Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeAmortised and provably-robust simulation-based inference

Feb 17, 2026Complex simulator-based models are now routinely used to perform inference across the sciences and engineering, but existing inference methods are often unable to account for outliers and other extreme values in data which occur due to faulty measurement instruments or human error. In this paper, we introduce a novel approach to simulation-based inference grounded in generalised Bayesian inference and a neural approximation of a weighted score-matching loss. This leads to a method that is both amortised and provably robust to outliers, a combination not achieved by existing approaches. Furthermore, through a carefully chosen conditional density model, we demonstrate that inference can be further simplified and performed without the need for Markov chain Monte Carlo sampling, thereby offering significant computational advantages, with complexity that is only a small fraction of that of current state-of-the-art approaches.

BayesSum: Bayesian Quadrature in Discrete Spaces

Dec 18, 2025This paper addresses the challenging computational problem of estimating intractable expectations over discrete domains. Existing approaches, including Monte Carlo and Russian Roulette estimators, are consistent but often require a large number of samples to achieve accurate results. We propose a novel estimator, \emph{BayesSum}, which is an extension of Bayesian quadrature to discrete domains. It is more sample efficient than alternatives due to its ability to make use of prior information about the integrand through a Gaussian process. We show this through theory, deriving a convergence rate significantly faster than Monte Carlo in a broad range of settings. We also demonstrate empirically that our proposed method does indeed require fewer samples on several synthetic settings as well as for parameter estimation for Conway-Maxwell-Poisson and Potts models.

Multi-Output Robust and Conjugate Gaussian Processes

Oct 30, 2025Multi-output Gaussian process (MOGP) regression allows modelling dependencies among multiple correlated response variables. Similarly to standard Gaussian processes, MOGPs are sensitive to model misspecification and outliers, which can distort predictions within individual outputs. This situation can be further exacerbated by multiple anomalous response variables whose errors propagate due to correlations between outputs. To handle this situation, we extend and generalise the robust and conjugate Gaussian process (RCGP) framework introduced by Altamirano et al. (2024). This results in the multi-output RCGP (MO-RCGP): a provably robust MOGP that is conjugate, and jointly captures correlations across outputs. We thoroughly evaluate our approach through applications in finance and cancer research.

Multilevel neural simulation-based inference

Jun 06, 2025

Neural simulation-based inference (SBI) is a popular set of methods for Bayesian inference when models are only available in the form of a simulator. These methods are widely used in the sciences and engineering, where writing down a likelihood can be significantly more challenging than constructing a simulator. However, the performance of neural SBI can suffer when simulators are computationally expensive, thereby limiting the number of simulations that can be performed. In this paper, we propose a novel approach to neural SBI which leverages multilevel Monte Carlo techniques for settings where several simulators of varying cost and fidelity are available. We demonstrate through both theoretical analysis and extensive experiments that our method can significantly enhance the accuracy of SBI methods given a fixed computational budget.

Stationary MMD Points for Cubature

May 27, 2025Approximation of a target probability distribution using a finite set of points is a problem of fundamental importance, arising in cubature, data compression, and optimisation. Several authors have proposed to select points by minimising a maximum mean discrepancy (MMD), but the non-convexity of this objective precludes global minimisation in general. Instead, we consider \emph{stationary} points of the MMD which, in contrast to points globally minimising the MMD, can be accurately computed. Our main theoretical contribution is the (perhaps surprising) result that, for integrands in the associated reproducing kernel Hilbert space, the cubature error of stationary MMD points vanishes \emph{faster} than the MMD. Motivated by this \emph{super-convergence} property, we consider discretised gradient flows as a practical strategy for computing stationary points of the MMD, presenting a refined convergence analysis that establishes a novel non-asymptotic finite-particle error bound, which may be of independent interest.

Kernel Quantile Embeddings and Associated Probability Metrics

May 26, 2025

Embedding probability distributions into reproducing kernel Hilbert spaces (RKHS) has enabled powerful nonparametric methods such as the maximum mean discrepancy (MMD), a statistical distance with strong theoretical and computational properties. At its core, the MMD relies on kernel mean embeddings to represent distributions as mean functions in RKHS. However, it remains unclear if the mean function is the only meaningful RKHS representation. Inspired by generalised quantiles, we introduce the notion of kernel quantile embeddings (KQEs). We then use KQEs to construct a family of distances that: (i) are probability metrics under weaker kernel conditions than MMD; (ii) recover a kernelised form of the sliced Wasserstein distance; and (iii) can be efficiently estimated with near-linear cost. Through hypothesis testing, we show that these distances offer a competitive alternative to MMD and its fast approximations.

