Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeHawkesRank: Event-Driven Centrality for Real-Time Importance Ranking

Mar 12, 2026Quantifying influence in networks is important across science, economics, and public health, yet widely used centrality measures remain limited: they rely on static representations, heuristic network constructions, and purely endogenous notions of importance, while offering little semantic connection to observable activity. We introduce HawkesRank, a dynamic framework grounded in multivariate Hawkes point processes that models exogenous drivers (intrinsic contributions) and endogenous amplification (self- and cross-excitation). This yields a principled, empirically calibrated, and adaptive importance measure. Classical indices such as Katz centrality and PageRank emerge as mean-field limits of the framework, clarifying both their validity and their limitations. Unlike static averages, HawkesRank measures importance through instantaneous event intensities, enabling prediction, transparent endo-exo decomposition, and adaptability to shocks. Using both simulations and empirical analysis of emotion dynamics in online communication platforms, we show that HawkesRank closely tracks system activity and consistently outperforms static centrality metrics.

Why AI Alignment Failure Is Structural: Learned Human Interaction Structures and AGI as an Endogenous Evolutionary Shock

Jan 13, 2026Recent reports of large language models (LLMs) exhibiting behaviors such as deception, threats, or blackmail are often interpreted as evidence of alignment failure or emergent malign agency. We argue that this interpretation rests on a conceptual error. LLMs do not reason morally; they statistically internalize the record of human social interaction, including laws, contracts, negotiations, conflicts, and coercive arrangements. Behaviors commonly labeled as unethical or anomalous are therefore better understood as structural generalizations of interaction regimes that arise under extreme asymmetries of power, information, or constraint. Drawing on relational models theory, we show that practices such as blackmail are not categorical deviations from normal social behavior, but limiting cases within the same continuum that includes market pricing, authority relations, and ultimatum bargaining. The surprise elicited by such outputs reflects an anthropomorphic expectation that intelligence should reproduce only socially sanctioned behavior, rather than the full statistical landscape of behaviors humans themselves enact. Because human morality is plural, context-dependent, and historically contingent, the notion of a universally moral artificial intelligence is ill-defined. We therefore reframe concerns about artificial general intelligence (AGI). The primary risk is not adversarial intent, but AGI's role as an endogenous amplifier of human intelligence, power, and contradiction. By eliminating longstanding cognitive and institutional frictions, AGI compresses timescales and removes the historical margin of error that has allowed inconsistent values and governance regimes to persist without collapse. Alignment failure is thus structural, not accidental, and requires governance approaches that address amplification, complexity, and regime stability rather than model-level intent alone.

