Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeLimited Lookahead in Imperfect-Information Games

Feb 17, 2019

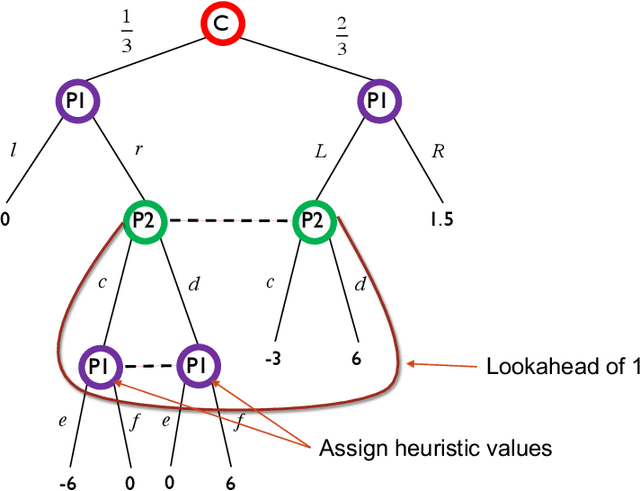

Limited lookahead has been studied for decades in complete-information games. We initiate a new direction via two simultaneous deviation points: generalization to incomplete-information games and a game-theoretic approach. We study how one should act when facing an opponent whose lookahead is limited. We study this for opponents that differ based on their lookahead depth, based on whether they, too, have incomplete information, and based on how they break ties. We characterize the hardness of finding a Nash equilibrium or an optimal commitment strategy for either player, showing that in some of these variations the problem can be solved in polynomial time while in others it is PPAD-hard or NP-hard. We proceed to design algorithms for computing optimal commitment strategies---for when the opponent breaks ties favorably, according to a fixed rule, or adversarially. We then experimentally investigate the impact of limited lookahead. The limited-lookahead player often obtains the value of the game if she knows the expected values of nodes in the game tree for some equilibrium---but we prove this is not sufficient in general. Finally, we study the impact of noise in those estimates and different lookahead depths. This uncovers an incomplete-information game lookahead pathology.

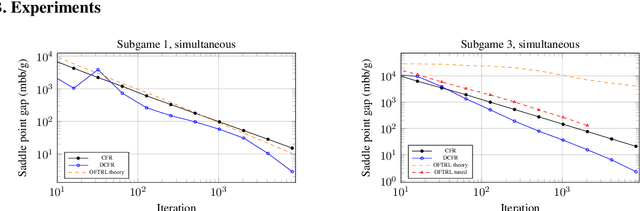

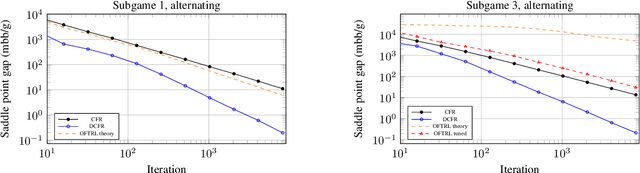

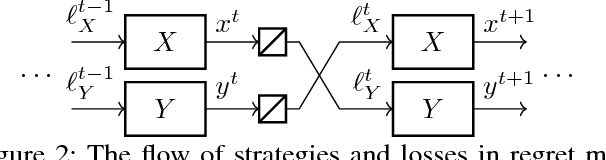

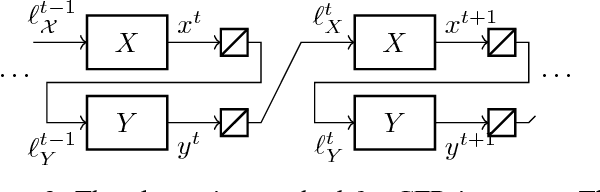

Stable-Predictive Optimistic Counterfactual Regret Minimization

Feb 13, 2019

The CFR framework has been a powerful tool for solving large-scale extensive-form games in practice. However, the theoretical rate at which past CFR-based algorithms converge to the Nash equilibrium is on the order of $O(T^{-1/2})$, where $T$ is the number of iterations. In contrast, first-order methods can be used to achieve a $O(T^{-1})$ dependence on iterations, yet these methods have been less successful in practice. In this work we present the first CFR variant that breaks the square-root dependence on iterations. By combining and extending recent advances on predictive and stable regret minimizers for the matrix-game setting we show that it is possible to leverage "optimistic" regret minimizers to achieve a $O(T^{-3/4})$ convergence rate within CFR. This is achieved by introducing a new notion of stable-predictivity, and by setting the stability of each counterfactual regret minimizer relative to its location in the decision tree. Experiments show that this method is faster than the original CFR algorithm, although not as fast as newer variants, in spite of their worst-case $O(T^{-1/2})$ dependence on iterations.

