Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgePClean: Bayesian Data Cleaning at Scale with Domain-Specific Probabilistic Programming

Aug 07, 2020

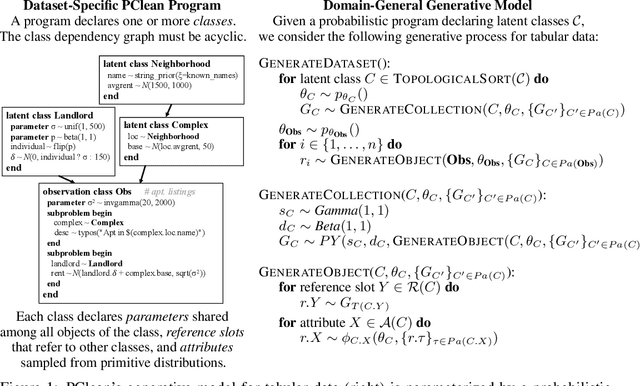

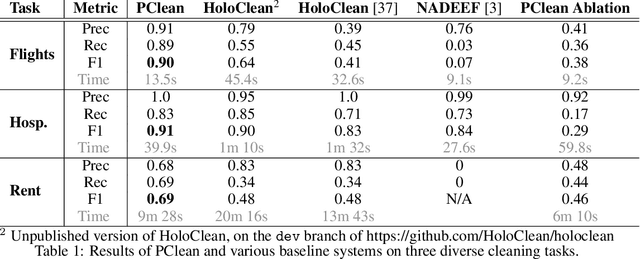

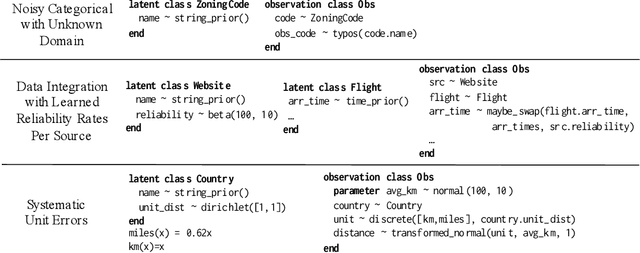

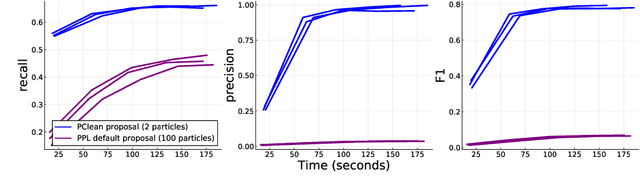

Data cleaning is naturally framed as probabilistic inference in a generative model, combining a prior distribution over ground-truth databases with a likelihood that models the noisy channel by which the data are filtered, corrupted, and joined to yield incomplete, dirty, and denormalized datasets. Based on this view, we present PClean, a unified generative modeling architecture for cleaning and normalizing dirty data in diverse domains. Given an unclean dataset and a probabilistic program encoding relevant domain knowledge, PClean learns a structured representation of the data as a relational database of interrelated objects, and uses this latent structure to impute missing values, identify duplicates, detect errors, and propose corrections in the original data table. PClean makes three modeling and inference contributions: (i) a domain-general non-parametric generative model of relational data, for inferring latent objects and their network of latent connections; (ii) a domain-specific probabilistic programming language, for encoding domain knowledge specific to each dataset being cleaned; and (iii) a domain-general inference engine that adapts to each PClean program by constructing data-driven proposals used in sequential Monte Carlo and particle Gibbs. We show empirically that short (< 50-line) PClean programs deliver higher accuracy than state-of-the-art data cleaning systems based on machine learning and weighted logic; that PClean's inference algorithm is faster than generic particle Gibbs inference for probabilistic programs; and that PClean scales to large real-world datasets with millions of rows.

