Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeNonstochastic Multi-Armed Bandits with Graph-Structured Feedback

Sep 30, 2014

We present and study a partial-information model of online learning, where a decision maker repeatedly chooses from a finite set of actions, and observes some subset of the associated losses. This naturally models several situations where the losses of different actions are related, and knowing the loss of one action provides information on the loss of other actions. Moreover, it generalizes and interpolates between the well studied full-information setting (where all losses are revealed) and the bandit setting (where only the loss of the action chosen by the player is revealed). We provide several algorithms addressing different variants of our setting, and provide tight regret bounds depending on combinatorial properties of the information feedback structure.

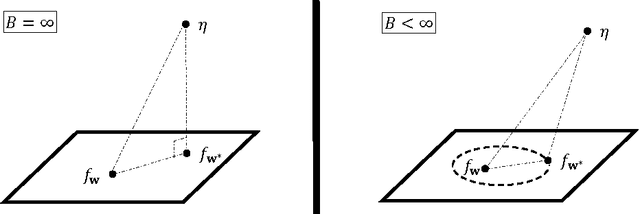

On the Complexity of Bandit Linear Optimization

Aug 11, 2014We study the attainable regret for online linear optimization problems with bandit feedback, where unlike the full-information setting, the player can only observe its own loss rather than the full loss vector. We show that the price of bandit information in this setting can be as large as $d$, disproving the well-known conjecture that the regret for bandit linear optimization is at most $\sqrt{d}$ times the full-information regret. Surprisingly, this is shown using "trivial" modifications of standard domains, which have no effect in the full-information setting. This and other results we present highlight some interesting differences between full-information and bandit learning, which were not considered in previous literature.

The Sample Complexity of Learning Linear Predictors with the Squared Loss

Jun 21, 2014

In this short note, we provide tight sample complexity bounds for learning linear predictors with respect to the squared loss. Our focus is on an agnostic setting, where no assumptions are made on the data distribution. This contrasts with standard results in the literature, which either make distributional assumptions, refer to specific parameter settings, or use other performance measures.

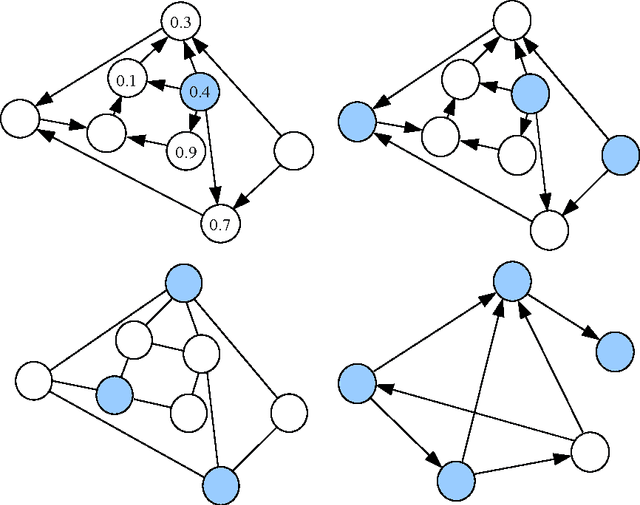

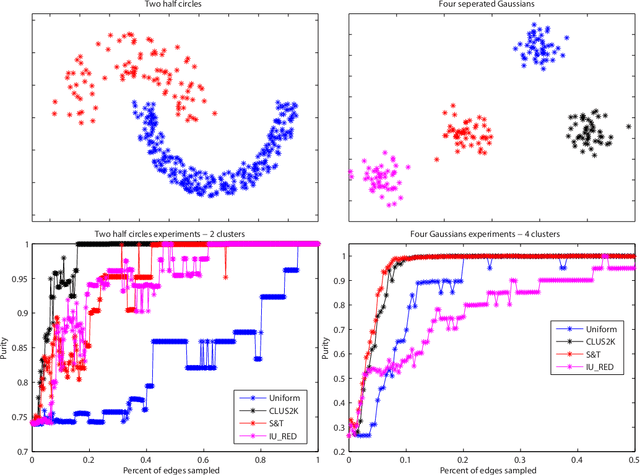

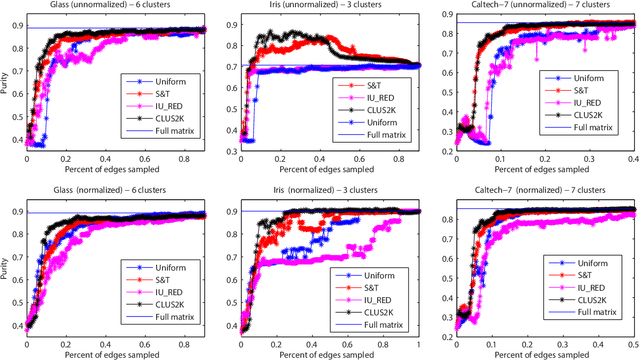

Graph Approximation and Clustering on a Budget

Jun 10, 2014

We consider the problem of learning from a similarity matrix (such as spectral clustering and lowd imensional embedding), when computing pairwise similarities are costly, and only a limited number of entries can be observed. We provide a theoretical analysis using standard notions of graph approximation, significantly generalizing previous results (which focused on spectral clustering with two clusters). We also propose a new algorithmic approach based on adaptive sampling, which experimentally matches or improves on previous methods, while being considerably more general and computationally cheaper.

