Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeRandomized Primal-Dual Algorithms for Composite Convex Minimization with Faster Convergence Rates

Mar 03, 2020

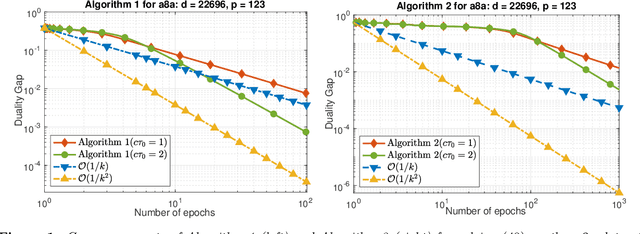

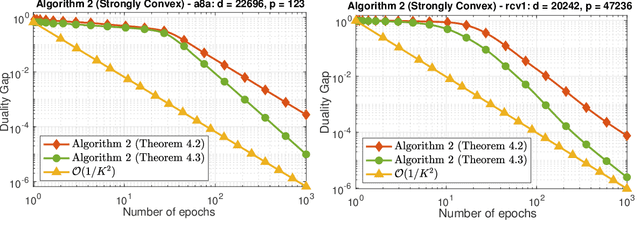

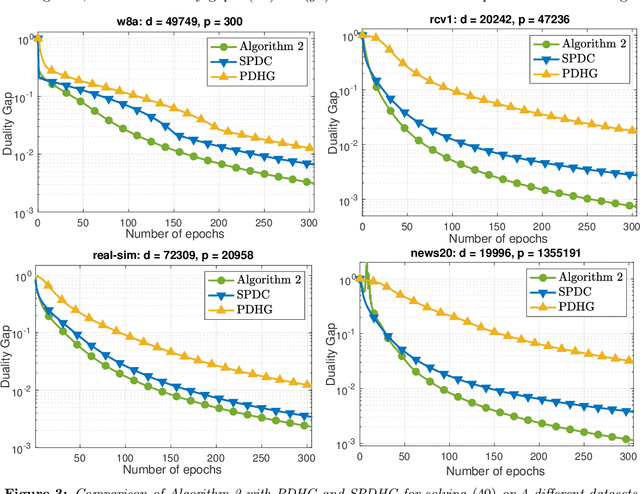

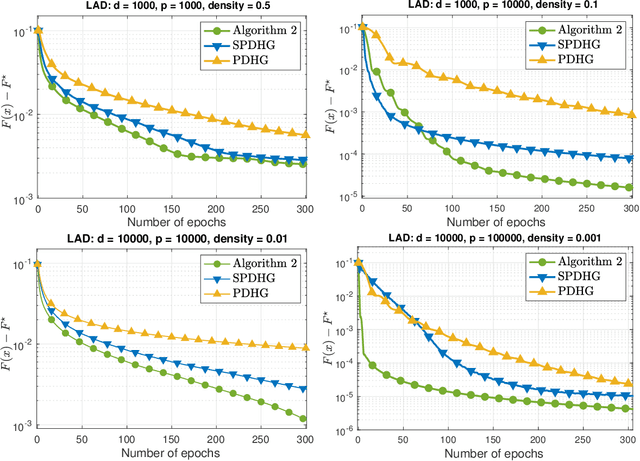

We develop two novel randomized primal-dual algorithms to solve nonsmooth composite convex optimization problems. The first algorithm is fully randomized, i.e., it has randomized updates on both primal and dual variables, while the second one is a semi-randomized scheme which only has one randomized update on the primal (or dual) variable while using the full update for the other. Both algorithms achieve the best-known $\mathcal{O}(1/k)$ or $\mathcal{O}(1/k^2)$ convergence rates in expectation under either only convexity or strong convexity, respectively, where $k$ is the iteration counter. Interestingly, with new parameter update rules, our algorithms can achieve $o(1/k)$ or $o(1/k^2)$ best-iterate convergence rate in expectation under either convexity or strong convexity, respectively. These rates can be obtained for both the primal and dual problems. To the best of our knowledge, this is the first time such faster convergence rates are shown for randomized primal-dual methods. Finally, we verify our theoretical results via two numerical examples and compare them with the state-of-the-art.

