Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeOffline Contextual Bandits in the Presence of New Actions

May 18, 2026Automated decision-making algorithms drive applications such as recommendation systems and search engines. These algorithms often rely on off-policy contextual bandits or off-policy learning (OPL). Conventionally, OPL selects actions that maximize the expected reward from an existing action set. However, in many real-world scenarios, actions, such as news articles or video content, change continuously, and the action space evolves over time after data collection. We define actions introduced after deploying the logging policy as new actions and focus on OPL with new actions. Existing OPL methods identify optimal actions from the existing set effectively but cannot learn and select new actions because no relevant data are logged. To address this limitation, we propose a new OPL method that leverages action features. We first introduce the Local Combination PseudoInverse (LCPI) estimator for the policy gradient, generalizing the PseudoInverse estimator initially proposed for off-policy evaluation of slate bandits. LCPI controls the trade-off between reward-modeling condition and the condition for data collection regarding the action features, capturing the interaction effects among different dimensions of action features. Furthermore, we propose a generalized algorithm called Policy Optimization for Effective New Actions (PONA), which integrates LCPI, a component specialized for new action selection, with Doubly Robust (DR), which excels at learning within existing actions. We define PONA as a weighted sum of the LCPI and DR estimators, optimizing both the selection of existing and new actions, and allowing the proportion of new action selections to be adjusted by the weight parameter. Through extensive experiments, we demonstrate that PONA efficiently selects new actions while maintaining the overall policy performance as opposed to most existing methods that cannot select new actions.

Off-Policy Evaluation for Ranking Policies under Deterministic Logging Policies

Mar 23, 2026Off-Policy Evaluation (OPE) is an important practical problem in algorithmic ranking systems, where the goal is to estimate the expected performance of a new ranking policy using only offline logged data collected under a different, logging policy. Existing estimators, such as the ranking-wise and position-wise inverse propensity score (IPS) estimators, require the data collection policy to be sufficiently stochastic and suffer from severe bias when the logging policy is fully deterministic. In this paper, we propose novel estimators, Click-based Inverse Propensity Score (CIPS), exploiting the intrinsic stochasticity of user click behavior to address this challenge. Unlike existing methods that rely on the stochasticity of the logging policy, our approach uses click probability as a new form of importance weighting, enabling low-bias OPE even under deterministic logging policies where existing methods incur substantial bias. We provide theoretical analyses of the bias and variance properties of the proposed estimators and show, through synthetic and real-world experiments, that our estimators achieve significantly lower bias compared to strong baselines, for a range of experimental settings with completely deterministic logging policies.

Off-Policy Learning with Limited Supply

Mar 19, 2026We study off-policy learning (OPL) in contextual bandits, which plays a key role in a wide range of real-world applications such as recommendation systems and online advertising. Typical OPL in contextual bandits assumes an unconstrained environment where a policy can select the same item infinitely. However, in many practical applications, including coupon allocation and e-commerce, limited supply constrains items through budget limits on distributed coupons or inventory restrictions on products. In these settings, greedily selecting the item with the highest expected reward for the current user may lead to early depletion of that item, making it unavailable for future users who could potentially generate higher expected rewards. As a result, OPL methods that are optimal in unconstrained settings may become suboptimal in limited supply settings. To address the issue, we provide a theoretical analysis showing that conventional greedy OPL approaches may fail to maximize the policy performance, and demonstrate that policies with superior performance must exist in limited supply settings. Based on this insight, we introduce a novel method called Off-Policy learning with Limited Supply (OPLS). Rather than simply selecting the item with the highest expected reward, OPLS focuses on items with relatively higher expected rewards compared to the other users, enabling more efficient allocation of items with limited supply. Our empirical results on both synthetic and real-world datasets show that OPLS outperforms existing OPL methods in contextual bandit problems with limited supply.