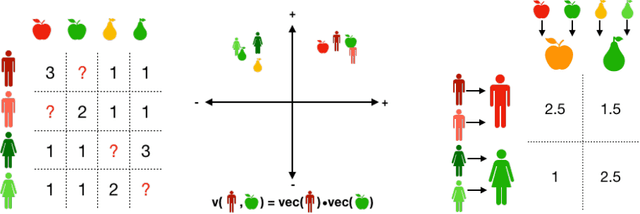

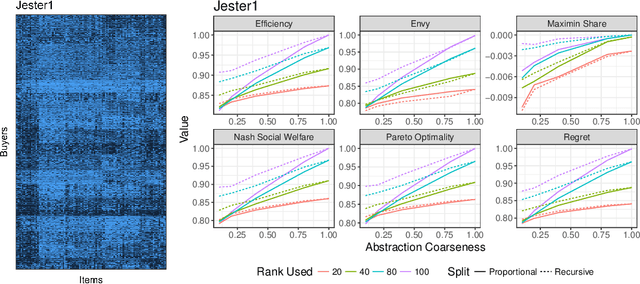

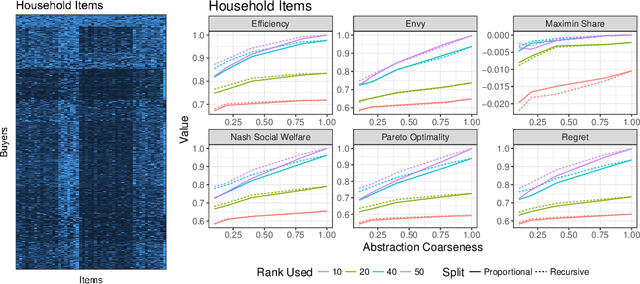

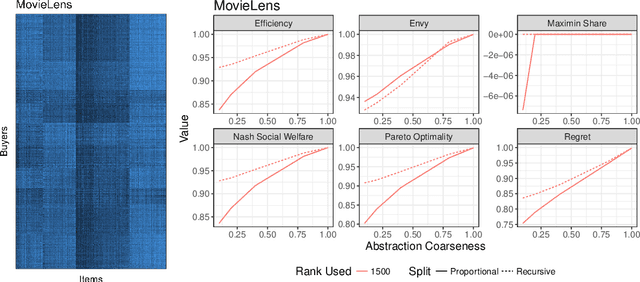

Computing large market equilibria using abstractions

Jan 18, 2019

Computing market equilibria is an important practical problem for market design (e.g. fair division, item allocation). However, computing equilibria requires large amounts of information (e.g. all valuations for all buyers for all items) and compute power. We consider ameliorating these issues by applying a method used for solving complex games: constructing a coarsened abstraction of a given market, solving for the equilibrium in the abstraction, and lifting the prices and allocations back to the original market. We show how to bound important quantities such as regret, envy, Nash social welfare, Pareto optimality, and maximin share when the abstracted prices and allocations are used in place of the real equilibrium. We then study two abstraction methods of interest for practitioners: 1) filling in unknown valuations using techniques from matrix completion, 2) reducing the problem size by aggregating groups of buyers/items into smaller numbers of representative buyers/items and solving for equilibrium in this coarsened market. We find that in real data allocations/prices that are relatively close to equilibria can be computed from even very coarse abstractions.