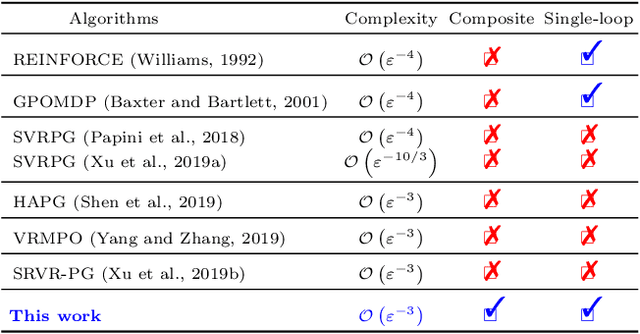

A Hybrid Stochastic Policy Gradient Algorithm for Reinforcement Learning

Mar 01, 2020

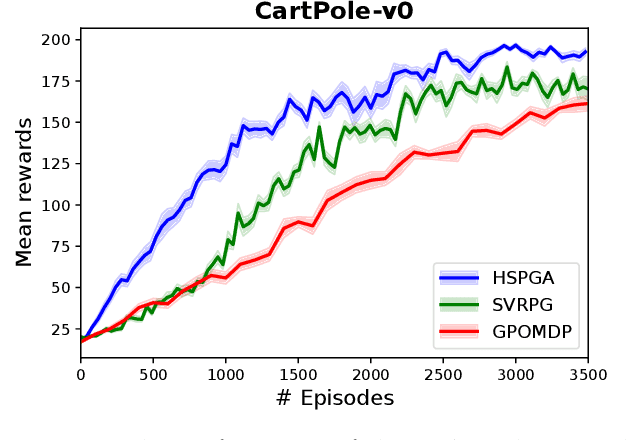

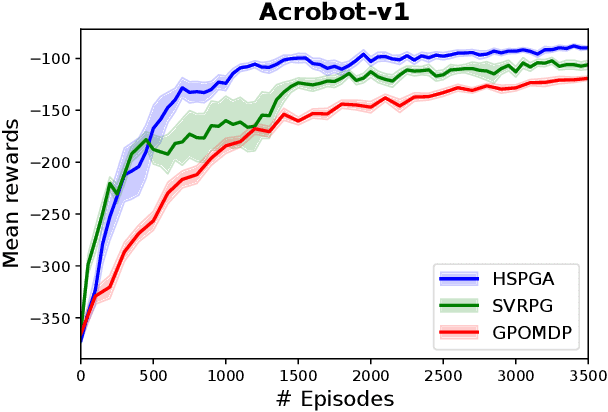

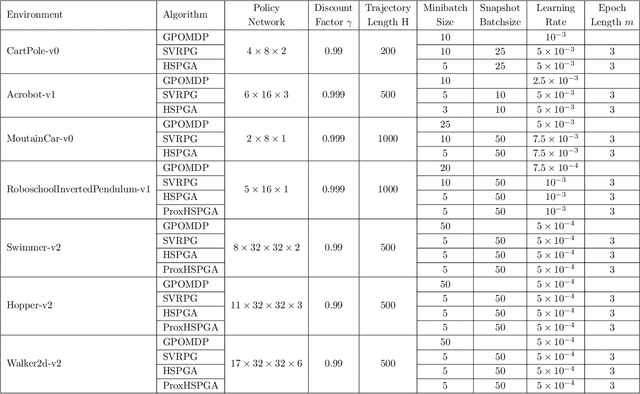

We propose a novel hybrid stochastic policy gradient estimator by combining an unbiased policy gradient estimator, the REINFORCE estimator, with another biased one, an adapted SARAH estimator for policy optimization. The hybrid policy gradient estimator is shown to be biased, but has variance reduced property. Using this estimator, we develop a new Proximal Hybrid Stochastic Policy Gradient Algorithm (ProxHSPGA) to solve a composite policy optimization problem that allows us to handle constraints or regularizers on the policy parameters. We first propose a single-looped algorithm then introduce a more practical restarting variant. We prove that both algorithms can achieve the best-known trajectory complexity $\mathcal{O}\left(\varepsilon^{-3}\right)$ to attain a first-order stationary point for the composite problem which is better than existing REINFORCE/GPOMDP $\mathcal{O}\left(\varepsilon^{-4}\right)$ and SVRPG $\mathcal{O}\left(\varepsilon^{-10/3}\right)$ in the non-composite setting. We evaluate the performance of our algorithm on several well-known examples in reinforcement learning. Numerical results show that our algorithm outperforms two existing methods on these examples. Moreover, the composite settings indeed have some advantages compared to the non-composite ones on certain problems.