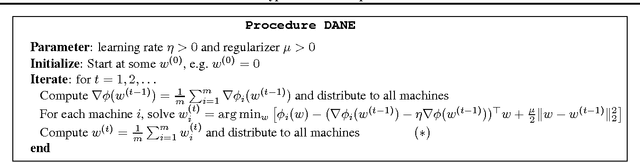

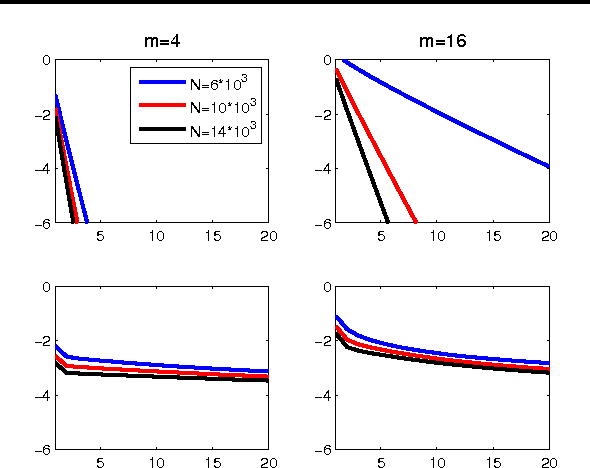

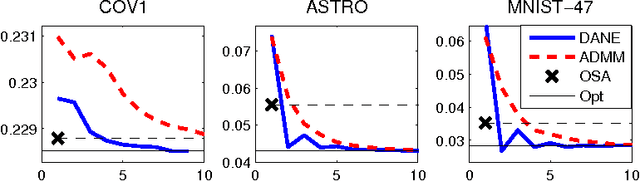

Communication Efficient Distributed Optimization using an Approximate Newton-type Method

May 13, 2014

We present a novel Newton-type method for distributed optimization, which is particularly well suited for stochastic optimization and learning problems. For quadratic objectives, the method enjoys a linear rate of convergence which provably \emph{improves} with the data size, requiring an essentially constant number of iterations under reasonable assumptions. We provide theoretical and empirical evidence of the advantages of our method compared to other approaches, such as one-shot parameter averaging and ADMM.

