Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeCODA: Rewriting Transformer Blocks as GEMM-Epilogue Programs

May 20, 2026Transformer training systems are built around dense linear algebra, yet a nontrivial fraction of end-to-end time is spent on surrounding memory-bound operators. Normalization, activations, residual updates, reductions, and related computations repeatedly move large intermediate tensors through global memory while performing little arithmetic, making data movement an increasingly important bottleneck in otherwise highly optimized training stacks. We introduce CODA, a GPU kernel abstraction that expresses these computations as GEMM-plus-epilogue programs. CODA is based on the observation that many Transformer operators exposed as separate framework kernels can be algebraically reparameterized to execute while a GEMM output tile remains on chip, before it is written to memory. The abstraction fixes the GEMM mainloop and exposes a small set of composable epilogue primitives for scaling, reductions, pairwise transformations, and accumulation. This constrained interface preserves the performance structure of expert-written GEMMs while remaining expressive enough to cover nearly all non-attention computation in the forward and backward pass of a standard Transformer block. Across representative Transformer workloads, both human- and LLM-authored CODA kernels achieve high performance, suggesting that GEMM-plus-epilogue programming offers a practical path toward combining framework-level productivity with hardware-level efficiency.

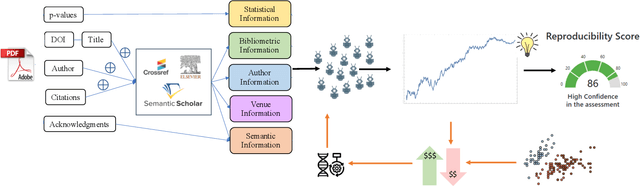

A Synthetic Prediction Market for Estimating Confidence in Published Work

Dec 23, 2021

Explainably estimating confidence in published scholarly work offers opportunity for faster and more robust scientific progress. We develop a synthetic prediction market to assess the credibility of published claims in the social and behavioral sciences literature. We demonstrate our system and detail our findings using a collection of known replication projects. We suggest that this work lays the foundation for a research agenda that creatively uses AI for peer review.

Design and Analysis of a Synthetic Prediction Market using Dynamic Convex Sets

Jan 05, 2021

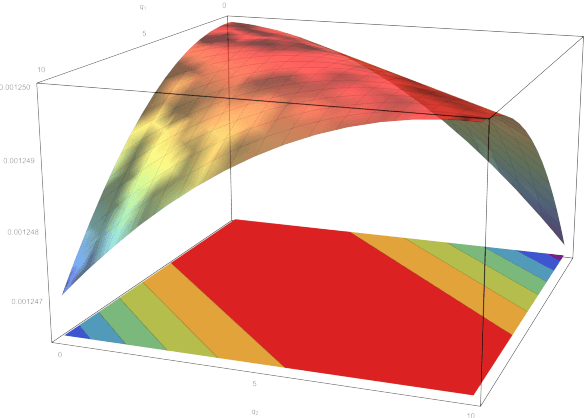

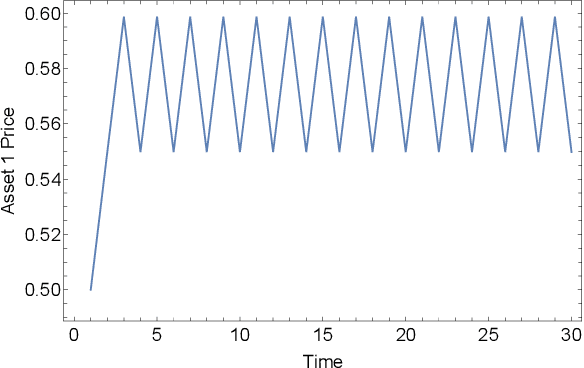

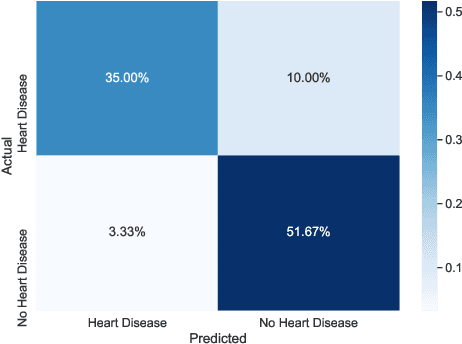

We present a synthetic prediction market whose agent purchase logic is defined using a sigmoid transformation of a convex semi-algebraic set defined in feature space. Asset prices are determined by a logarithmic scoring market rule. Time varying asset prices affect the structure of the semi-algebraic sets leading to time-varying agent purchase rules. We show that under certain assumptions on the underlying geometry, the resulting synthetic prediction market can be used to arbitrarily closely approximate a binary function defined on a set of input data. We also provide sufficient conditions for market convergence and show that under certain instances markets can exhibit limit cycles in asset spot price. We provide an evolutionary algorithm for training agent parameters to allow a market to model the distribution of a given data set and illustrate the market approximation using two open source data sets. Results are compared to standard machine learning methods.