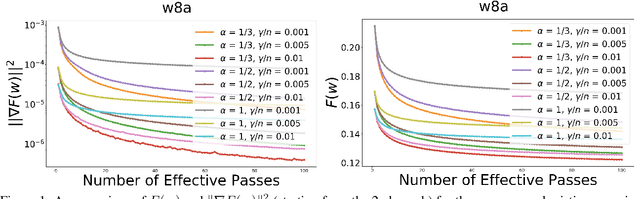

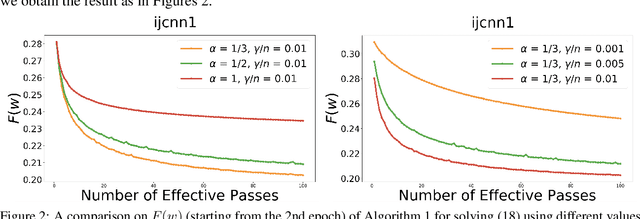

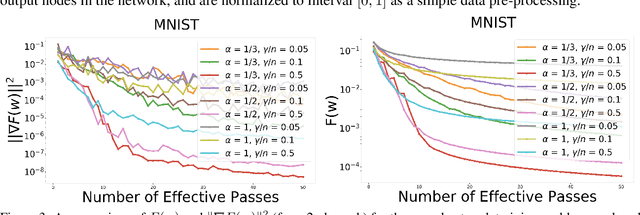

A Unified Convergence Analysis for Shuffling-Type Gradient Methods

Feb 19, 2020

In this paper, we provide a unified convergence analysis for a class of shuffling-type gradient methods for solving a well-known finite-sum minimization problem commonly used in machine learning. This algorithm covers various variants such as randomized reshuffling, single shuffling, and cyclic/incremental gradient schemes. We consider two different settings: strongly convex and non-convex problems. Our main contribution consists of new non-asymptotic and asymptotic convergence rates for a general class of shuffling-type gradient methods to solve both non-convex and strongly convex problems. While our rate in the non-convex problem is new (i.e. not known yet under standard assumptions), the rate on the strongly convex case matches (up to a constant) the best-known results. However, unlike existing works in this direction, we only use standard assumptions such as smoothness and strong convexity. Finally, we empirically illustrate the effect of learning rates via a non-convex logistic regression and neural network examples.

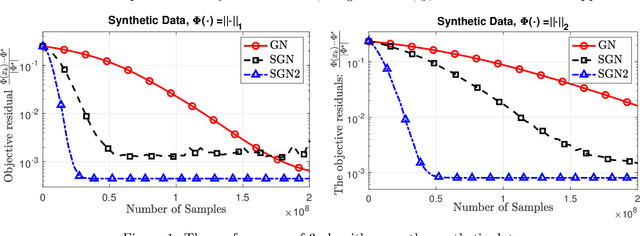

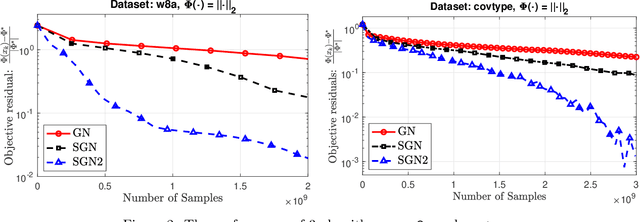

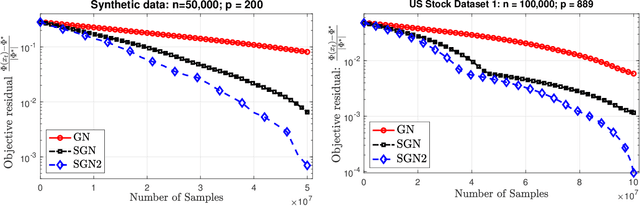

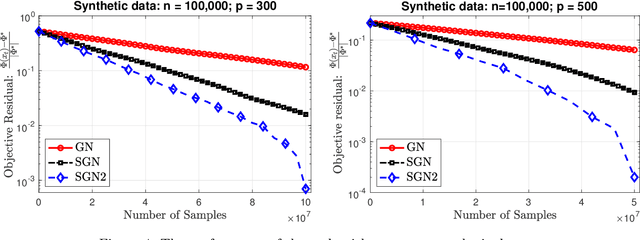

Stochastic Gauss-Newton Algorithms for Nonconvex Compositional Optimization

Feb 17, 2020

We develop two new stochastic Gauss-Newton algorithms for solving a class of stochastic nonconvex compositional optimization problems frequently arising in practice. We consider both the expectation and finite-sum settings under standard assumptions. We use both classical stochastic and SARAH estimators for approximating function values and Jacobians. In the expectation case, we establish $\mathcal{O}(\varepsilon^{-2})$ iteration complexity to achieve a stationary point in expectation and estimate the total number of stochastic oracle calls for both function values and its Jacobian, where $\varepsilon$ is a desired accuracy. In the finite sum case, we also estimate the same iteration complexity and the total oracle calls with high probability. To our best knowledge, this is the first time such global stochastic oracle complexity is established for stochastic Gauss-Newton methods. We illustrate our theoretical results via numerical examples on both synthetic and real datasets.

