Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeStock Movement Prediction Based on Bi-typed Hybrid-relational Market Knowledge Graph via Dual Attention Networks

Paper and Code

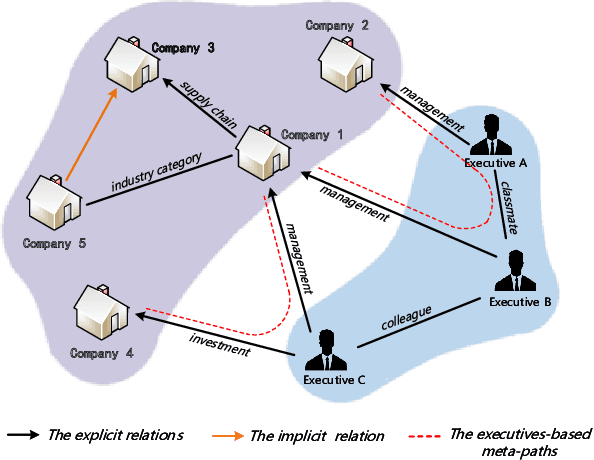

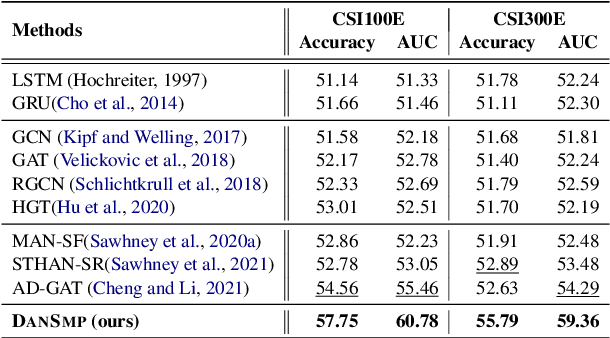

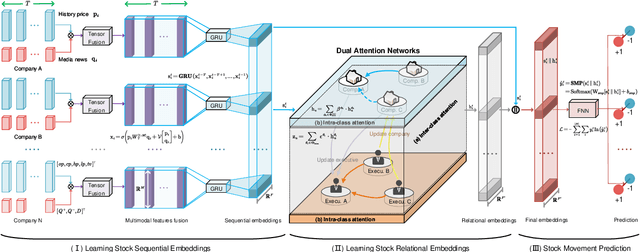

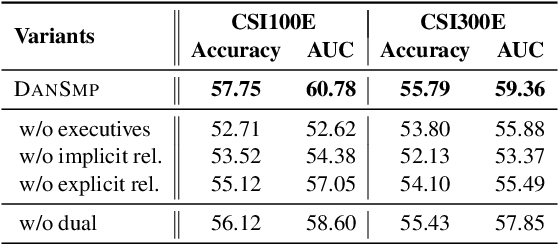

Stock Movement Prediction (SMP) aims at predicting listed companies' stock future price trend, which is a challenging task due to the volatile nature of financial markets. Recent financial studies show that the momentum spillover effect plays a significant role in stock fluctuation. However, previous studies typically only learn the simple connection information among related companies, which inevitably fail to model complex relations of listed companies in the real financial market. To address this issue, we first construct a more comprehensive Market Knowledge Graph (MKG) which contains bi-typed entities including listed companies and their associated executives, and hybrid-relations including the explicit relations and implicit relations. Afterward, we propose DanSmp, a novel Dual Attention Networks to learn the momentum spillover signals based upon the constructed MKG for stock prediction. The empirical experiments on our constructed datasets against nine SOTA baselines demonstrate that the proposed DanSmp is capable of improving stock prediction with the constructed MKG.