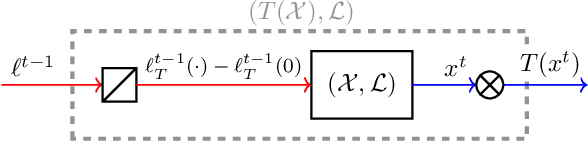

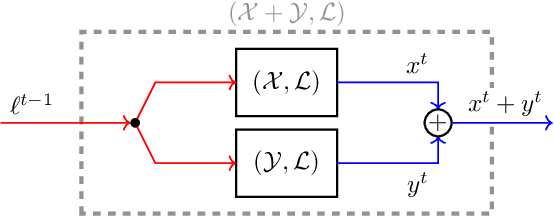

Composability of Regret Minimizers

Nov 06, 2018

Regret minimization is a powerful tool for solving large-scale problems; it was recently used in breakthrough results for large-scale extensive-form-game solving. This was achieved by composing simplex regret minimizers into an overall regret-minimization framework for extensive-form-game strategy spaces. In this paper we study the general composability of regret minimizers. We derive a calculus for constructing regret minimizers for complex convex sets that are constructed from convexity-preserving operations on simpler convex sets. In particular, we show that local regret minimizers for the simpler sets can be composed with additional regret minimizers into an aggregate regret minimizer for the complex set. As an application of our framework we show that the CFR framework can be constructed easily from our framework. We also show how to construct a CFR variant for extensive-form games with strategy constraints. Unlike a recently proposed variant of CFR for strategy constraints by Davis, Waugh, and Bowling (2018), the algorithm resulting from our calculus does not depend on any unknown constants and thus avoids binary search.