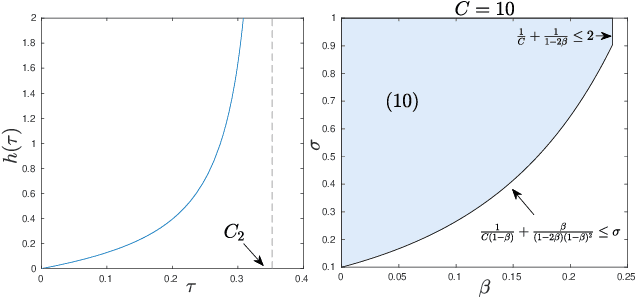

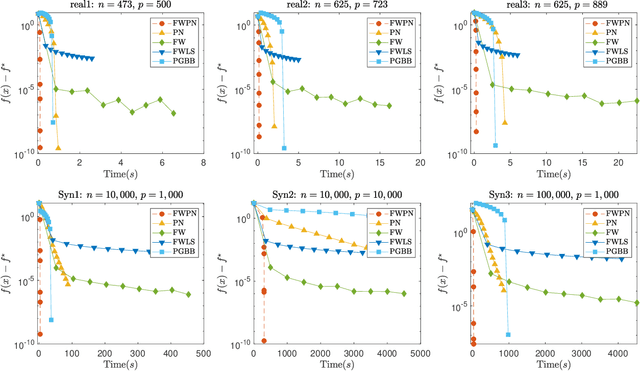

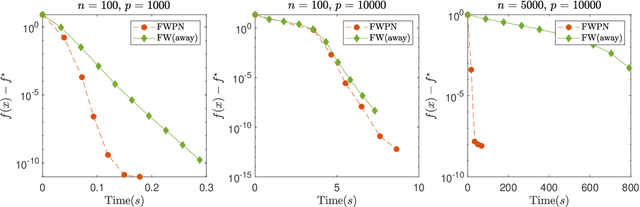

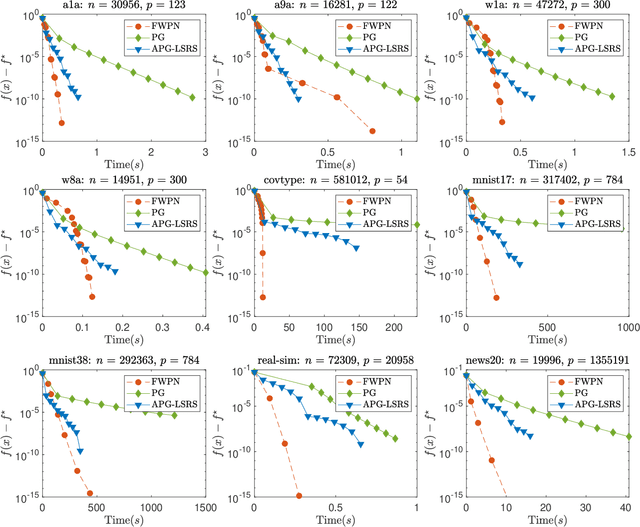

A Newton Frank-Wolfe Method for Constrained Self-Concordant Minimization

Feb 17, 2020

We demonstrate how to scalably solve a class of constrained self-concordant minimization problems using linear minimization oracles (LMO) over the constraint set. We prove that the number of LMO calls of our method is nearly the same as that of the Frank-Wolfe method in the L-smooth case. Specifically, our Newton Frank-Wolfe method uses $\mathcal{O}(\epsilon^{-\nu})$ LMO's, where $\epsilon$ is the desired accuracy and $\nu:= 1 + o(1)$. In addition, we demonstrate how our algorithm can exploit the improved variants of the LMO-based schemes, including away-steps, to attain linear convergence rates. We also provide numerical evidence with portfolio design with the competitive ratio, D-optimal experimental design, and logistic regression with the elastic net where Newton Frank-Wolfe outperforms the state-of-the-art.

