Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeQuantum Reservoir Computing and Risk Bounds

Jan 15, 2025We propose a way to bound the generalisation errors of several classes of quantum reservoirs using the Rademacher complexity. We give specific, parameter-dependent bounds for two particular quantum reservoir classes. We analyse how the generalisation bounds scale with growing numbers of qubits. Applying our results to classes with polynomial readout functions, we find that the risk bounds converge in the number of training samples. The explicit dependence on the quantum reservoir and readout parameters in our bounds can be used to control the generalisation error to a certain extent. It should be noted that the bounds scale exponentially with the number of qubits $n$. The upper bounds on the Rademacher complexity can be applied to other reservoir classes that fulfill a few hypotheses on the quantum dynamics and the readout function.

On the challenges of using D-Wave computers to sample Boltzmann Random Variables

Dec 01, 2021Sampling random variables following a Boltzmann distribution is an NP-hard problem involved in various applications such as training of \textit{Boltzmann machines}, a specific kind of neural network. Several attempts have been made to use a D-Wave quantum computer to sample such a distribution, as this could lead to significant speedup in these applications. Yet, at present, several challenges remain to efficiently perform such sampling. We detail the various obstacles and explain the remaining difficulties in solving the sampling problem on a D-wave machine.

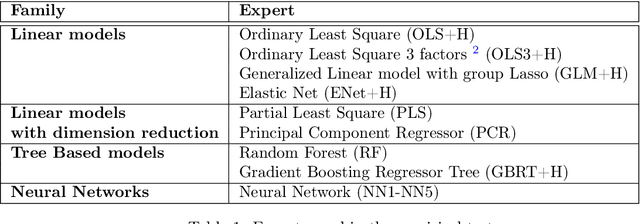

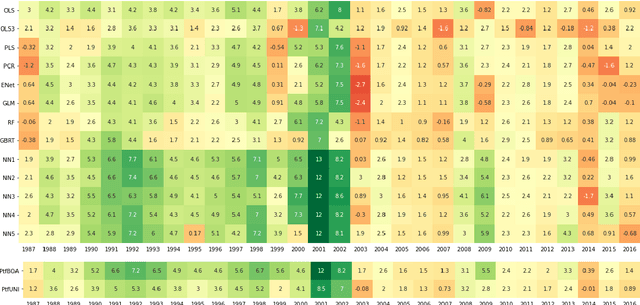

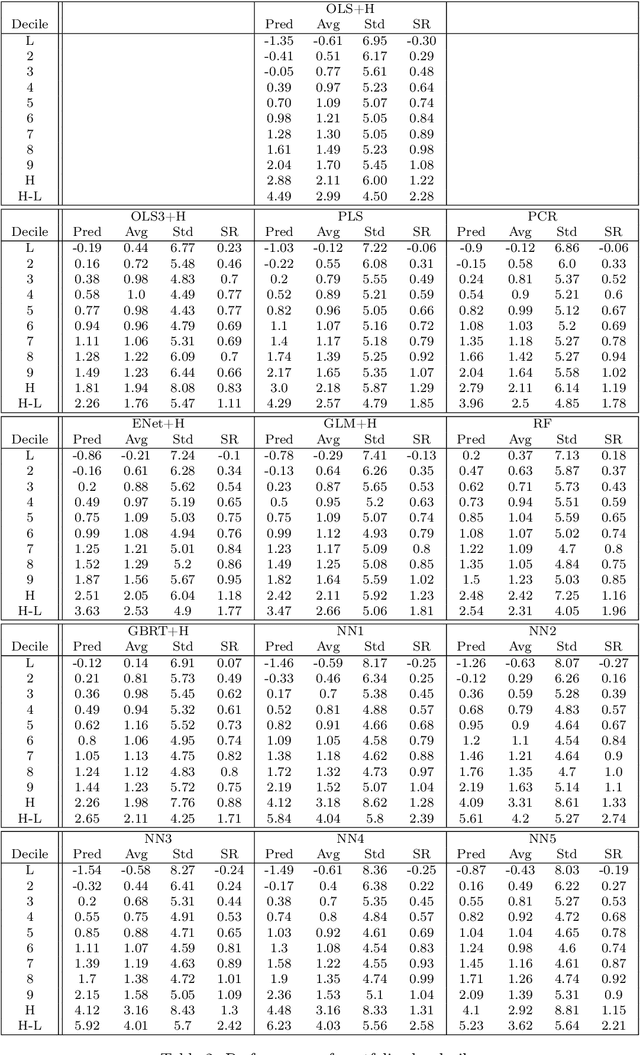

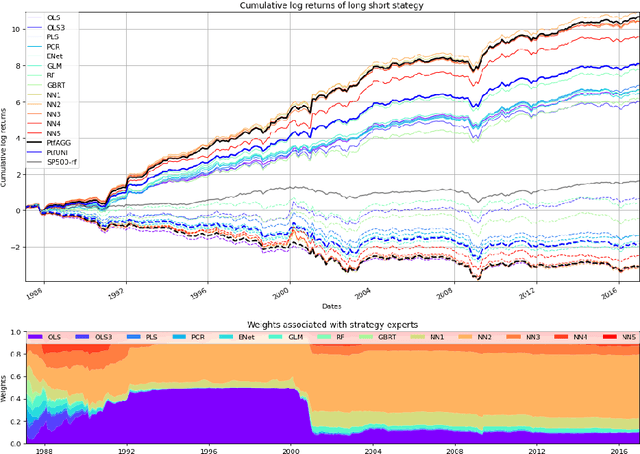

Expert Aggregation for Financial Forecasting

Dec 01, 2021

Machine learning algorithms dedicated to financial time series forecasting have gained a lot of interest over the last few years. One difficulty lies in the choice between several algorithms, as their estimation accuracy may be unstable through time. In this paper, we propose to apply an online aggregation-based forecasting model combining several machine learning techniques to build a portfolio which dynamically adapts itself to market conditions. We apply this aggregation technique to the construction of a long-short-portfolio of individual stocks ranked on their financial characteristics and we demonstrate how aggregation outperforms single algorithms both in terms of performances and of stability.