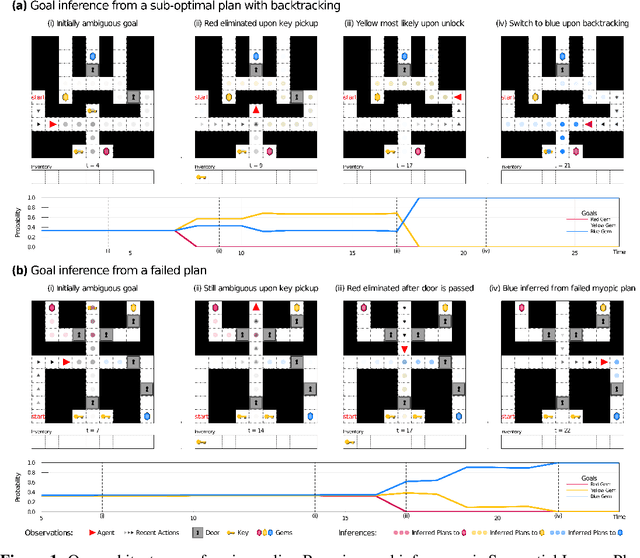

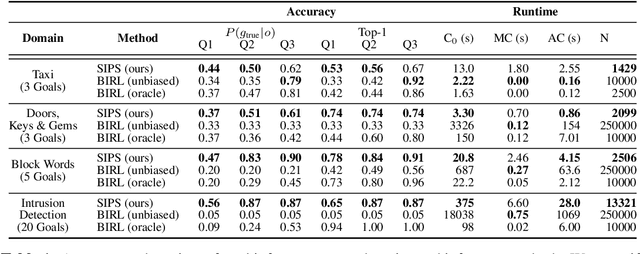

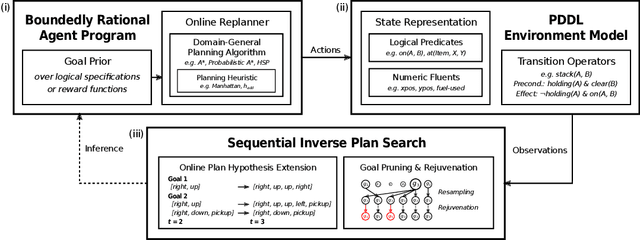

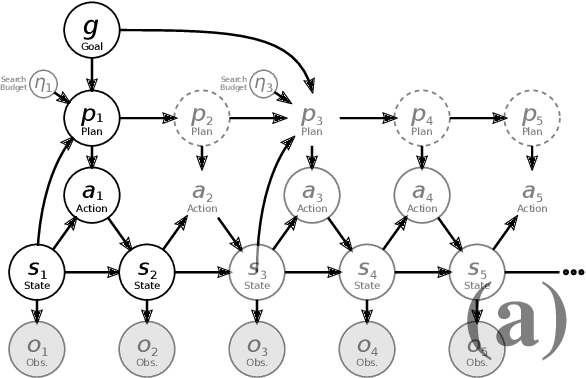

Online Bayesian Goal Inference for Boundedly-Rational Planning Agents

Jun 13, 2020

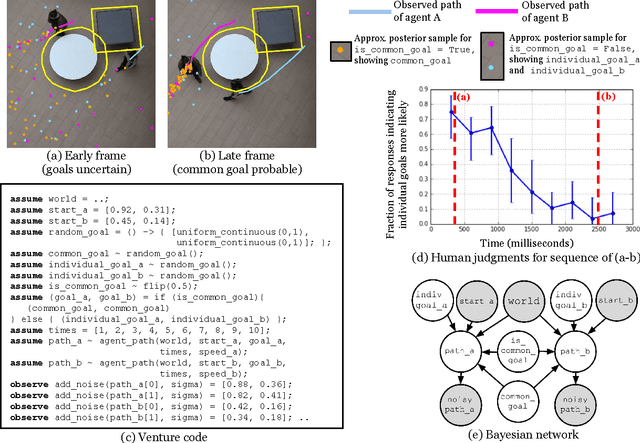

People routinely infer the goals of others by observing their actions over time. Remarkably, we can do so even when those actions lead to failure, enabling us to assist others when we detect that they might not achieve their goals. How might we endow machines with similar capabilities? Here we present an architecture capable of inferring an agent's goals online from both optimal and non-optimal sequences of actions. Our architecture models agents as boundedly-rational planners that interleave search with execution by replanning, thereby accounting for sub-optimal behavior. These models are specified as probabilistic programs, allowing us to represent and perform efficient Bayesian inference over an agent's goals and internal planning processes. To perform such inference, we develop Sequential Inverse Plan Search (SIPS), a sequential Monte Carlo algorithm that exploits the online replanning assumption of these models, limiting computation by incrementally extending inferred plans as new actions are observed. We present experiments showing that this modeling and inference architecture outperforms Bayesian inverse reinforcement learning baselines, accurately inferring goals from both optimal and non-optimal trajectories involving failure and back-tracking, while generalizing across domains with compositional structure and sparse rewards.