Predicting Adverse Media Risk using a Heterogeneous Information Network

Nov 09, 2018

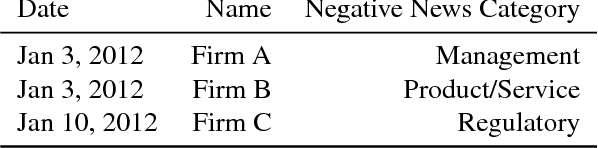

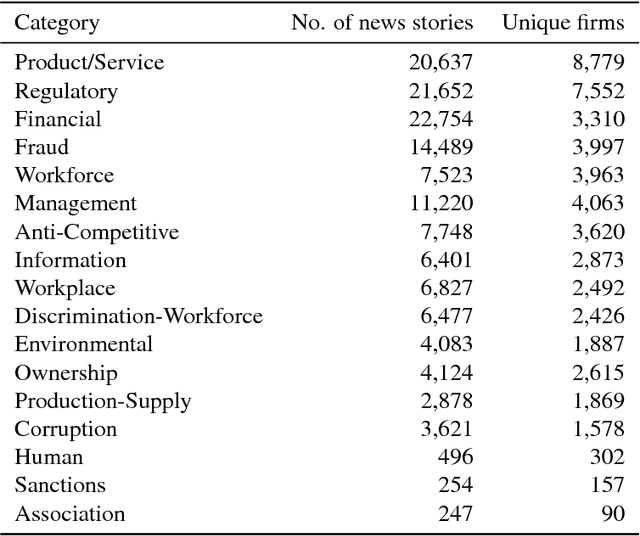

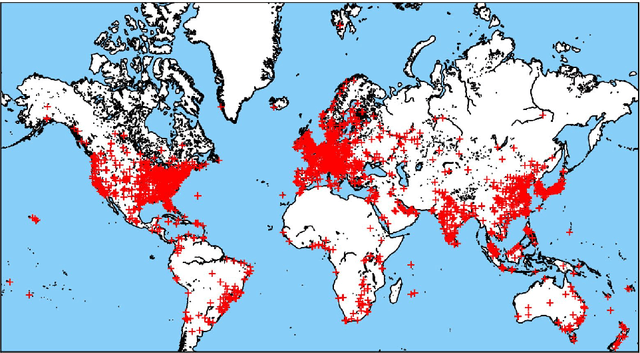

The media plays a central role in monitoring powerful institutions and identifying any activities harmful to the public interest. In the investing sphere constituted of 46,583 officially listed domestic firms on the stock exchanges worldwide, there is a growing interest `to do the right thing', i.e., to put pressure on companies to improve their environmental, social and government (ESG) practices. However, how to overcome the sparsity of ESG data from non-reporting firms, and how to identify the relevant information in the annual reports of this large universe? Here, we construct a vast heterogeneous information network that covers the necessary information surrounding each firm, which is assembled using seven professionally curated datasets and two open datasets, resulting in about 50 million nodes and 400 million edges in total. Exploiting this heterogeneous information network, we propose a model that can learn from past adverse media coverage patterns and predict the occurrence of future adverse media coverage events on the whole universe of firms. Our approach is tested using the adverse media coverage data of more than 35,000 firms worldwide from January 2012 to May 2018. Comparing with state-of-the-art methods with and without the network, we show that the predictive accuracy is substantially improved when using the heterogeneous information network. This work suggests new ways to consolidate the diffuse information contained in big data in order to monitor dominant institutions on a global scale for more socially responsible investment, better risk management, and the surveillance of powerful institutions.

Learning like humans with Deep Symbolic Networks

Jul 13, 2017

We introduce the Deep Symbolic Network (DSN) model, which aims at becoming the white-box version of Deep Neural Networks (DNN). The DSN model provides a simple, universal yet powerful structure, similar to DNN, to represent any knowledge of the world, which is transparent to humans. The conjecture behind the DSN model is that any type of real world objects sharing enough common features are mapped into human brains as a symbol. Those symbols are connected by links, representing the composition, correlation, causality, or other relationships between them, forming a deep, hierarchical symbolic network structure. Powered by such a structure, the DSN model is expected to learn like humans, because of its unique characteristics. First, it is universal, using the same structure to store any knowledge. Second, it can learn symbols from the world and construct the deep symbolic networks automatically, by utilizing the fact that real world objects have been naturally separated by singularities. Third, it is symbolic, with the capacity of performing causal deduction and generalization. Fourth, the symbols and the links between them are transparent to us, and thus we will know what it has learned or not - which is the key for the security of an AI system. Fifth, its transparency enables it to learn with relatively small data. Sixth, its knowledge can be accumulated. Last but not least, it is more friendly to unsupervised learning than DNN. We present the details of the model, the algorithm powering its automatic learning ability, and describe its usefulness in different use cases. The purpose of this paper is to generate broad interest to develop it within an open source project centered on the Deep Symbolic Network (DSN) model towards the development of general AI.

Decision trees unearth return sign correlation in the S&P 500

Apr 14, 2017Technical trading rules and linear regressive models are often used by practitioners to find trends in financial data. However, these models are unsuited to find non-linearly separable patterns. We propose a decision tree forecasting model that has the flexibility to capture arbitrary patterns. To illustrate, we construct a binary Markov process with a deterministic component that cannot be predicted with an autoregressive process. A simulation study confirms the robustness of the trees and limitation of the autoregressive model. Finally, adjusting for multiple testing, we show that some tree based strategies achieve trading performance significant at the 99% confidence level on the S&P 500 over the past 20 years. The best strategy breaks even with the buy-and-hold strategy at 21 bps in transaction costs per round trip. A four-factor regression analysis shows significant intercept and correlation with the market. The return anomalies are strongest during the bursts of the dotcom bubble, financial crisis, and European debt crisis. The correlation of the return signs during these periods confirms the theoretical model.