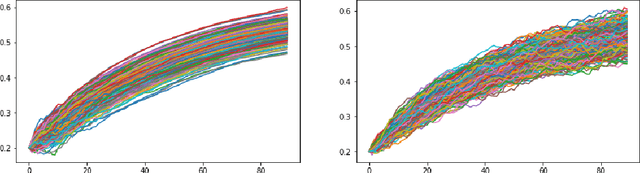

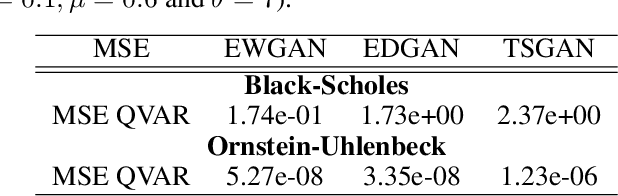

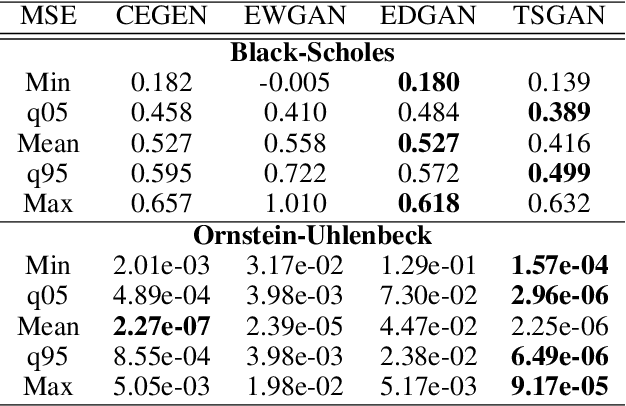

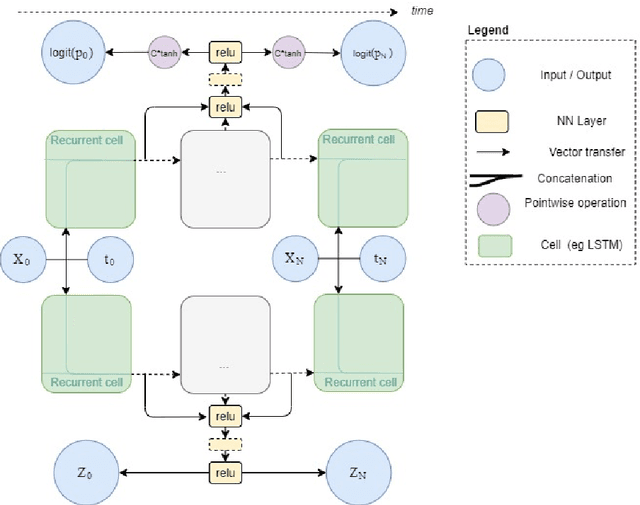

Conditional Versus Adversarial Euler-based Generators For Time Series

Feb 10, 2021

We introduce new generative models for time series based on Euler discretization that do not require any pre-stationarization procedure. Specifically, we develop two GAN based methods, relying on the adaptation of Wasserstein GANs (Arjovsky et al., 2017) and DVD GANs (Clark et al., 2019b) to time series. Alternatively, we consider a conditional Euler Generator (CEGEN) minimizing a distance between the induced conditional densities. In the context of It\^o processes, we theoretically validate this approach and demonstrate using the Bures metric that reaching a low loss level provides accurate estimations for both the drift and the volatility terms of the underlying process. Tests on simple models show how the Euler discretization and the use of Wasserstein distance allow the proposed GANs and (more considerably) CEGEN to outperform state-of-the-art Time Series GAN generation( Yoon et al., 2019b) on time structure metrics. In higher dimensions we observe that CEGEN manages to get the correct covariance structures. Finally we illustrate how our model can be combined to a Monte Carlo simulator in a low data context by using a transfer learning technique