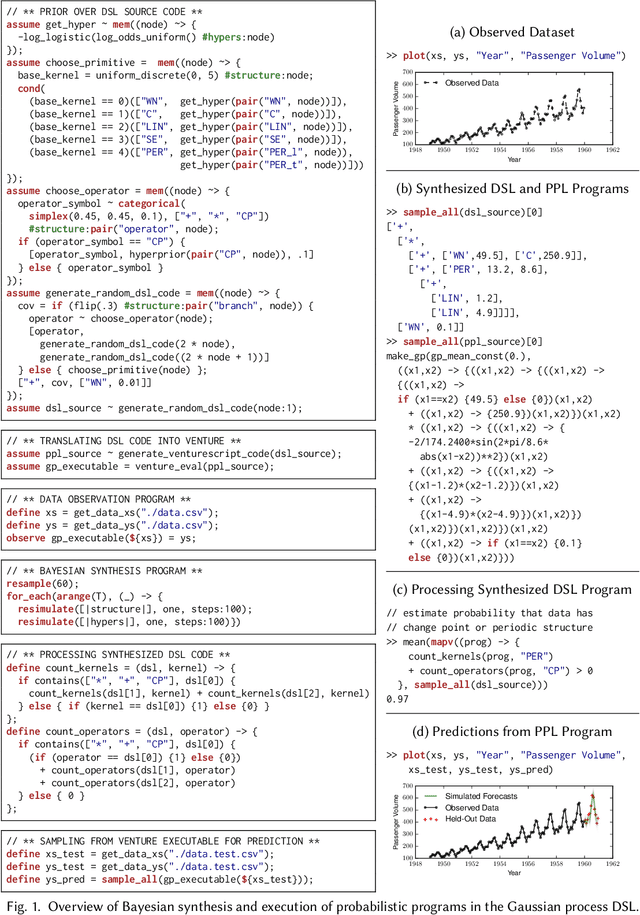

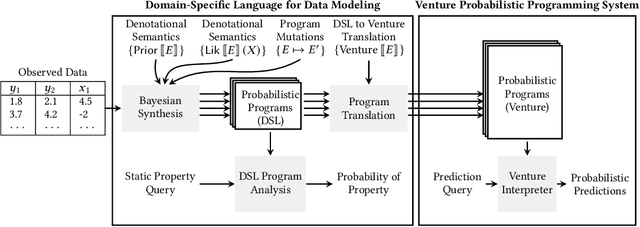

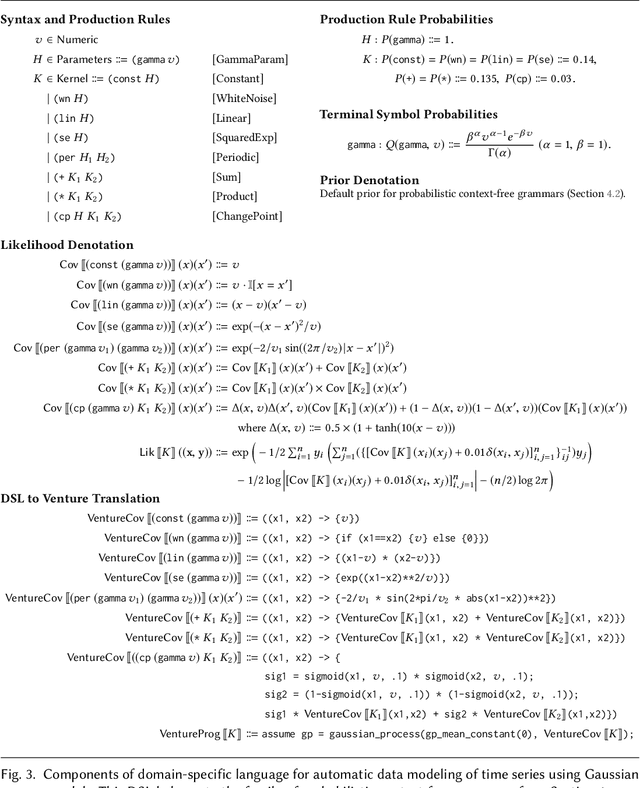

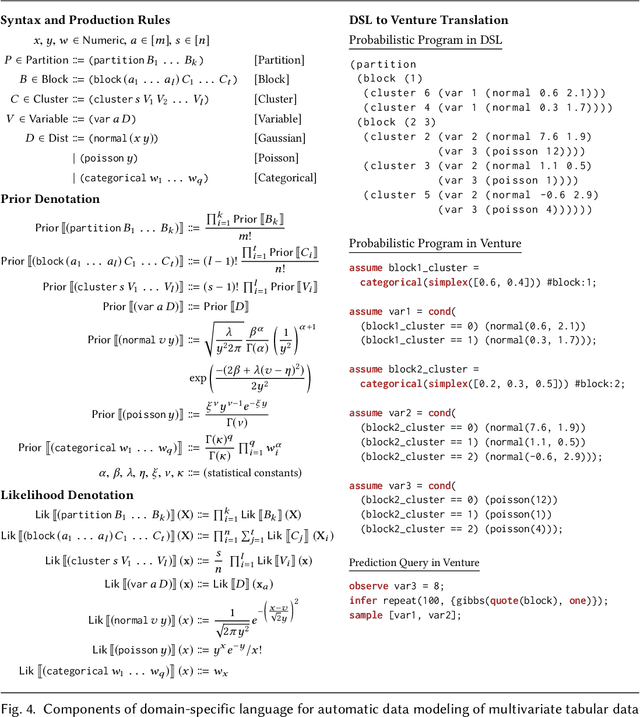

Bayesian Synthesis of Probabilistic Programs for Automatic Data Modeling

Jul 14, 2019

We present new techniques for automatically constructing probabilistic programs for data analysis, interpretation, and prediction. These techniques work with probabilistic domain-specific data modeling languages that capture key properties of a broad class of data generating processes, using Bayesian inference to synthesize probabilistic programs in these modeling languages given observed data. We provide a precise formulation of Bayesian synthesis for automatic data modeling that identifies sufficient conditions for the resulting synthesis procedure to be sound. We also derive a general class of synthesis algorithms for domain-specific languages specified by probabilistic context-free grammars and establish the soundness of our approach for these languages. We apply the techniques to automatically synthesize probabilistic programs for time series data and multivariate tabular data. We show how to analyze the structure of the synthesized programs to compute, for key qualitative properties of interest, the probability that the underlying data generating process exhibits each of these properties. Second, we translate probabilistic programs in the domain-specific language into probabilistic programs in Venture, a general-purpose probabilistic programming system. The translated Venture programs are then executed to obtain predictions of new time series data and new multivariate data records. Experimental results show that our techniques can accurately infer qualitative structure in multiple real-world data sets and outperform standard data analysis methods in forecasting and predicting new data.