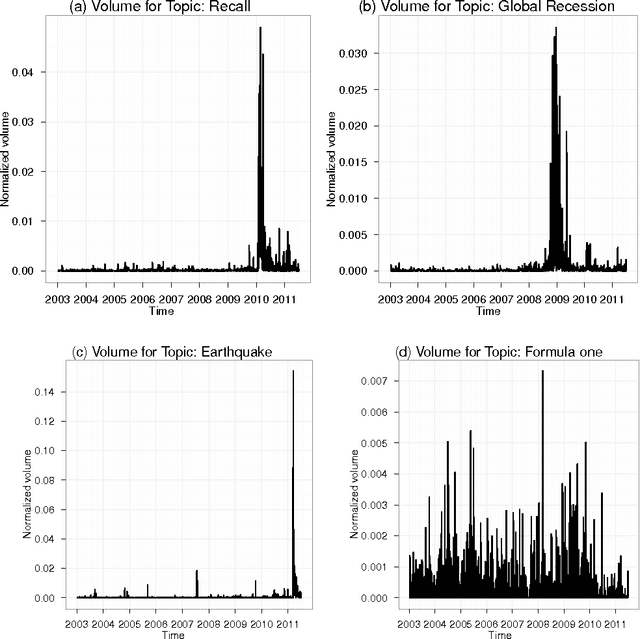

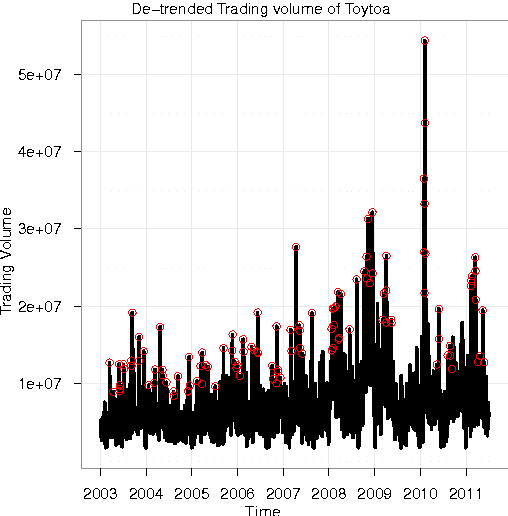

High quality topic extraction from business news explains abnormal financial market volatility

Mar 23, 2013

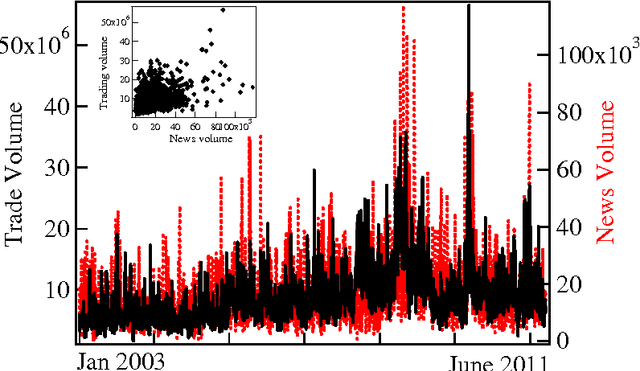

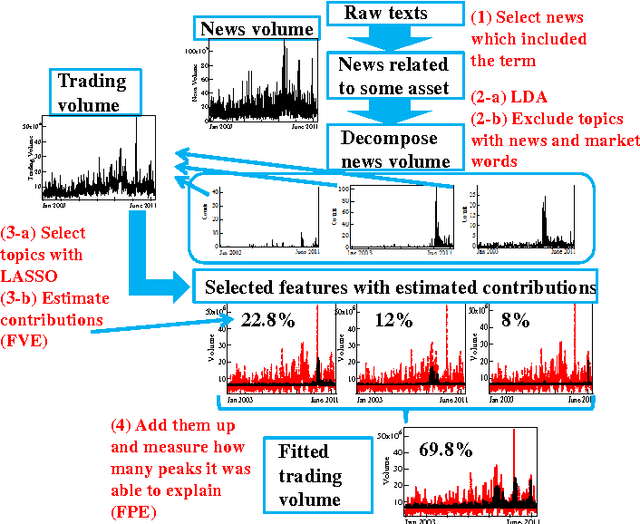

Understanding the mutual relationships between information flows and social activity in society today is one of the cornerstones of the social sciences. In financial economics, the key issue in this regard is understanding and quantifying how news of all possible types (geopolitical, environmental, social, financial, economic, etc.) affect trading and the pricing of firms in organized stock markets. In this article, we seek to address this issue by performing an analysis of more than 24 million news records provided by Thompson Reuters and of their relationship with trading activity for 206 major stocks in the S&P US stock index. We show that the whole landscape of news that affect stock price movements can be automatically summarized via simple regularized regressions between trading activity and news information pieces decomposed, with the help of simple topic modeling techniques, into their "thematic" features. Using these methods, we are able to estimate and quantify the impacts of news on trading. We introduce network-based visualization techniques to represent the whole landscape of news information associated with a basket of stocks. The examination of the words that are representative of the topic distributions confirms that our method is able to extract the significant pieces of information influencing the stock market. Our results show that one of the most puzzling stylized fact in financial economies, namely that at certain times trading volumes appear to be "abnormally large," can be partially explained by the flow of news. In this sense, our results prove that there is no "excess trading," when restricting to times when news are genuinely novel and provide relevant financial information.