Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeDeep combinatorial optimisation for optimal stopping time problems and stochastic impulse control. Application to swing options pricing and fixed transaction costs options hedging

Paper and Code

Jan 30, 2020

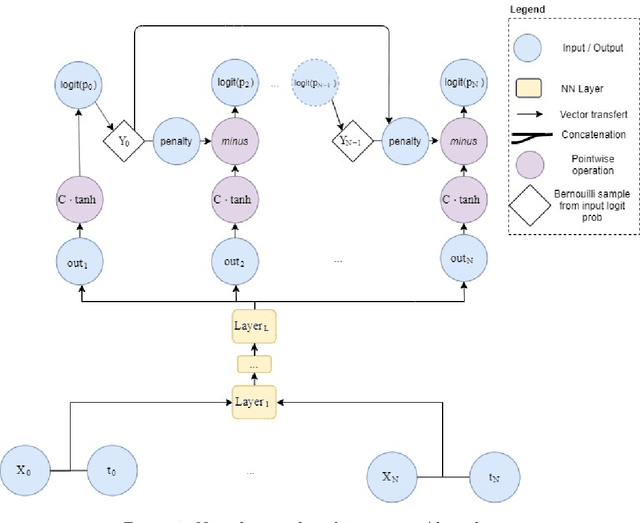

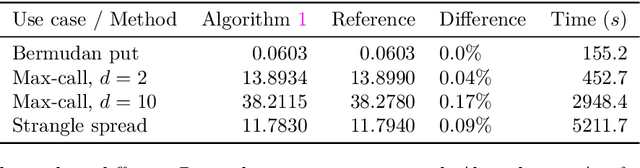

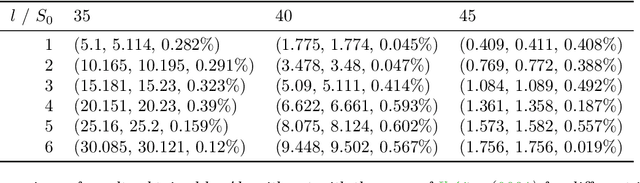

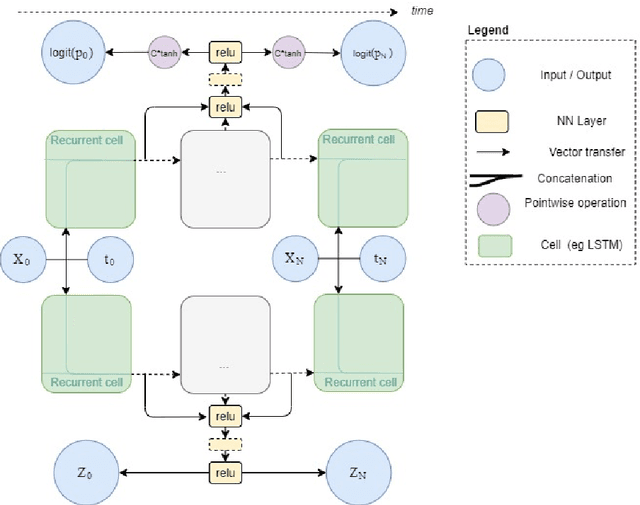

A new method for stochastic control based on neural networks and using randomisation of discrete random variables is proposed and applied to optimal stopping time problems. Numerical tests are done on the pricing of American and swing options. An extension to impulse control problems is described and applied to options hedging under fixed transaction costs. The proposed algorithms seem to be competitive with the best existing algorithms both in terms of precision and in terms of computation time.

View paper on