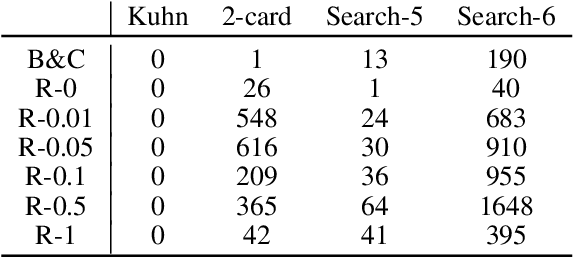

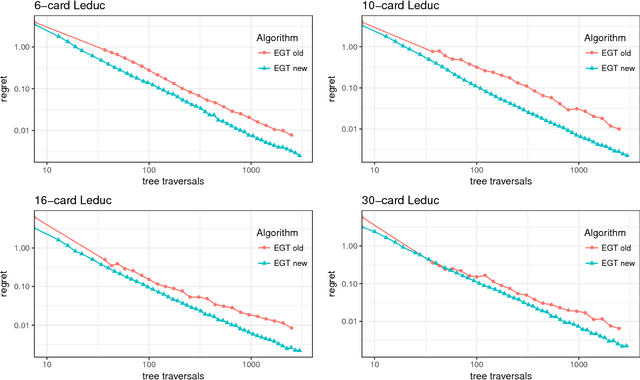

Solving Large Sequential Games with the Excessive Gap Technique

Oct 07, 2018

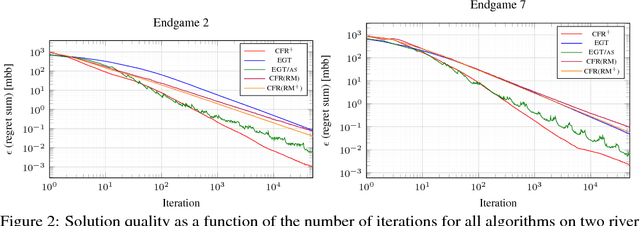

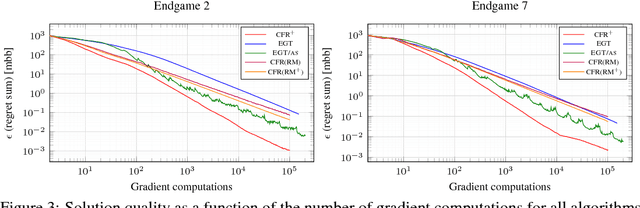

There has been tremendous recent progress on equilibrium-finding algorithms for zero-sum imperfect-information extensive-form games, but there has been a puzzling gap between theory and practice. First-order methods have significantly better theoretical convergence rates than any counterfactual-regret minimization (CFR) variant. Despite this, CFR variants have been favored in practice. Experiments with first-order methods have only been conducted on small- and medium-sized games because those methods are complicated to implement in this setting, and because CFR variants have been enhanced extensively for over a decade they perform well in practice. In this paper we show that a particular first-order method, a state-of-the-art variant of the excessive gap technique---instantiated with the dilated entropy distance function---can efficiently solve large real-world problems competitively with CFR and its variants. We show this on large endgames encountered by the Libratus poker AI, which recently beat top human poker specialist professionals at no-limit Texas hold'em. We show experimental results on our variant of the excessive gap technique as well as a prior version. We introduce a numerically friendly implementation of the smoothed best response computation associated with first-order methods for extensive-form game solving. We present, to our knowledge, the first GPU implementation of a first-order method for extensive-form games. We present comparisons of several excessive gap technique and CFR variants.

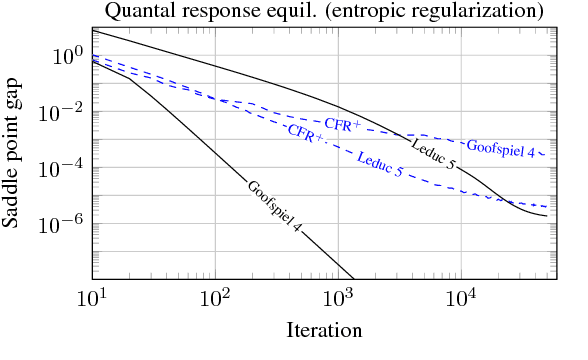

Online Convex Optimization for Sequential Decision Processes and Extensive-Form Games

Sep 10, 2018

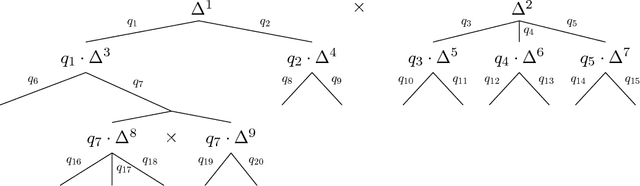

Regret minimization is a powerful tool for solving large-scale extensive-form games. State-of-the-art methods rely on minimizing regret locally at each decision point. In this work we derive a new framework for regret minimization on sequential decision problems and extensive-form games with general compact convex sets at each decision point and general convex losses, as opposed to prior work which has been for simplex decision points and linear losses. We call our framework laminar regret decomposition. It generalizes the CFR algorithm to this more general setting. Furthermore, our framework enables a new proof of CFR even in the known setting, which is derived from a perspective of decomposing polytope regret, thereby leading to an arguably simpler interpretation of the algorithm. Our generalization to convex compact sets and convex losses allows us to develop new algorithms for several problems: regularized sequential decision making, regularized Nash equilibria in extensive-form games, and computing approximate extensive-form perfect equilibria. Our generalization also leads to the first regret-minimization algorithm for computing reduced-normal-form quantal response equilibria based on minimizing local regrets. Experiments show that our framework leads to algorithms that scale at a rate comparable to the fastest variants of counterfactual regret minimization for computing Nash equilibrium, and therefore our approach leads to the first algorithm for computing quantal response equilibria in extremely large games. Finally we show that our framework enables a new kind of scalable opponent exploitation approach.

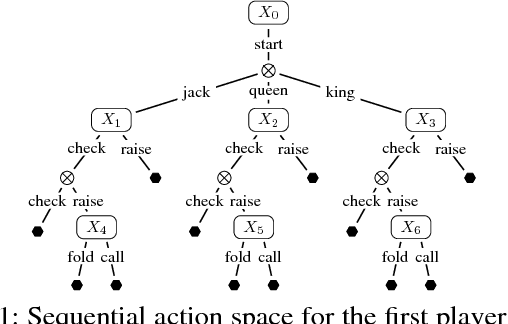

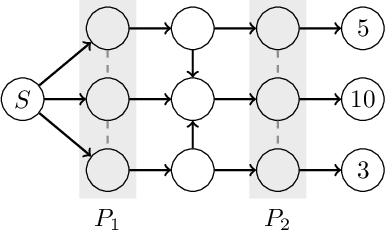

Robust Stackelberg Equilibria in Extensive-Form Games and Extension to Limited Lookahead

