Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeDo Not Trust The Auctioneer: Learning to Bid in Feedback-Manipulated Auctions

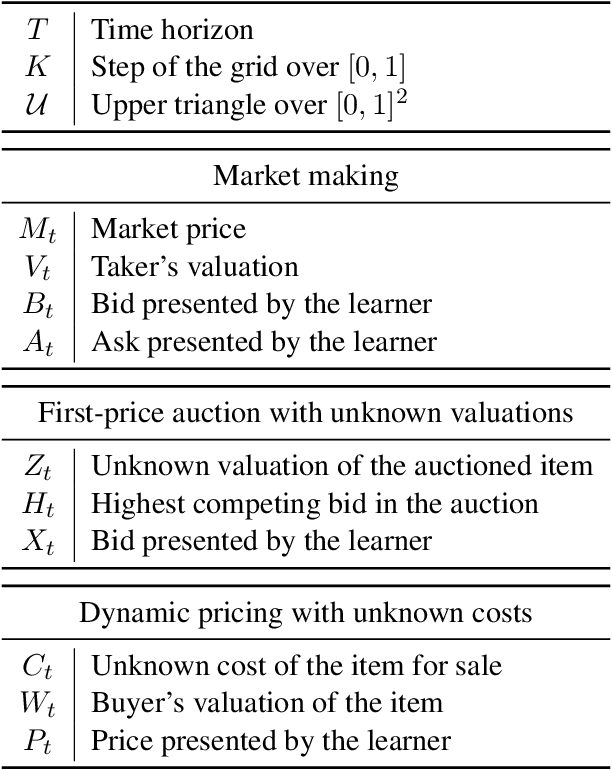

May 21, 2026Shilling is the use of artificial bids to make competition appear stronger and push prices upward. We study repeated first-price auctions in which shilling affects feedback but not allocation: the learner wins or loses against the real competing bid, but after a loss observes the maximum of the real bid and an independent shill bid. Thus the manipulation changes what the learner observes and hence how it learns to bid, without changing the outcome of the current auction. We analyze regret with respect to the best bid benchmark, assuming that the shill-bid distribution is known. Even then, shilling can mask the real bid, while useful side information appears only through intermittent low-shill events. Our algorithm combines a robust interval-elimination branch, which ignores the shilled report and achieves the dynamic-pricing rate $\tilde{\mathcal{O}}(T^{2/3})$, with an optimistic branch that debiases losing-side reports and exploits the resulting suffix information when it is reliable and achieves the first-price auctions rate $\tilde{\mathcal{O}}(\sqrt{T})$. A validation and racing procedure lets the algorithm use these optimistic updates without knowing the right scale or feedback geometry in advance. We complement the upper bounds with a matching lower bound, up to logarithmic factors, in the single-active-region case. Overall, the results show that even feedback-only shilling can sharply alter the statistical difficulty of repeated bidding.

Market Making without Regret

Nov 21, 2024

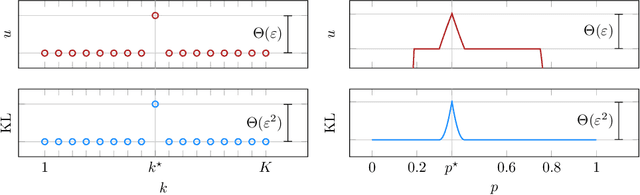

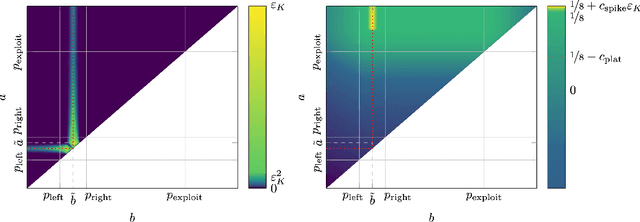

We consider a sequential decision-making setting where, at every round $t$, a market maker posts a bid price $B_t$ and an ask price $A_t$ to an incoming trader (the taker) with a private valuation for one unit of some asset. If the trader's valuation is lower than the bid price, or higher than the ask price, then a trade (sell or buy) occurs. If a trade happens at round $t$, then letting $M_t$ be the market price (observed only at the end of round $t$), the maker's utility is $M_t - B_t$ if the maker bought the asset, and $A_t - M_t$ if they sold it. We characterize the maker's regret with respect to the best fixed choice of bid and ask pairs under a variety of assumptions (adversarial, i.i.d., and their variants) on the sequence of market prices and valuations. Our upper bound analysis unveils an intriguing connection relating market making to first-price auctions and dynamic pricing. Our main technical contribution is a lower bound for the i.i.d. case with Lipschitz distributions and independence between prices and valuations. The difficulty in the analysis stems from the unique structure of the reward and feedback functions, allowing an algorithm to acquire information by graduating the "cost of exploration" in an arbitrary way.