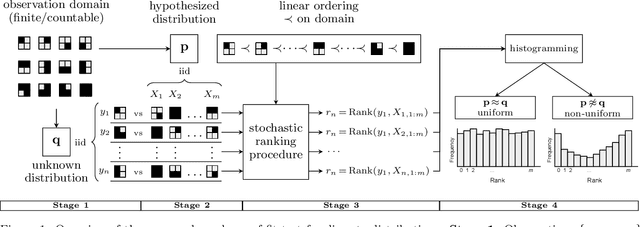

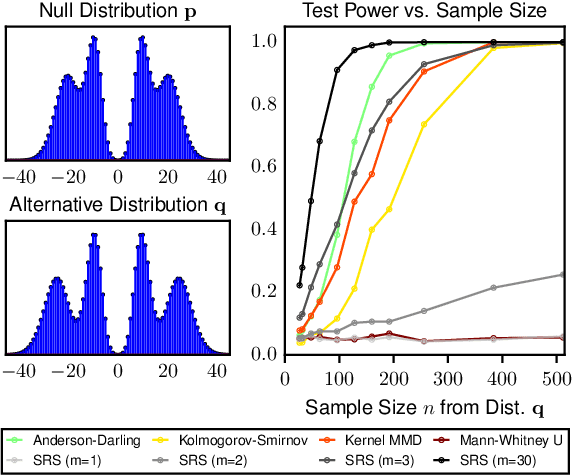

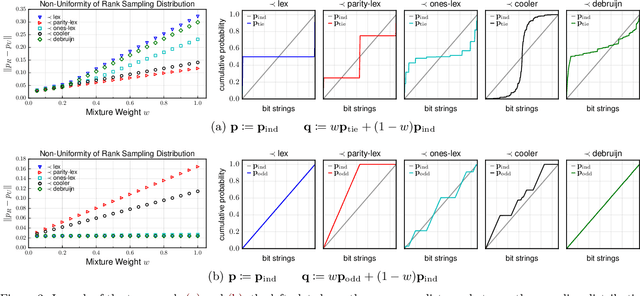

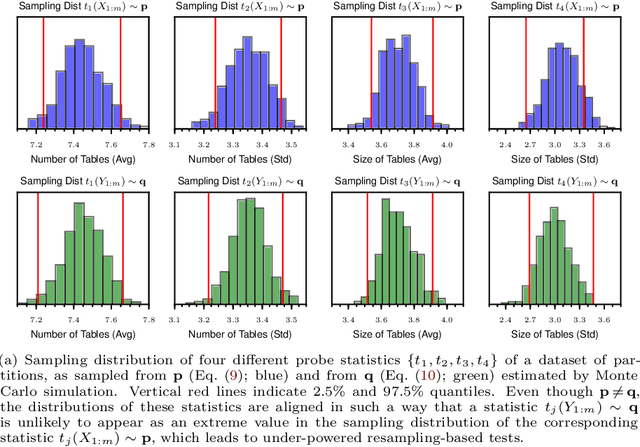

A Family of Exact Goodness-of-Fit Tests for High-Dimensional Discrete Distributions

Feb 26, 2019

The objective of goodness-of-fit testing is to assess whether a dataset of observations is likely to have been drawn from a candidate probability distribution. This paper presents a rank-based family of goodness-of-fit tests that is specialized to discrete distributions on high-dimensional domains. The test is readily implemented using a simulation-based, linear-time procedure. The testing procedure can be customized by the practitioner using knowledge of the underlying data domain. Unlike most existing test statistics, the proposed test statistic is distribution-free and its exact (non-asymptotic) sampling distribution is known in closed form. We establish consistency of the test against all alternatives by showing that the test statistic is distributed as a discrete uniform if and only if the samples were drawn from the candidate distribution. We illustrate its efficacy for assessing the sample quality of approximate sampling algorithms over combinatorially large spaces with intractable probabilities, including random partitions in Dirichlet process mixture models and random lattices in Ising models.

* 20 pages, 6 figures. Appearing in AISTATS 2019

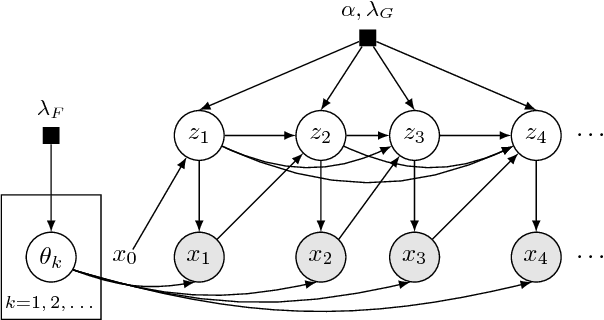

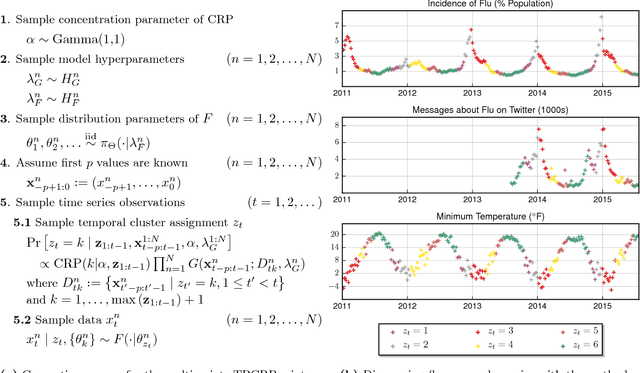

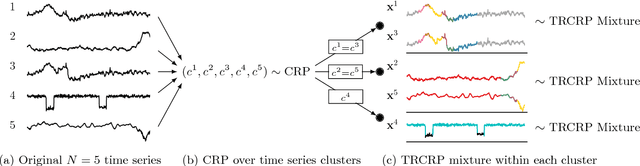

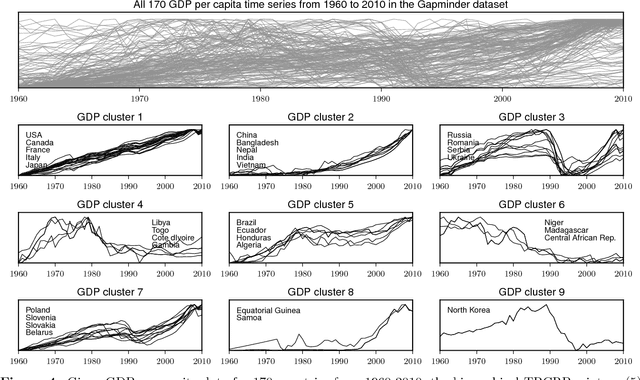

Temporally-Reweighted Chinese Restaurant Process Mixtures for Clustering, Imputing, and Forecasting Multivariate Time Series

