Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

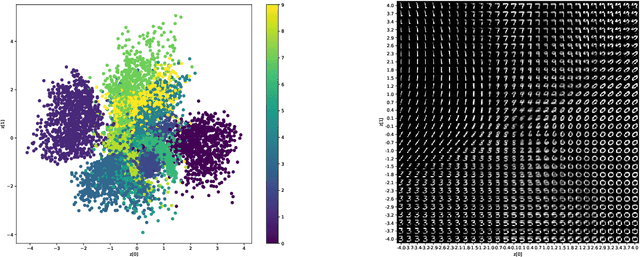

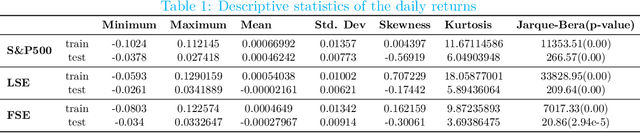

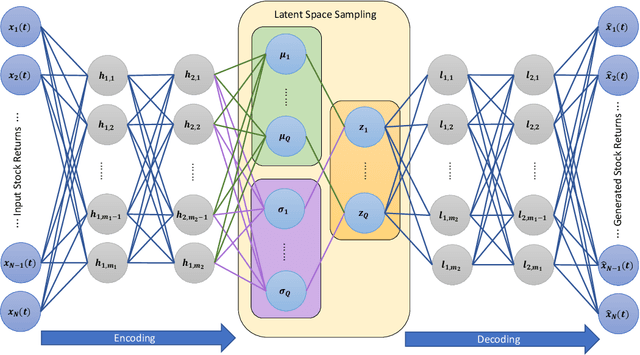

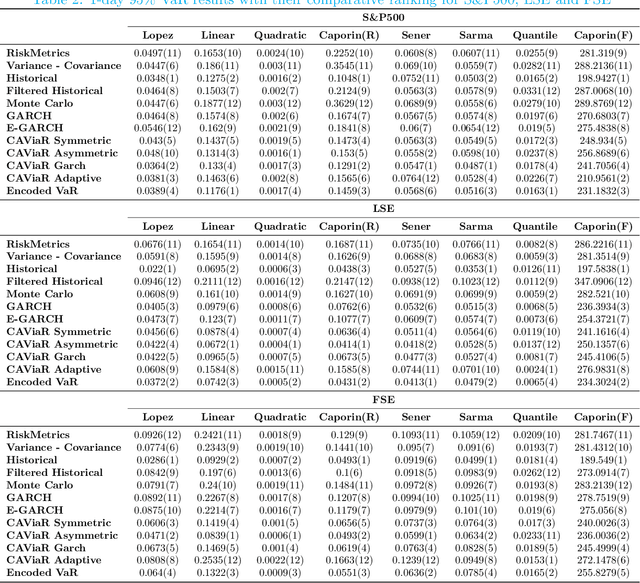

Add to EdgeEncoded Value-at-Risk: A Predictive Machine for Financial Risk Management

Nov 13, 2020

Measuring risk is at the center of modern financial risk management. As the world economy is becoming more complex and standard modeling assumptions are violated, the advanced artificial intelligence solutions may provide the right tools to analyze the global market. In this paper, we provide a novel approach for measuring market risk called Encoded Value-at-Risk (Encoded VaR), which is based on a type of artificial neural network, called Variational Auto-encoders (VAEs). Encoded VaR is a generative model which can be used to reproduce market scenarios from a range of historical cross-sectional stock returns, while increasing the signal-to-noise ratio present in the financial data, and learning the dependency structure of the market without any assumptions about the joint distribution of stock returns. We compare Encoded VaR out-of-sample results with eleven other methods and show that it is competitive to many other well-known VaR algorithms presented in the literature.

A Novel Classification Approach for Credit Scoring based on Gaussian Mixture Models

Oct 26, 2020

Credit scoring is a rapidly expanding analytical technique used by banks and other financial institutions. Academic studies on credit scoring provide a range of classification techniques used to differentiate between good and bad borrowers. The main contribution of this paper is to introduce a new method for credit scoring based on Gaussian Mixture Models. Our algorithm classifies consumers into groups which are labeled as positive or negative. Labels are estimated according to the probability associated with each class. We apply our model with real world databases from Australia, Japan, and Germany. Numerical results show that not only our model's performance is comparable to others, but also its flexibility avoids over-fitting even in the absence of standard cross validation techniques. The framework developed by this paper can provide a computationally efficient and powerful tool for assessment of consumer default risk in related financial institutions.

Forecasting Stock Market with Support Vector Regression and Butterfly Optimization Algorithm

May 27, 2019

Support Vector Regression (SVR) has achieved high performance on forecasting future behavior of random systems. However, the performance of SVR models highly depends upon the appropriate choice of SVR parameters. In this study, a novel BOA-SVR model based on Butterfly Optimization Algorithm (BOA) is presented. The performance of the proposed model is compared with eleven other meta-heuristic algorithms on a number of stocks from NASDAQ. The results indicate that the presented model here is capable to optimize the SVR parameters very well and indeed is one of the best models judged by both prediction performance accuracy and time consumption.