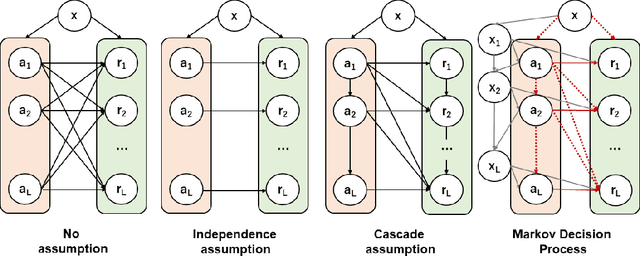

Off-Policy Evaluation of Ranking Policies under Diverse User Behavior

Jun 26, 2023Ranking interfaces are everywhere in online platforms. There is thus an ever growing interest in their Off-Policy Evaluation (OPE), aiming towards an accurate performance evaluation of ranking policies using logged data. A de-facto approach for OPE is Inverse Propensity Scoring (IPS), which provides an unbiased and consistent value estimate. However, it becomes extremely inaccurate in the ranking setup due to its high variance under large action spaces. To deal with this problem, previous studies assume either independent or cascade user behavior, resulting in some ranking versions of IPS. While these estimators are somewhat effective in reducing the variance, all existing estimators apply a single universal assumption to every user, causing excessive bias and variance. Therefore, this work explores a far more general formulation where user behavior is diverse and can vary depending on the user context. We show that the resulting estimator, which we call Adaptive IPS (AIPS), can be unbiased under any complex user behavior. Moreover, AIPS achieves the minimum variance among all unbiased estimators based on IPS. We further develop a procedure to identify the appropriate user behavior model to minimize the mean squared error (MSE) of AIPS in a data-driven fashion. Extensive experiments demonstrate that the empirical accuracy improvement can be significant, enabling effective OPE of ranking systems even under diverse user behavior.

Counterfactual Learning with General Data-generating Policies

Dec 04, 2022

Off-policy evaluation (OPE) attempts to predict the performance of counterfactual policies using log data from a different policy. We extend its applicability by developing an OPE method for a class of both full support and deficient support logging policies in contextual-bandit settings. This class includes deterministic bandit (such as Upper Confidence Bound) as well as deterministic decision-making based on supervised and unsupervised learning. We prove that our method's prediction converges in probability to the true performance of a counterfactual policy as the sample size increases. We validate our method with experiments on partly and entirely deterministic logging policies. Finally, we apply it to evaluate coupon targeting policies by a major online platform and show how to improve the existing policy.

Policy-Adaptive Estimator Selection for Off-Policy Evaluation

Nov 25, 2022

Off-policy evaluation (OPE) aims to accurately evaluate the performance of counterfactual policies using only offline logged data. Although many estimators have been developed, there is no single estimator that dominates the others, because the estimators' accuracy can vary greatly depending on a given OPE task such as the evaluation policy, number of actions, and noise level. Thus, the data-driven estimator selection problem is becoming increasingly important and can have a significant impact on the accuracy of OPE. However, identifying the most accurate estimator using only the logged data is quite challenging because the ground-truth estimation accuracy of estimators is generally unavailable. This paper studies this challenging problem of estimator selection for OPE for the first time. In particular, we enable an estimator selection that is adaptive to a given OPE task, by appropriately subsampling available logged data and constructing pseudo policies useful for the underlying estimator selection task. Comprehensive experiments on both synthetic and real-world company data demonstrate that the proposed procedure substantially improves the estimator selection compared to a non-adaptive heuristic.