Apr 01, 2018

This article proposes a Bayesian nonparametric method for forecasting, imputation, and clustering in sparsely observed, multivariate time series data. The method is appropriate for jointly modeling hundreds of time series with widely varying, non-stationary dynamics. Given a collection of $N$ time series, the Bayesian model first partitions them into independent clusters using a Chinese restaurant process prior. Within a cluster, all time series are modeled jointly using a novel "temporally-reweighted" extension of the Chinese restaurant process mixture. Markov chain Monte Carlo techniques are used to obtain samples from the posterior distribution, which are then used to form predictive inferences. We apply the technique to challenging forecasting and imputation tasks using seasonal flu data from the US Center for Disease Control and Prevention, demonstrating superior forecasting accuracy and competitive imputation accuracy as compared to multiple widely used baselines. We further show that the model discovers interpretable clusters in datasets with hundreds of time series, using macroeconomic data from the Gapminder Foundation.

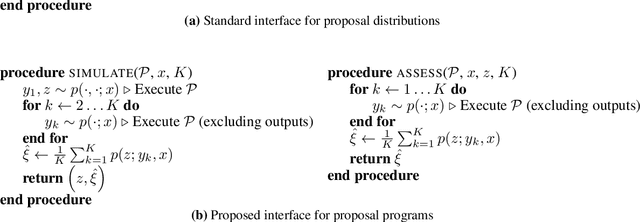

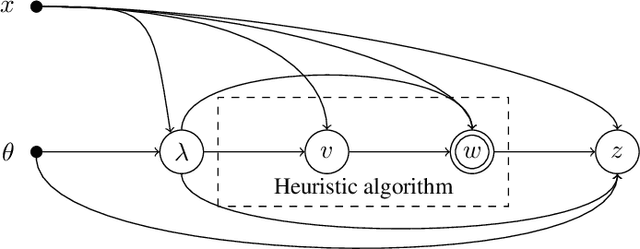

Using probabilistic programs as proposals

Jan 13, 2018

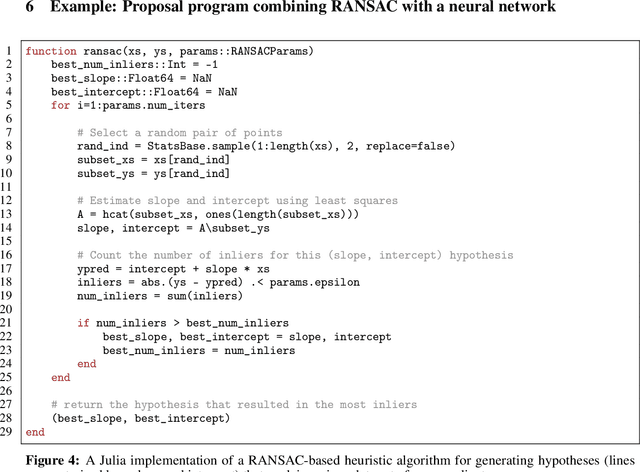

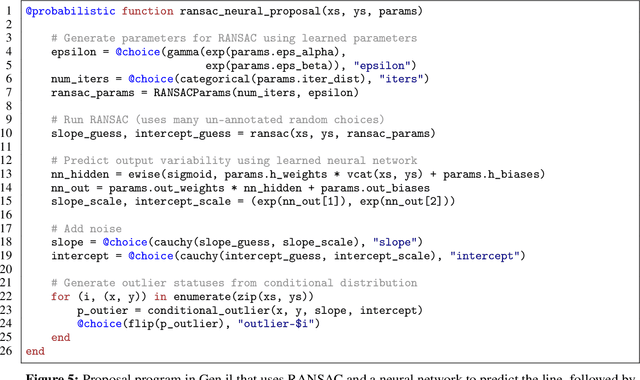

Monte Carlo inference has asymptotic guarantees, but can be slow when using generic proposals. Handcrafted proposals that rely on user knowledge about the posterior distribution can be efficient, but are difficult to derive and implement. This paper proposes to let users express their posterior knowledge in the form of proposal programs, which are samplers written in probabilistic programming languages. One strategy for writing good proposal programs is to combine domain-specific heuristic algorithms with neural network models. The heuristics identify high probability regions, and the neural networks model the posterior uncertainty around the outputs of the algorithm. Proposal programs can be used as proposal distributions in importance sampling and Metropolis-Hastings samplers without sacrificing asymptotic consistency, and can be optimized offline using inference compilation. Support for optimizing and using proposal programs is easily implemented in a sampling-based probabilistic programming runtime. The paper illustrates the proposed technique with a proposal program that combines RANSAC and neural networks to accelerate inference in a Bayesian linear regression with outliers model.