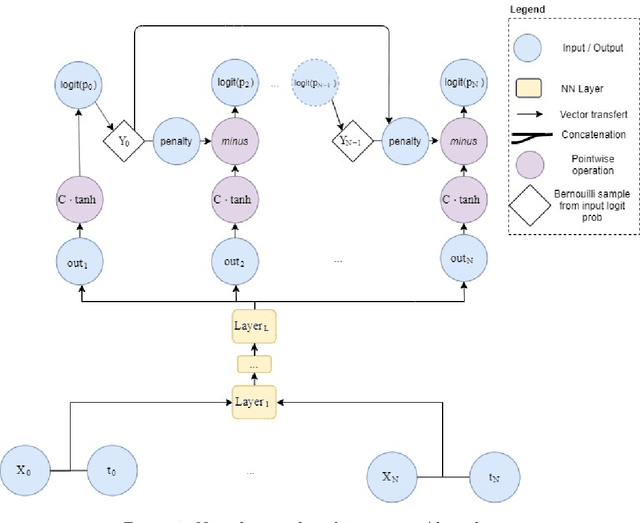

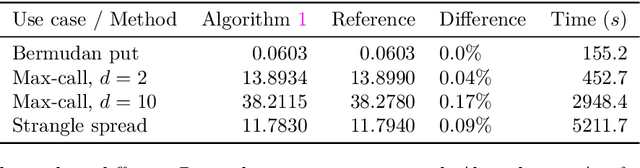

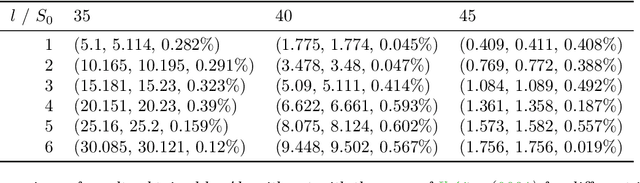

Deep combinatorial optimisation for optimal stopping time problems and stochastic impulse control. Application to swing options pricing and fixed transaction costs options hedging

Jan 30, 2020

A new method for stochastic control based on neural networks and using randomisation of discrete random variables is proposed and applied to optimal stopping time problems. Numerical tests are done on the pricing of American and swing options. An extension to impulse control problems is described and applied to options hedging under fixed transaction costs. The proposed algorithms seem to be competitive with the best existing algorithms both in terms of precision and in terms of computation time.

Machine Learning for semi linear PDEs

Sep 20, 2018Recent machine learning algorithms dedicated to solving semi-linear PDEs are improved by using different neural network architectures and different parameterizations. These algorithms are compared to a new one that solves a fixed point problem by using deep learning techniques. This new algorithm appears to be competitive in terms of accuracy with the best existing algorithms.