Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeRLHF Fine-Tuning of LLMs for Alignment with Implicit User Feedback in Conversational Recommenders

Aug 07, 2025Conversational recommender systems (CRS) based on Large Language Models (LLMs) need to constantly be aligned to the user preferences to provide satisfying and context-relevant item recommendations. The traditional supervised fine-tuning cannot capture the implicit feedback signal, e.g., dwell time, sentiment polarity, or engagement patterns. In this paper, we share a fine-tuning solution using human feedback reinforcement learning (RLHF) to maximize implied user feedback (IUF) in a multi-turn recommendation context. We specify a reward model $R_{\phi}$ learnt on weakly-labelled engagement information and maximize user-centric utility by optimizing the foundational LLM M_{\theta} through a proximal policy optimization (PPO) approach. The architecture models conversational state transitions $s_t \to a_t \to s_{t +1}$, where the action $a_t$ is associated with LLM-generated item suggestions only on condition of conversation history in the past. The evaluation across synthetic and real-world datasets (e.g.REDIAL, OpenDialKG) demonstrates that our RLHF-fine-tuned models can perform better in terms of top-$k$ recommendation accuracy, coherence, and user satisfaction compared to (arrow-zero-cmwrquca-teja-falset ensuite 2Round group-deca States penalty give up This paper shows that implicit signal alignment can be efficient in achieving scalable and user-adaptive design of CRS.

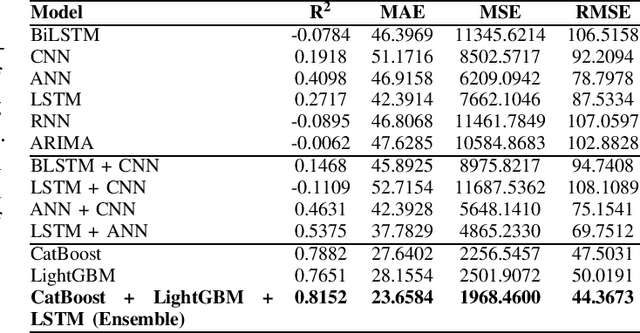

Gradient Boosting Decision Tree with LSTM for Investment Prediction

May 29, 2025

This paper proposes a hybrid framework combining LSTM (Long Short-Term Memory) networks with LightGBM and CatBoost for stock price prediction. The framework processes time-series financial data and evaluates performance using seven models: Artificial Neural Networks (ANNs), Convolutional Neural Networks (CNNs), Bidirectional LSTM (BiLSTM), vanilla LSTM, XGBoost, LightGBM, and standard Neural Networks (NNs). Key metrics, including MAE, R-squared, MSE, and RMSE, are used to establish benchmarks across different time scales. Building on these benchmarks, we develop an ensemble model that combines the strengths of sequential and tree-based approaches. Experimental results show that the proposed framework improves accuracy by 10 to 15 percent compared to individual models and reduces error during market changes. This study highlights the potential of ensemble methods for financial forecasting and provides a flexible design for integrating new machine learning techniques.