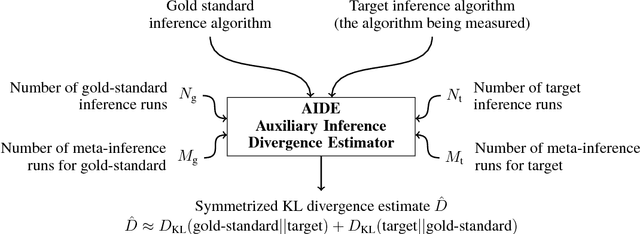

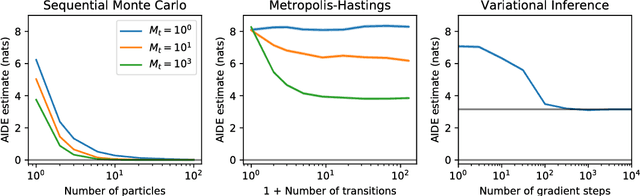

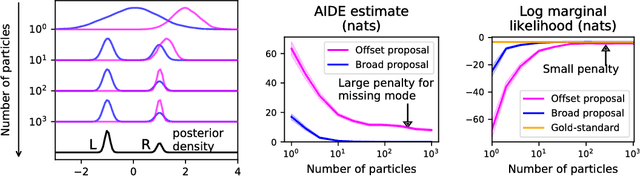

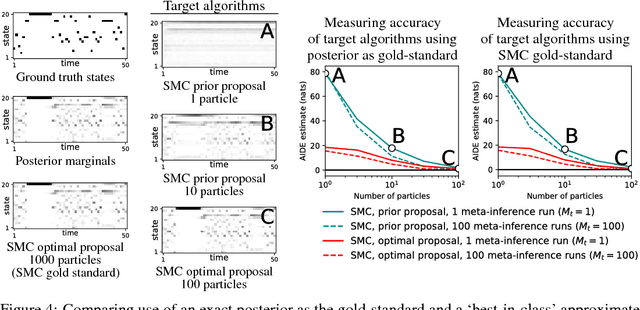

AIDE: An algorithm for measuring the accuracy of probabilistic inference algorithms

Nov 04, 2017

Approximate probabilistic inference algorithms are central to many fields. Examples include sequential Monte Carlo inference in robotics, variational inference in machine learning, and Markov chain Monte Carlo inference in statistics. A key problem faced by practitioners is measuring the accuracy of an approximate inference algorithm on a specific data set. This paper introduces the auxiliary inference divergence estimator (AIDE), an algorithm for measuring the accuracy of approximate inference algorithms. AIDE is based on the observation that inference algorithms can be treated as probabilistic models and the random variables used within the inference algorithm can be viewed as auxiliary variables. This view leads to a new estimator for the symmetric KL divergence between the approximating distributions of two inference algorithms. The paper illustrates application of AIDE to algorithms for inference in regression, hidden Markov, and Dirichlet process mixture models. The experiments show that AIDE captures the qualitative behavior of a broad class of inference algorithms and can detect failure modes of inference algorithms that are missed by standard heuristics.

