Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeExpert Aggregation for Financial Forecasting

Dec 01, 2021

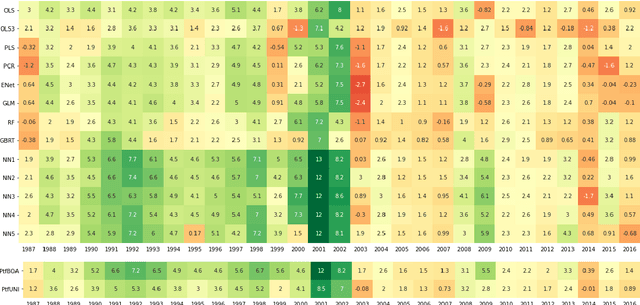

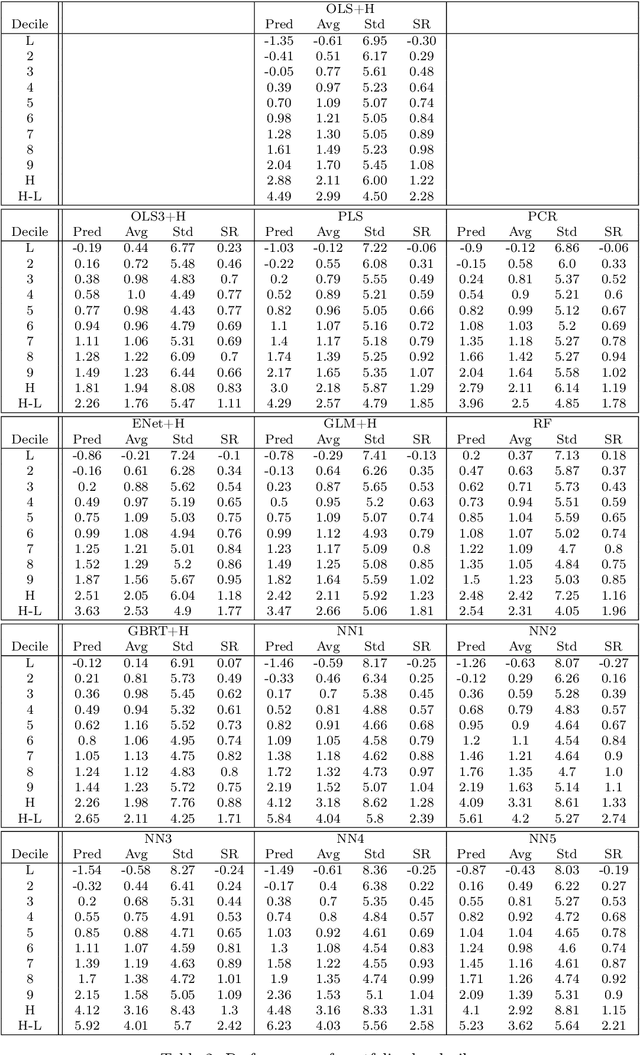

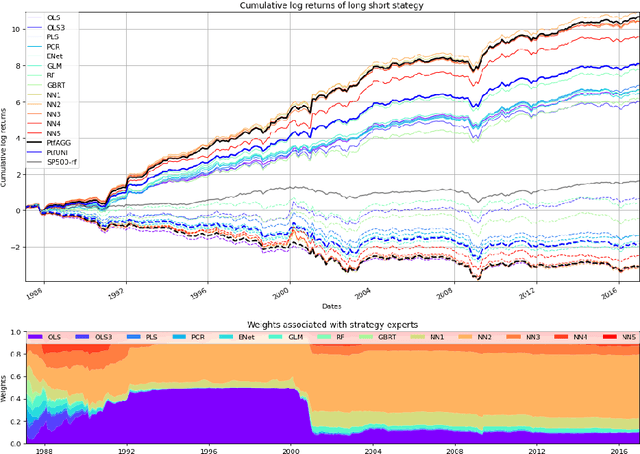

Machine learning algorithms dedicated to financial time series forecasting have gained a lot of interest over the last few years. One difficulty lies in the choice between several algorithms, as their estimation accuracy may be unstable through time. In this paper, we propose to apply an online aggregation-based forecasting model combining several machine learning techniques to build a portfolio which dynamically adapts itself to market conditions. We apply this aggregation technique to the construction of a long-short-portfolio of individual stocks ranked on their financial characteristics and we demonstrate how aggregation outperforms single algorithms both in terms of performances and of stability.

Via