro-SF) to address the problem, a principled framework grounded in prospect theory to model and learn under behaviorally realistic strategic responses. Specifically, to capture behaviorally realistic strategic manipulations, our framework reformulates the Stackelberg-style interaction between agents and the decision-maker by incorporating three key mechanisms inspired by prospect theory, including the asymmetry between benefits and costs, different subjective reference points, and non-rational probability distortion. Experiments on synthetic and real-world datasets establish Pro-SF as a behaviorally grounded approach to strategic classification, bridging machine learning and behavioral economics for more reliable deployment in the real world.

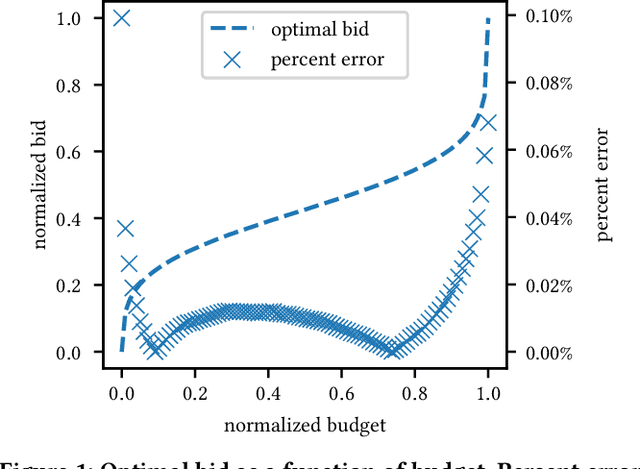

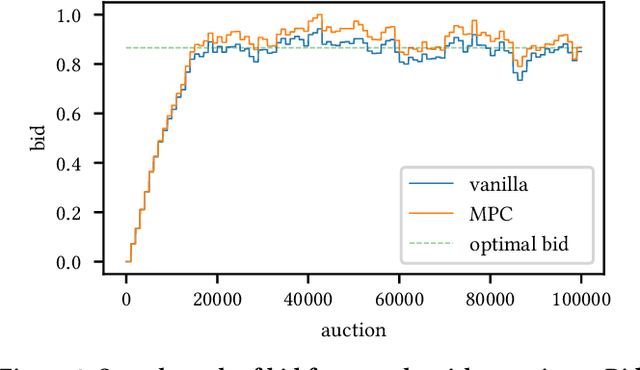

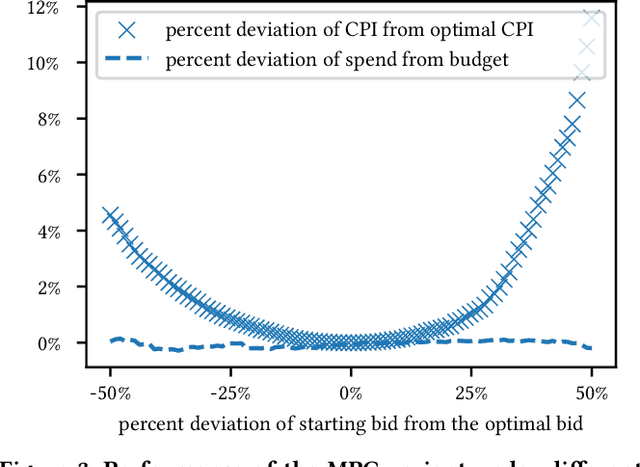

A Lightweight MPC Bidding Framework for Brand Auction Ads

Mar 08, 2026Brand advertising plays a critical role in building long-term consumer awareness and loyalty, making it a key objective for advertisers across digital platforms. Although real-time bidding has been extensively studied, there is limited literature on algorithms specifically tailored for brand auction ads that fully leverage their unique characteristics. In this paper, we propose a lightweight Model Predictive Control (MPC) framework designed for brand advertising campaigns, exploiting the inherent attributes of brand ads -- such as stable user engagement patterns and fast feedback loops -- to simplify modeling and improve efficiency. Our approach utilizes online isotonic regression to construct monotonic bid-to-spend and bid-to-conversion models directly from streaming data, eliminating the need for complex machine learning models. The algorithm operates fully online with low computational overhead, making it highly practical for real-world deployment. Simulation results demonstrate that our approach significantly improves spend efficiency and cost control compared to baseline strategies, providing a scalable and easily implementable solution for modern brand advertising platforms.

Breaking the Gradient Barrier: Unveiling Large Language Models for Strategic Classification

Nov 10, 2025Strategic classification~(SC) explores how individuals or entities modify their features strategically to achieve favorable classification outcomes. However, existing SC methods, which are largely based on linear models or shallow neural networks, face significant limitations in terms of scalability and capacity when applied to real-world datasets with significantly increasing scale, especially in financial services and the internet sector. In this paper, we investigate how to leverage large language models to design a more scalable and efficient SC framework, especially in the case of growing individuals engaged with decision-making processes. Specifically, we introduce GLIM, a gradient-free SC method grounded in in-context learning. During the feed-forward process of self-attention, GLIM implicitly simulates the typical bi-level optimization process of SC, including both the feature manipulation and decision rule optimization. Without fine-tuning the LLMs, our proposed GLIM enjoys the advantage of cost-effective adaptation in dynamic strategic environments. Theoretically, we prove GLIM can support pre-trained LLMs to adapt to a broad range of strategic manipulations. We validate our approach through experiments with a collection of pre-trained LLMs on real-world and synthetic datasets in financial and internet domains, demonstrating that our GLIM exhibits both robustness and efficiency, and offering an effective solution for large-scale SC tasks.

Bidding Agent Design in the LinkedIn Ad Marketplace

Feb 25, 2022

We establish a general optimization framework for the design of automated bidding agent in dynamic online marketplaces. It optimizes solely for the buyer's interest and is agnostic to the auction mechanism imposed by the seller. As a result, the framework allows, for instance, the joint optimization of a group of ads across multiple platforms each running its own auction format. Bidding strategy derived from this framework automatically guarantees the optimality of budget allocation across ad units and platforms. Common constraints such as budget delivery schedule, return on investments and guaranteed results, directly translates to additional parameters in the bidding formula. We share practical learnings of the deployed bidding system in the LinkedIn ad marketplace based on this framework.

On the convergence of optimistic policy iteration for stochastic shortest path problem

Aug 30, 2018In this paper, we prove some convergence results of a special case of optimistic policy iteration algorithm for stochastic shortest path problem. We consider both Monte Carlo and $TD(\lambda)$ methods for the policy evaluation step under the condition that the termination state will eventually be reached almost surely.