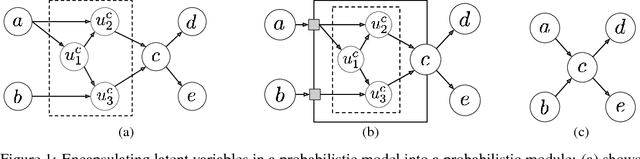

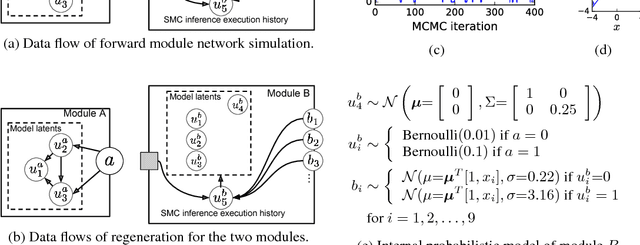

Encapsulating models and approximate inference programs in probabilistic modules

May 06, 2017

This paper introduces the probabilistic module interface, which allows encapsulation of complex probabilistic models with latent variables alongside custom stochastic approximate inference machinery, and provides a platform-agnostic abstraction barrier separating the model internals from the host probabilistic inference system. The interface can be seen as a stochastic generalization of a standard simulation and density interface for probabilistic primitives. We show that sound approximate inference algorithms can be constructed for networks of probabilistic modules, and we demonstrate that the interface can be implemented using learned stochastic inference networks and MCMC and SMC approximate inference programs.

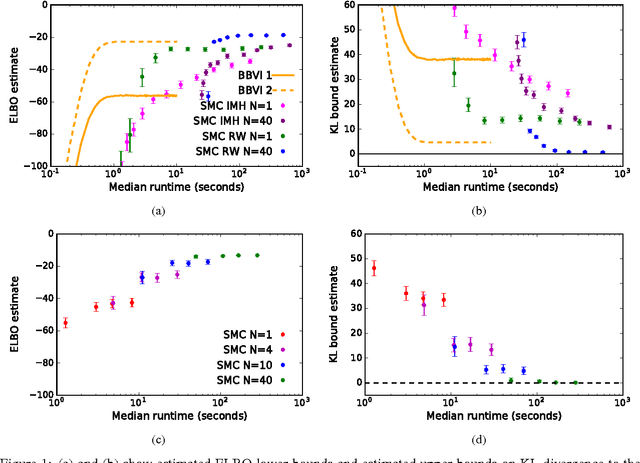

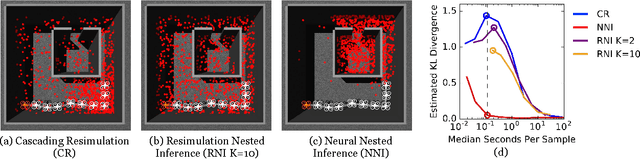

Measuring the non-asymptotic convergence of sequential Monte Carlo samplers using probabilistic programming

May 06, 2017

A key limitation of sampling algorithms for approximate inference is that it is difficult to quantify their approximation error. Widely used sampling schemes, such as sequential importance sampling with resampling and Metropolis-Hastings, produce output samples drawn from a distribution that may be far from the target posterior distribution. This paper shows how to upper-bound the symmetric KL divergence between the output distribution of a broad class of sequential Monte Carlo (SMC) samplers and their target posterior distributions, subject to assumptions about the accuracy of a separate gold-standard sampler. The proposed method applies to samplers that combine multiple particles, multinomial resampling, and rejuvenation kernels. The experiments show the technique being used to estimate bounds on the divergence of SMC samplers for posterior inference in a Bayesian linear regression model and a Dirichlet process mixture model.

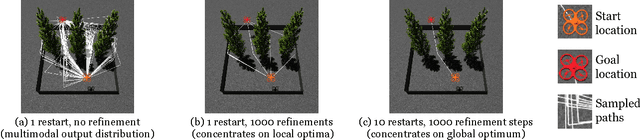

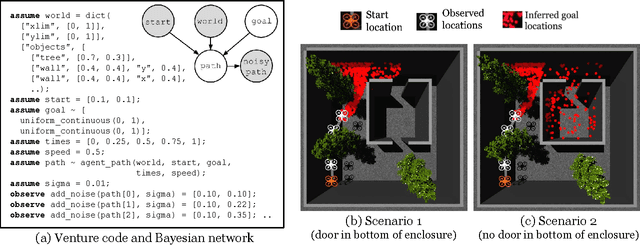

Probabilistic programs for inferring the goals of autonomous agents

Apr 18, 2017

Intelligent systems sometimes need to infer the probable goals of people, cars, and robots, based on partial observations of their motion. This paper introduces a class of probabilistic programs for formulating and solving these problems. The formulation uses randomized path planning algorithms as the basis for probabilistic models of the process by which autonomous agents plan to achieve their goals. Because these path planning algorithms do not have tractable likelihood functions, new inference algorithms are needed. This paper proposes two Monte Carlo techniques for these "likelihood-free" models, one of which can use likelihood estimates from neural networks to accelerate inference. The paper demonstrates efficacy on three simple examples, each using under 50 lines of probabilistic code.