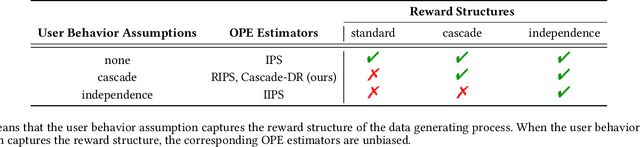

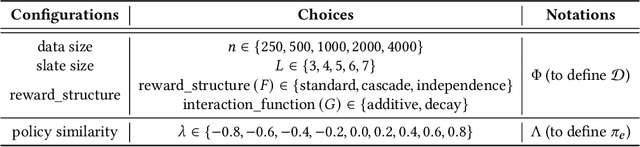

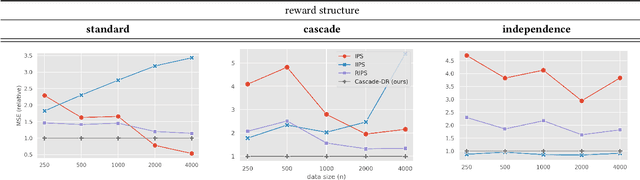

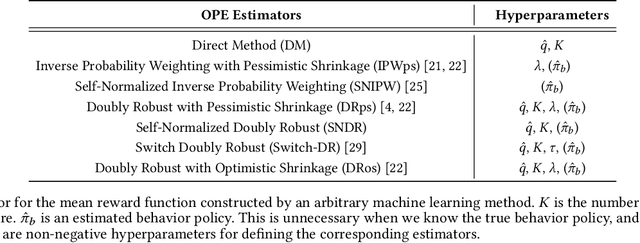

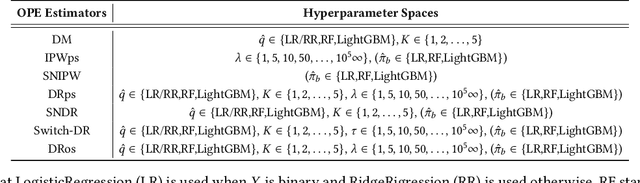

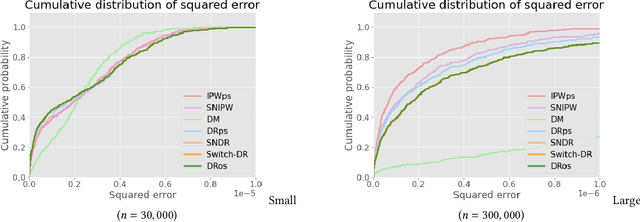

Doubly Robust Off-Policy Evaluation for Ranking Policies under the Cascade Behavior Model

Feb 03, 2022

In real-world recommender systems and search engines, optimizing ranking decisions to present a ranked list of relevant items is critical. Off-policy evaluation (OPE) for ranking policies is thus gaining a growing interest because it enables performance estimation of new ranking policies using only logged data. Although OPE in contextual bandits has been studied extensively, its naive application to the ranking setting faces a critical variance issue due to the huge item space. To tackle this problem, previous studies introduce some assumptions on user behavior to make the combinatorial item space tractable. However, an unrealistic assumption may, in turn, cause serious bias. Therefore, appropriately controlling the bias-variance tradeoff by imposing a reasonable assumption is the key for success in OPE of ranking policies. To achieve a well-balanced bias-variance tradeoff, we propose the Cascade Doubly Robust estimator building on the cascade assumption, which assumes that a user interacts with items sequentially from the top position in a ranking. We show that the proposed estimator is unbiased in more cases compared to existing estimators that make stronger assumptions. Furthermore, compared to a previous estimator based on the same cascade assumption, the proposed estimator reduces the variance by leveraging a control variate. Comprehensive experiments on both synthetic and real-world data demonstrate that our estimator leads to more accurate OPE than existing estimators in a variety of settings.

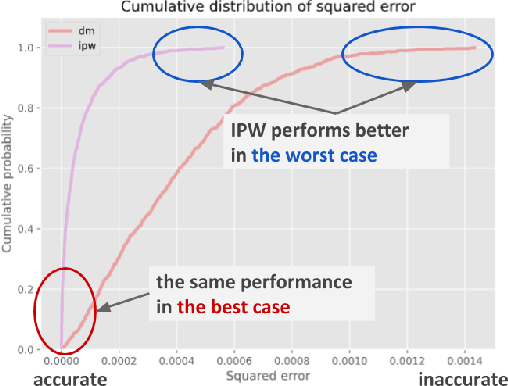

Evaluating the Robustness of Off-Policy Evaluation

Aug 31, 2021

Off-policy Evaluation (OPE), or offline evaluation in general, evaluates the performance of hypothetical policies leveraging only offline log data. It is particularly useful in applications where the online interaction involves high stakes and expensive setting such as precision medicine and recommender systems. Since many OPE estimators have been proposed and some of them have hyperparameters to be tuned, there is an emerging challenge for practitioners to select and tune OPE estimators for their specific application. Unfortunately, identifying a reliable estimator from results reported in research papers is often difficult because the current experimental procedure evaluates and compares the estimators' performance on a narrow set of hyperparameters and evaluation policies. Therefore, it is difficult to know which estimator is safe and reliable to use. In this work, we develop Interpretable Evaluation for Offline Evaluation (IEOE), an experimental procedure to evaluate OPE estimators' robustness to changes in hyperparameters and/or evaluation policies in an interpretable manner. Then, using the IEOE procedure, we perform extensive evaluation of a wide variety of existing estimators on Open Bandit Dataset, a large-scale public real-world dataset for OPE. We demonstrate that our procedure can evaluate the estimators' robustness to the hyperparamter choice, helping us avoid using unsafe estimators. Finally, we apply IEOE to real-world e-commerce platform data and demonstrate how to use our protocol in practice.

