Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeTweedie's Formulae and Diffusion Generative Models Beyond Gaussian

May 19, 2026Diffusion models have achieved remarkable success in generating samples from unknown data distributions. Most popular stochastic differential equation-based diffusion models perturb the target distribution by adding Gaussian noise, transforming it into a simple prior, and then use denoising score matching, a consequence of Tweedie's formula, to learn the score function and generate clean samples from noise. However, non-Gaussian diffusion models with state-dependent diffusion coefficient have been largely underexplored, as have the corresponding Tweedie's formulae. In this work, we extend Tweedie's formula to important non-Gaussian processes, including geometric Brownian motion (GBM), squared Bessel (BESQ) processes, and Cox-Ingersoll-Ross (CIR) processes, thereby yielding the corresponding denoising score-matching objectives. We then apply the derived formulae to image and financial time series generation using GBM- and CIR-based diffusion models, and to empirical Bayes estimation under the BESQ setting. The reported experimental results demonstrate the potential of non-Gaussian models.

Amortized Guidance for Image Inpainting with Pretrained Diffusion Models

May 13, 2026We study image inpainting with generative diffusion models. Existing methods typically either train dedicated task-specific models, or adapt a pretrained diffusion model separately for each masked image at deployment. We introduce a middle-ground model, termed Amortized Inpainting with Diffusion (AID), which keeps a pretrained diffusion backbone fixed, trains a small reusable guidance module offline, and then reuses it across masked images without per-instance optimization. We formulate it as a deterministic guidance problem with a supervised terminal objective. To make this problem learnable in high dimensions, we derive an auxiliary Gaussian formulation and prove that solving this randomized problem recovers the optimal deterministic guidance field. This bridge yields a principled continuous-time actor--critic algorithm for learning the guidance module in a fully data-driven manner. Empirically, on AFHQv2 and FFHQ under the pixel EDM pipeline and on ImageNet under the latent EDM2 pipeline, AID consistently improves the quality--speed trade-off over strong fixed-backbone and amortized inpainting baselines across multiple mask types, while adding less than one percent trainable overhead.

Data-driven generative simulation of SDEs using diffusion models

Sep 10, 2025

This paper introduces a new approach to generating sample paths of unknown stochastic differential equations (SDEs) using diffusion models, a class of generative AI models commonly employed in image and video applications. Unlike the traditional Monte Carlo methods for simulating SDEs, which require explicit specifications of the drift and diffusion coefficients, our method takes a model-free, data-driven approach. Given a finite set of sample paths from an SDE, we utilize conditional diffusion models to generate new, synthetic paths of the same SDE. To demonstrate the effectiveness of our approach, we conduct a simulation experiment to compare our method with alternative benchmark ones including neural SDEs. Furthermore, in an empirical study we leverage these synthetically generated sample paths to enhance the performance of reinforcement learning algorithms for continuous-time mean-variance portfolio selection, hinting promising applications of diffusion models in financial analysis and decision-making.

Regret of exploratory policy improvement and $q$-learning

Nov 02, 2024

We study the convergence of $q$-learning and related algorithms introduced by Jia and Zhou (J. Mach. Learn. Res., 24 (2023), 161) for controlled diffusion processes. Under suitable conditions on the growth and regularity of the model parameters, we provide a quantitative error and regret analysis of both the exploratory policy improvement algorithm and the $q$-learning algorithm.

Reward-Directed Score-Based Diffusion Models via q-Learning

Sep 07, 2024

We propose a new reinforcement learning (RL) formulation for training continuous-time score-based diffusion models for generative AI to generate samples that maximize reward functions while keeping the generated distributions close to the unknown target data distributions. Different from most existing studies, our formulation does not involve any pretrained model for the unknown score functions of the noise-perturbed data distributions. We present an entropy-regularized continuous-time RL problem and show that the optimal stochastic policy has a Gaussian distribution with a known covariance matrix. Based on this result, we parameterize the mean of Gaussian policies and develop an actor-critic type (little) q-learning algorithm to solve the RL problem. A key ingredient in our algorithm design is to obtain noisy observations from the unknown score function via a ratio estimator. Numerically, we show the effectiveness of our approach by comparing its performance with two state-of-the-art RL methods that fine-tune pretrained models. Finally, we discuss extensions of our RL formulation to probability flow ODE implementation of diffusion models and to conditional diffusion models.