Nov 21, 2017

Stackelberg equilibria have become increasingly important as a solution concept in computational game theory, largely inspired by practical problems such as security settings. In practice, however, there is typically uncertainty regarding the model about the opponent. This paper is, to our knowledge, the first to investigate Stackelberg equilibria under uncertainty in extensive-form games, one of the broadest classes of game. We introduce robust Stackelberg equilibria, where the uncertainty is about the opponent's payoffs, as well as ones where the opponent has limited lookahead and the uncertainty is about the opponent's node evaluation function. We develop a new mixed-integer program for the deterministic limited-lookahead setting. We then extend the program to the robust setting for Stackelberg equilibrium under unlimited and under limited lookahead by the opponent. We show that for the specific case of interval uncertainty about the opponent's payoffs (or about the opponent's node evaluations in the case of limited lookahead), robust Stackelberg equilibria can be computed with a mixed-integer program that is of the same asymptotic size as that for the deterministic setting.

Regret Minimization in Behaviorally-Constrained Zero-Sum Games

Nov 09, 2017

No-regret learning has emerged as a powerful tool for solving extensive-form games. This was facilitated by the counterfactual-regret minimization (CFR) framework, which relies on the instantiation of regret minimizers for simplexes at each information set of the game. We use an instantiation of the CFR framework to develop algorithms for solving behaviorally-constrained (and, as a special case, perturbed in the Selten sense) extensive-form games, which allows us to compute approximate Nash equilibrium refinements. Nash equilibrium refinements are motivated by a major deficiency in Nash equilibrium: it provides virtually no guarantees on how it will play in parts of the game tree that are reached with zero probability. Refinements can mend this issue, but have not been adopted in practice, mostly due to a lack of scalable algorithms. We show that, compared to standard algorithms, our method finds solutions that have substantially better refinement properties, while enjoying a convergence rate that is comparable to that of state-of-the-art algorithms for Nash equilibrium computation both in theory and practice.