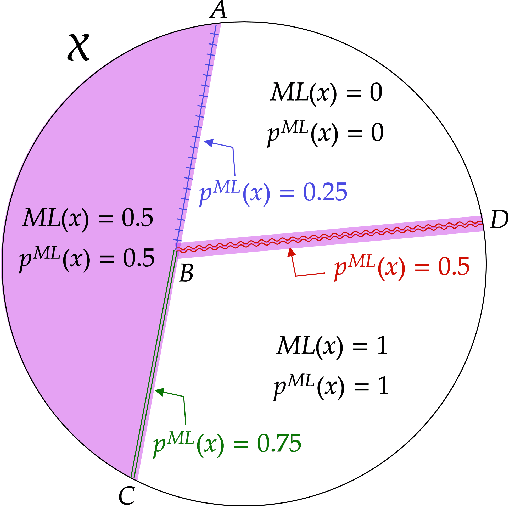

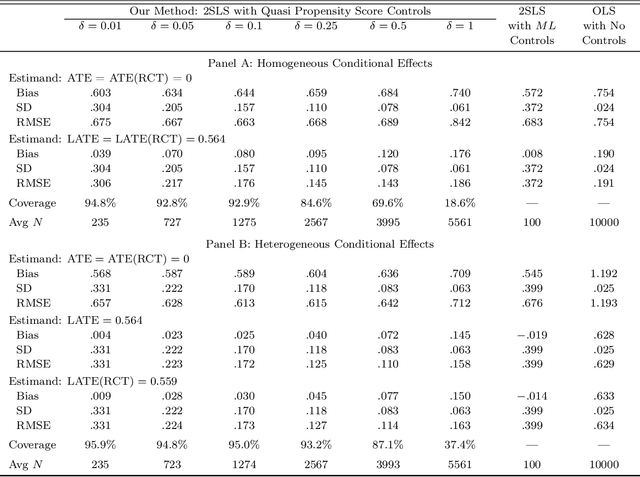

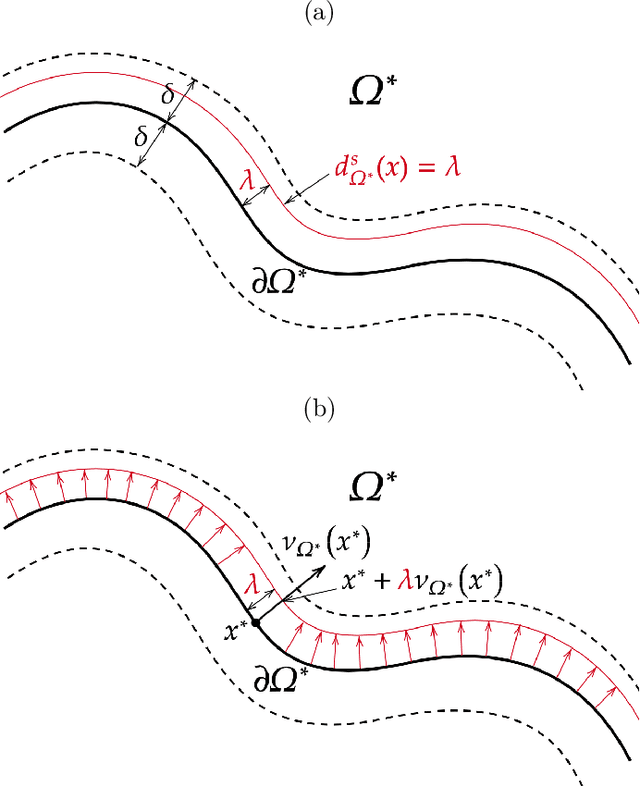

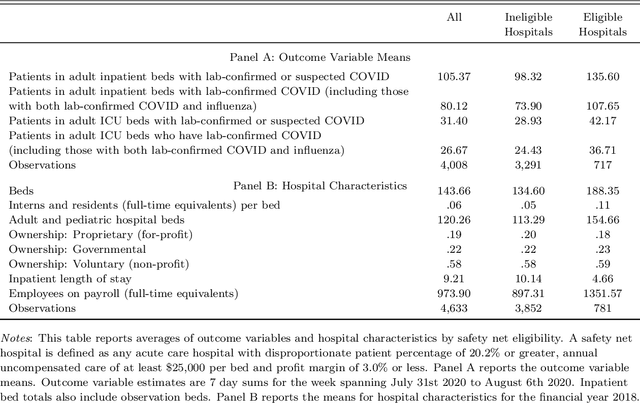

Algorithm is Experiment: Machine Learning, Market Design, and Policy Eligibility Rules

Apr 26, 2021

Algorithms produce a growing portion of decisions and recommendations both in policy and business. Such algorithmic decisions are natural experiments (conditionally quasi-randomly assigned instruments) since the algorithms make decisions based only on observable input variables. We use this observation to develop a treatment-effect estimator for a class of stochastic and deterministic algorithms. Our estimator is shown to be consistent and asymptotically normal for well-defined causal effects. A key special case of our estimator is a high-dimensional regression discontinuity design. The proofs use tools from differential geometry and geometric measure theory, which may be of independent interest. The practical performance of our method is first demonstrated in a high-dimensional simulation resembling decision-making by machine learning algorithms. Our estimator has smaller mean squared errors compared to alternative estimators. We finally apply our estimator to evaluate the effect of Coronavirus Aid, Relief, and Economic Security (CARES) Act, where more than \$10 billion worth of relief funding is allocated to hospitals via an algorithmic rule. The estimates suggest that the relief funding has little effects on COVID-19-related hospital activity levels. Naive OLS and IV estimates exhibit substantial selection bias.