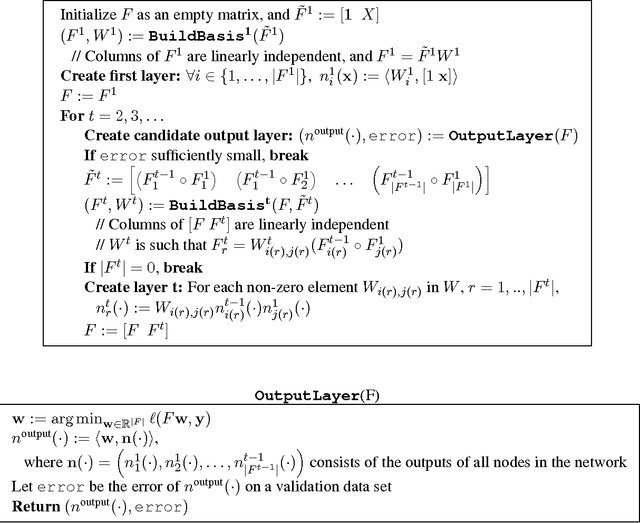

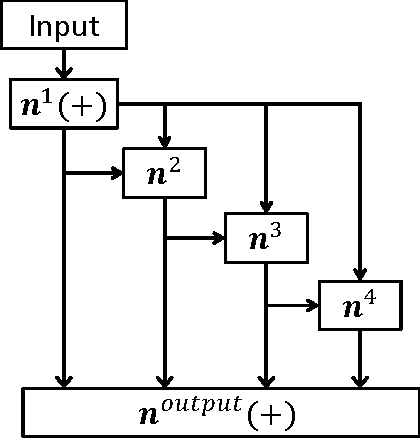

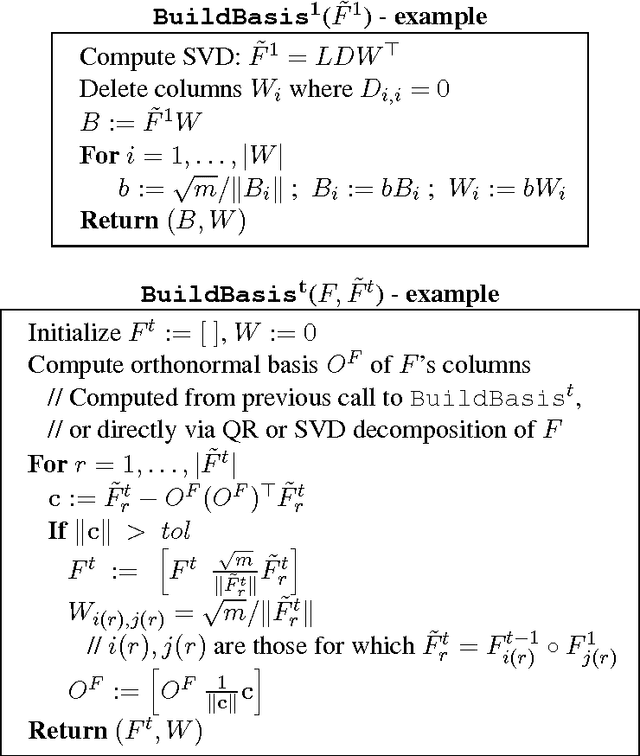

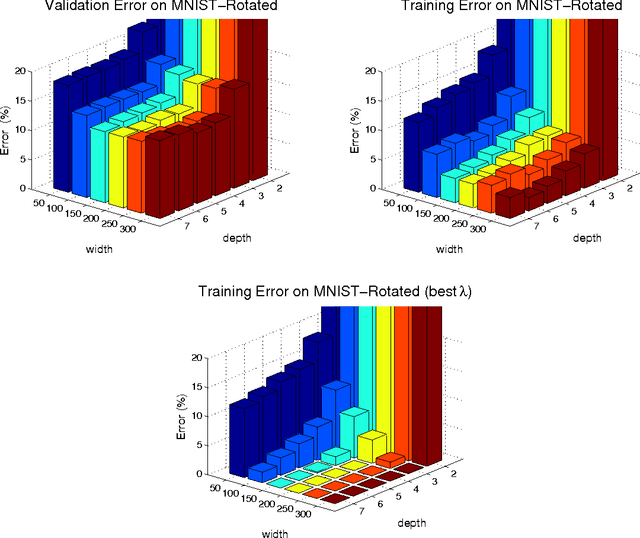

An Algorithm for Training Polynomial Networks

Feb 20, 2014

We consider deep neural networks, in which the output of each node is a quadratic function of its inputs. Similar to other deep architectures, these networks can compactly represent any function on a finite training set. The main goal of this paper is the derivation of an efficient layer-by-layer algorithm for training such networks, which we denote as the \emph{Basis Learner}. The algorithm is a universal learner in the sense that the training error is guaranteed to decrease at every iteration, and can eventually reach zero under mild conditions. We present practical implementations of this algorithm, as well as preliminary experimental results. We also compare our deep architecture to other shallow architectures for learning polynomials, in particular kernel learning.

Efficient Transductive Online Learning via Randomized Rounding

Sep 11, 2013Most traditional online learning algorithms are based on variants of mirror descent or follow-the-leader. In this paper, we present an online algorithm based on a completely different approach, tailored for transductive settings, which combines "random playout" and randomized rounding of loss subgradients. As an application of our approach, we present the first computationally efficient online algorithm for collaborative filtering with trace-norm constrained matrices. As a second application, we solve an open question linking batch learning and transductive online learning

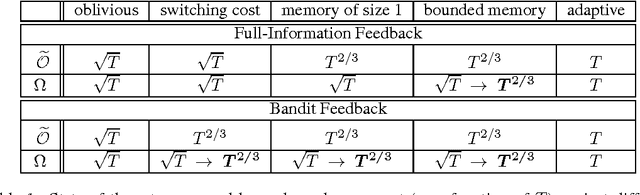

Online Learning with Switching Costs and Other Adaptive Adversaries

Jun 01, 2013

We study the power of different types of adaptive (nonoblivious) adversaries in the setting of prediction with expert advice, under both full-information and bandit feedback. We measure the player's performance using a new notion of regret, also known as policy regret, which better captures the adversary's adaptiveness to the player's behavior. In a setting where losses are allowed to drift, we characterize ---in a nearly complete manner--- the power of adaptive adversaries with bounded memories and switching costs. In particular, we show that with switching costs, the attainable rate with bandit feedback is $\widetilde{\Theta}(T^{2/3})$. Interestingly, this rate is significantly worse than the $\Theta(\sqrt{T})$ rate attainable with switching costs in the full-information case. Via a novel reduction from experts to bandits, we also show that a bounded memory adversary can force $\widetilde{\Theta}(T^{2/3})$ regret even in the full information case, proving that switching costs are easier to control than bounded memory adversaries. Our lower bounds rely on a new stochastic adversary strategy that generates loss processes with strong dependencies.