A Dictionary of Closed-Form Kernel Mean Embeddings

Apr 26, 2025

Kernel mean embeddings -- integrals of a kernel with respect to a probability distribution -- are essential in Bayesian quadrature, but also widely used in other computational tools for numerical integration or for statistical inference based on the maximum mean discrepancy. These methods often require, or are enhanced by, the availability of a closed-form expression for the kernel mean embedding. However, deriving such expressions can be challenging, limiting the applicability of kernel-based techniques when practitioners do not have access to a closed-form embedding. This paper addresses this limitation by providing a comprehensive dictionary of known kernel mean embeddings, along with practical tools for deriving new embeddings from known ones. We also provide a Python library that includes minimal implementations of the embeddings.

Nested Expectations with Kernel Quadrature

Feb 25, 2025

This paper considers the challenging computational task of estimating nested expectations. Existing algorithms, such as nested Monte Carlo or multilevel Monte Carlo, are known to be consistent but require a large number of samples at both inner and outer levels to converge. Instead, we propose a novel estimator consisting of nested kernel quadrature estimators and we prove that it has a faster convergence rate than all baseline methods when the integrands have sufficient smoothness. We then demonstrate empirically that our proposed method does indeed require fewer samples to estimate nested expectations on real-world applications including Bayesian optimisation, option pricing, and health economics.

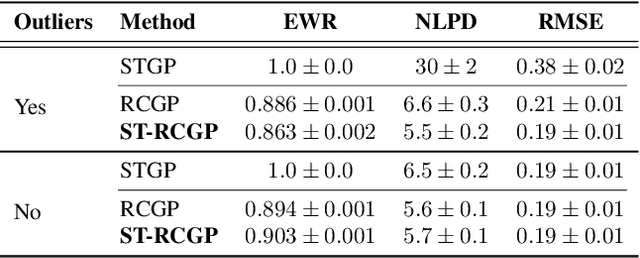

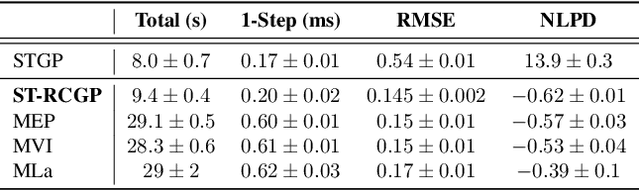

Robust and Conjugate Spatio-Temporal Gaussian Processes

Feb 04, 2025

State-space formulations allow for Gaussian process (GP) regression with linear-in-time computational cost in spatio-temporal settings, but performance typically suffers in the presence of outliers. In this paper, we adapt and specialise the robust and conjugate GP (RCGP) framework of Altamirano et al. (2024) to the spatio-temporal setting. In doing so, we obtain an outlier-robust spatio-temporal GP with a computational cost comparable to classical spatio-temporal GPs. We also overcome the three main drawbacks of RCGPs: their unreliable performance when the prior mean is chosen poorly, their lack of reliable uncertainty quantification, and the need to carefully select a hyperparameter by hand. We study our method extensively in finance and weather forecasting applications, demonstrating that it provides a reliable approach to spatio-temporal modelling in the presence of outliers.

Cost-aware Simulation-based Inference

Oct 10, 2024

Simulation-based inference (SBI) is the preferred framework for estimating parameters of intractable models in science and engineering. A significant challenge in this context is the large computational cost of simulating data from complex models, and the fact that this cost often depends on parameter values. We therefore propose \textit{cost-aware SBI methods} which can significantly reduce the cost of existing sampling-based SBI methods, such as neural SBI and approximate Bayesian computation. This is achieved through a combination of rejection and self-normalised importance sampling, which significantly reduces the number of expensive simulations needed. Our approach is studied extensively on models from epidemiology to telecommunications engineering, where we obtain significant reductions in the overall cost of inference.