A Large-scale Open Dataset for Bandit Algorithms

Aug 17, 2020

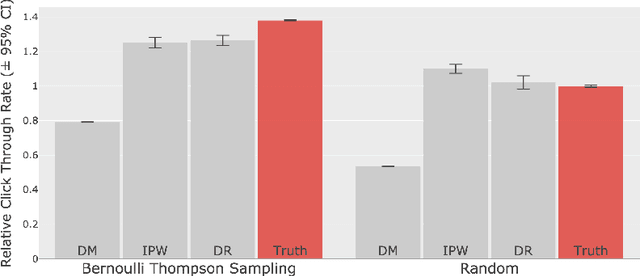

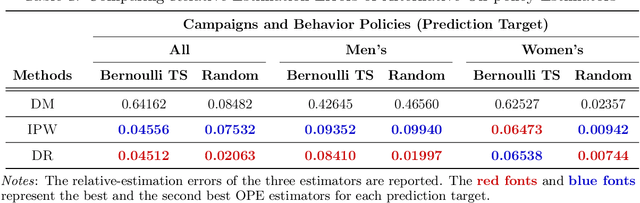

We build and publicize the Open Bandit Dataset and Pipeline to facilitate scalable and reproducible research on bandit algorithms. They are especially suitable for off-policy evaluation (OPE), which attempts to predict the performance of hypothetical algorithms using data generated by a different algorithm. We construct the dataset based on experiments and implementations on a large-scale fashion e-commerce platform, ZOZOTOWN. The data contain the ground-truth about the performance of several bandit policies and enable the fair comparisons of different OPE estimators. We also provide a pipeline to make its implementation easy and consistent. As a proof of concept, we use the dataset and pipeline to implement and evaluate OPE estimators. First, we find that a well-established estimator fails, suggesting that it is critical to choose an appropriate estimator. We then select a well-performing estimator and use it to improve the platform's fashion item recommendation. Our analysis succeeds in finding a counterfactual policy that significantly outperforms the historical ones. Our open data and pipeline will allow researchers and practitioners to easily evaluate and compare their bandit algorithms and OPE estimators with others in a large, real-world setting.