Sublinear Regret for An Actor-Critic Algorithm in Continuous-Time Linear-Quadratic Reinforcement Learning

Jul 24, 2024

We study reinforcement learning (RL) for a class of continuous-time linear-quadratic (LQ) control problems for diffusions where volatility of the state processes depends on both state and control variables. We apply a model-free approach that relies neither on knowledge of model parameters nor on their estimations, and devise an actor-critic algorithm to learn the optimal policy parameter directly. Our main contributions include the introduction of a novel exploration schedule and a regret analysis of the proposed algorithm. We provide the convergence rate of the policy parameter to the optimal one, and prove that the algorithm achieves a regret bound of $O(N^{\frac{3}{4}})$ up to a logarithmic factor. We conduct a simulation study to validate the theoretical results and demonstrate the effectiveness and reliability of the proposed algorithm. We also perform numerical comparisons between our method and those of the recent model-based stochastic LQ RL studies adapted to the state- and control-dependent volatility setting, demonstrating a better performance of the former in terms of regret bounds.

Reinforcement Learning for Jump-Diffusions

May 26, 2024

We study continuous-time reinforcement learning (RL) for stochastic control in which system dynamics are governed by jump-diffusion processes. We formulate an entropy-regularized exploratory control problem with stochastic policies to capture the exploration--exploitation balance essential for RL. Unlike the pure diffusion case initially studied by Wang et al. (2020), the derivation of the exploratory dynamics under jump-diffusions calls for a careful formulation of the jump part. Through a theoretical analysis, we find that one can simply use the same policy evaluation and q-learning algorithms in Jia and Zhou (2022a, 2023), originally developed for controlled diffusions, without needing to check a priori whether the underlying data come from a pure diffusion or a jump-diffusion. However, we show that the presence of jumps ought to affect parameterizations of actors and critics in general. Finally, we investigate as an application the mean-variance portfolio selection problem with stock price modelled as a jump-diffusion, and show that both RL algorithms and parameterizations are invariant with respect to jumps.

Learning Merton's Strategies in an Incomplete Market: Recursive Entropy Regularization and Biased Gaussian Exploration

Dec 19, 2023

We study Merton's expected utility maximization problem in an incomplete market, characterized by a factor process in addition to the stock price process, where all the model primitives are unknown. We take the reinforcement learning (RL) approach to learn optimal portfolio policies directly by exploring the unknown market, without attempting to estimate the model parameters. Based on the entropy-regularization framework for general continuous-time RL formulated in Wang et al. (2020), we propose a recursive weighting scheme on exploration that endogenously discounts the current exploration reward by the past accumulative amount of exploration. Such a recursive regularization restores the optimality of Gaussian exploration. However, contrary to the existing results, the optimal Gaussian policy turns out to be biased in general, due to the interwinding needs for hedging and for exploration. We present an asymptotic analysis of the resulting errors to show how the level of exploration affects the learned policies. Furthermore, we establish a policy improvement theorem and design several RL algorithms to learn Merton's optimal strategies. At last, we carry out both simulation and empirical studies with a stochastic volatility environment to demonstrate the efficiency and robustness of the RL algorithms in comparison to the conventional plug-in method.

Variable Clustering via Distributionally Robust Nodewise Regression

Dec 21, 2022

We study a multi-factor block model for variable clustering and connect it to the regularized subspace clustering by formulating a distributionally robust version of the nodewise regression. To solve the latter problem, we derive a convex relaxation, provide guidance on selecting the size of the robust region, and hence the regularization weighting parameter, based on the data, and propose an ADMM algorithm for implementation. We validate our method in an extensive simulation study. Finally, we propose and apply a variant of our method to stock return data, obtain interpretable clusters that facilitate portfolio selection and compare its out-of-sample performance with other clustering methods in an empirical study.

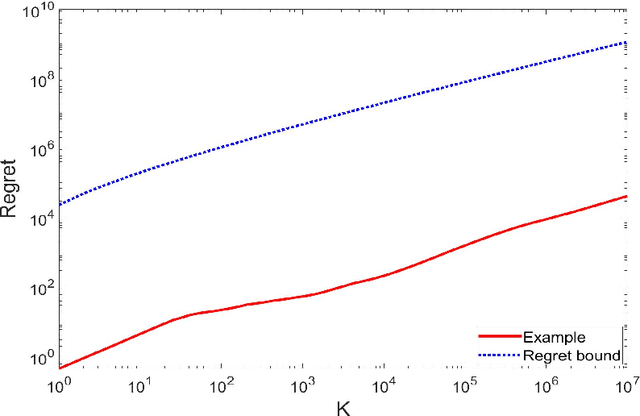

Square-root regret bounds for continuous-time episodic Markov decision processes

Oct 03, 2022

We study reinforcement learning for continuous-time Markov decision processes (MDPs) in the finite-horizon episodic setting. We present a learning algorithm based on the methods of value iteration and upper confidence bound. We derive an upper bound on the worst-case expected regret for the proposed algorithm, and establish a worst-case lower bound, both bounds are of the order of square-root on the number of episodes. Finally, we conduct simulation experiments to illustrate the performance of our algorithm.