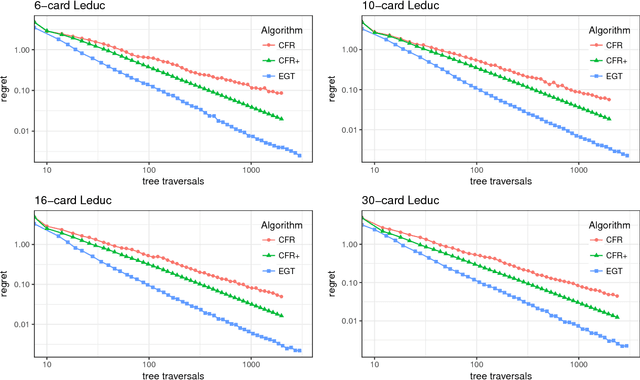

Theoretical and Practical Advances on Smoothing for Extensive-Form Games

May 09, 2017

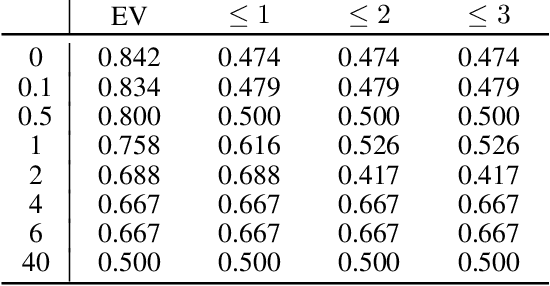

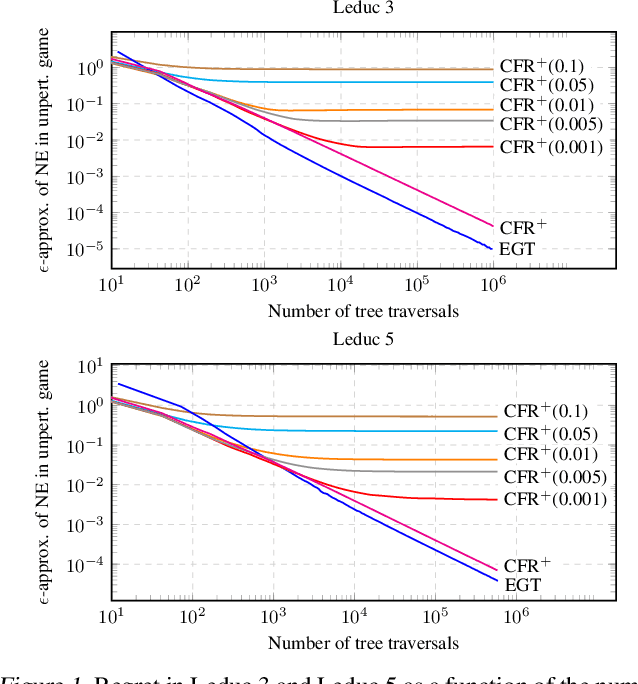

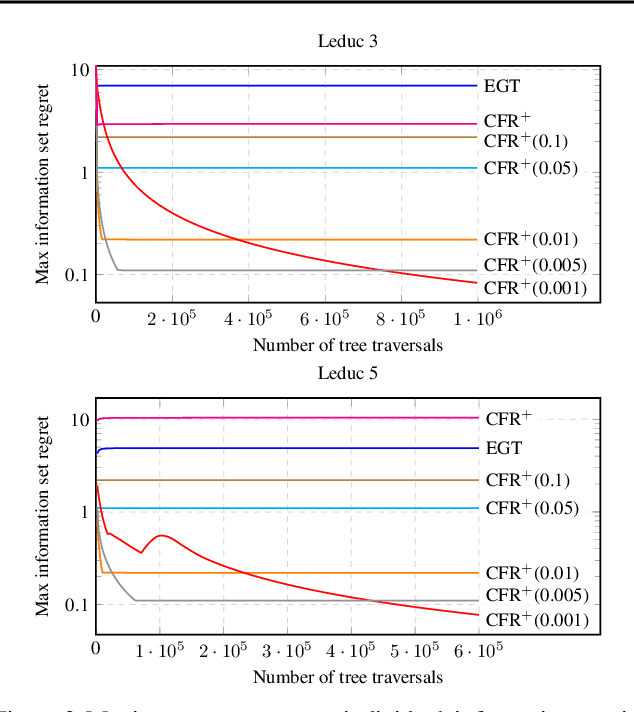

Sparse iterative methods, in particular first-order methods, are known to be among the most effective in solving large-scale two-player zero-sum extensive-form games. The convergence rates of these methods depend heavily on the properties of the distance-generating function that they are based on. We investigate the acceleration of first-order methods for solving extensive-form games through better design of the dilated entropy function---a class of distance-generating functions related to the domains associated with the extensive-form games. By introducing a new weighting scheme for the dilated entropy function, we develop the first distance-generating function for the strategy spaces of sequential games that has no dependence on the branching factor of the player. This result improves the convergence rate of several first-order methods by a factor of $\Omega(b^dd)$, where $b$ is the branching factor of the player, and $d$ is the depth of the game tree. Thus far, counterfactual regret minimization methods have been faster in practice, and more popular, than first-order methods despite their theoretically inferior convergence rates. Using our new weighting scheme and practical tuning we show that, for the first time, the excessive gap technique can be made faster than the fastest counterfactual regret minimization algorithm, CFR+, in practice.

Arbitrage-Free Combinatorial Market Making via Integer Programming

Jun 10, 2016

We present a new combinatorial market maker that operates arbitrage-free combinatorial prediction markets specified by integer programs. Although the problem of arbitrage-free pricing, while maintaining a bound on the subsidy provided by the market maker, is #P-hard in the worst case, we posit that the typical case might be amenable to modern integer programming (IP) solvers. At the crux of our method is the Frank-Wolfe (conditional gradient) algorithm which is used to implement a Bregman projection aligned with the market maker's cost function, using an IP solver as an oracle. We demonstrate the tractability and improved accuracy of our approach on real-world prediction market data from combinatorial bets placed on the 2010 NCAA Men's Division I Basketball Tournament, where the outcome space is of size 2^63. To our knowledge, this is the first implementation and empirical evaluation of an arbitrage-free combinatorial prediction market on this scale.