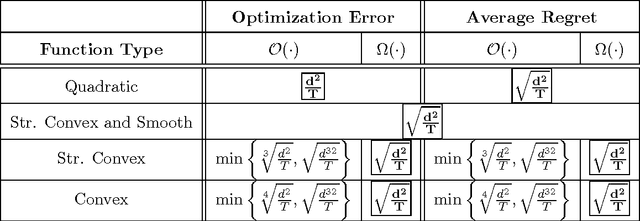

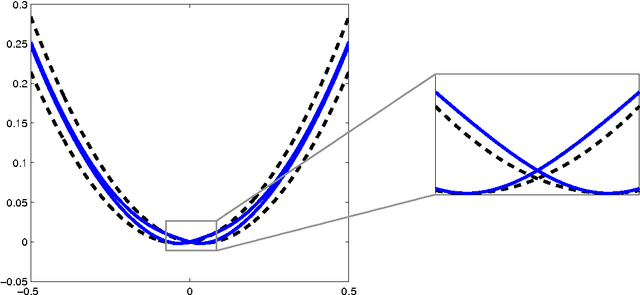

On the Complexity of Bandit and Derivative-Free Stochastic Convex Optimization

Apr 29, 2013

The problem of stochastic convex optimization with bandit feedback (in the learning community) or without knowledge of gradients (in the optimization community) has received much attention in recent years, in the form of algorithms and performance upper bounds. However, much less is known about the inherent complexity of these problems, and there are few lower bounds in the literature, especially for nonlinear functions. In this paper, we investigate the attainable error/regret in the bandit and derivative-free settings, as a function of the dimension d and the available number of queries T. We provide a precise characterization of the attainable performance for strongly-convex and smooth functions, which also imply a non-trivial lower bound for more general problems. Moreover, we prove that in both the bandit and derivative-free setting, the required number of queries must scale at least quadratically with the dimension. Finally, we show that on the natural class of quadratic functions, it is possible to obtain a "fast" O(1/T) error rate in terms of T, under mild assumptions, even without having access to gradients. To the best of our knowledge, this is the first such rate in a derivative-free stochastic setting, and holds despite previous results which seem to imply the contrary.

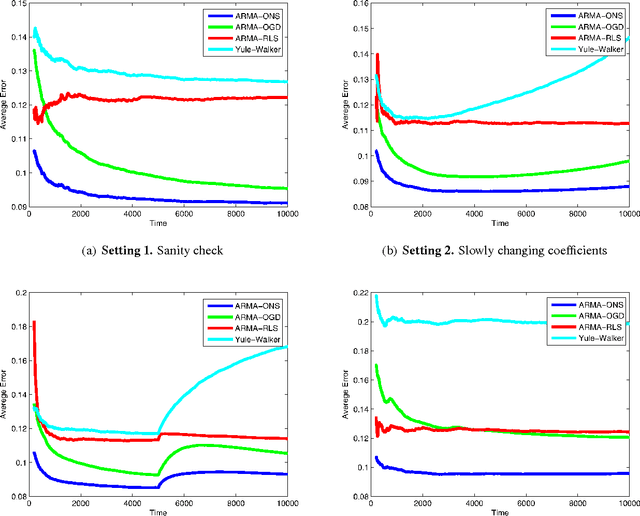

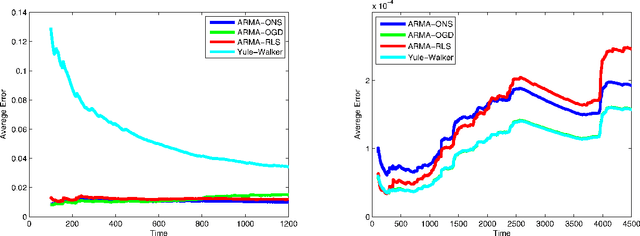

Online Learning for Time Series Prediction

Feb 27, 2013

In this paper we address the problem of predicting a time series using the ARMA (autoregressive moving average) model, under minimal assumptions on the noise terms. Using regret minimization techniques, we develop effective online learning algorithms for the prediction problem, without assuming that the noise terms are Gaussian, identically distributed or even independent. Furthermore, we show that our algorithm's performances asymptotically approaches the performance of the best ARMA model in hindsight.