Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeBERT for Long Documents: A Case Study of Automated ICD Coding

Nov 04, 2022

Transformer models have achieved great success across many NLP problems. However, previous studies in automated ICD coding concluded that these models fail to outperform some of the earlier solutions such as CNN-based models. In this paper we challenge this conclusion. We present a simple and scalable method to process long text with the existing transformer models such as BERT. We show that this method significantly improves the previous results reported for transformer models in ICD coding, and is able to outperform one of the prominent CNN-based methods.

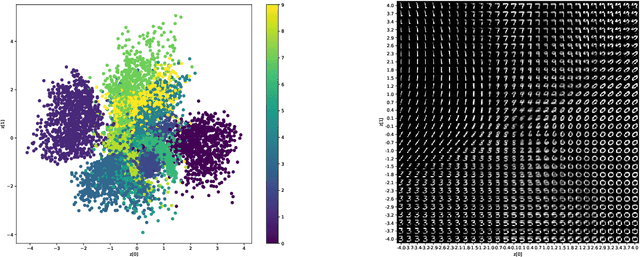

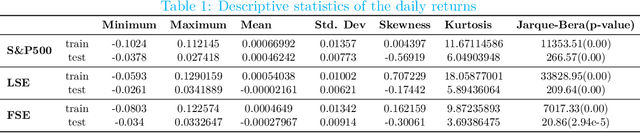

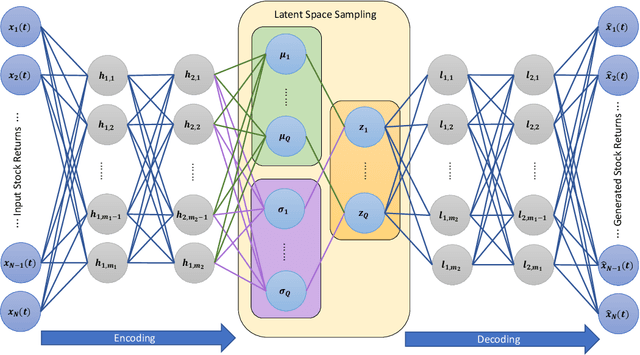

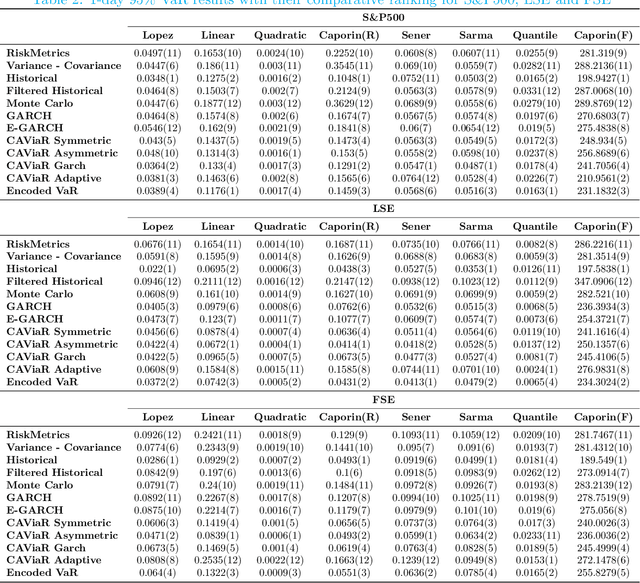

Encoded Value-at-Risk: A Predictive Machine for Financial Risk Management

Nov 13, 2020

Measuring risk is at the center of modern financial risk management. As the world economy is becoming more complex and standard modeling assumptions are violated, the advanced artificial intelligence solutions may provide the right tools to analyze the global market. In this paper, we provide a novel approach for measuring market risk called Encoded Value-at-Risk (Encoded VaR), which is based on a type of artificial neural network, called Variational Auto-encoders (VAEs). Encoded VaR is a generative model which can be used to reproduce market scenarios from a range of historical cross-sectional stock returns, while increasing the signal-to-noise ratio present in the financial data, and learning the dependency structure of the market without any assumptions about the joint distribution of stock returns. We compare Encoded VaR out-of-sample results with eleven other methods and show that it is competitive to many other well-known VaR algorithms presented in the literature.