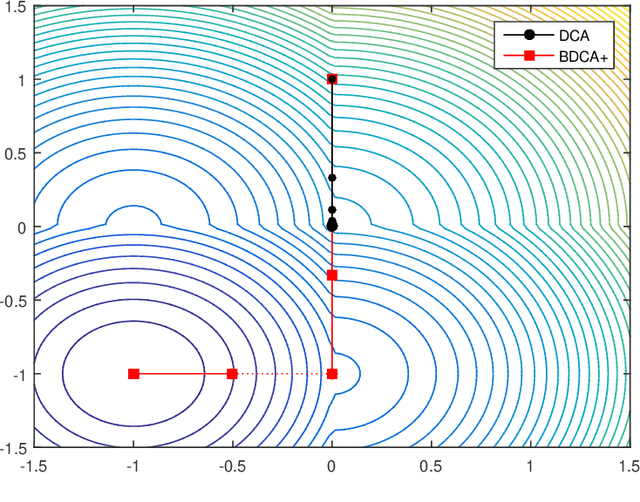

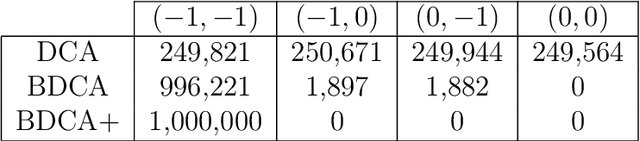

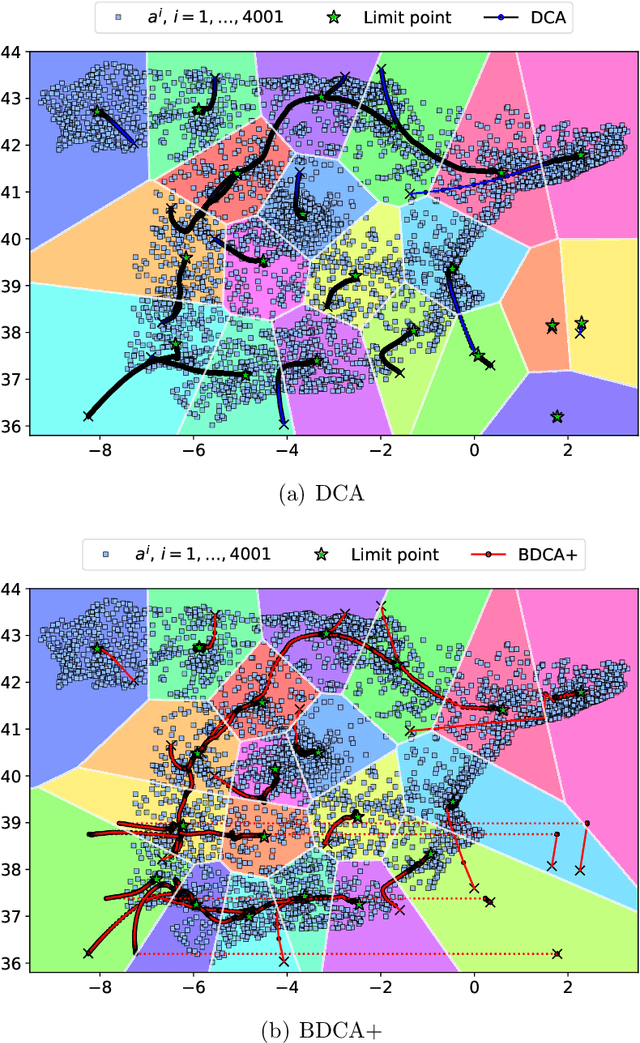

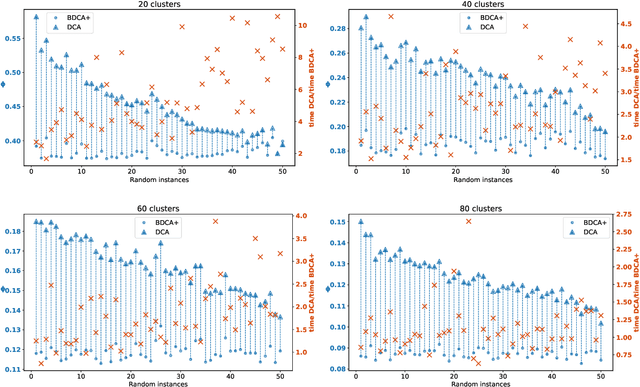

Using positive spanning sets to achieve stationarity with the Boosted DC Algorithm

Jul 26, 2019

The Difference of Convex function Algorithm (DCA) is widely used for minimizing the difference of two convex functions. A recently proposed accelerated version, termed BDCA for Boosted DC Algorithm, incorporates a line search step to achieve a larger decrease of the objective value at each iteration. Thanks to this step, BDCA usually converges much faster than DCA in practice. The solutions found by DCA are guaranteed to be critical points of the problem, but they are rarely local minima. Although BDCA tends to improve the objective value of the solutions it finds, these are frequently just critical points as well. In this paper we combine BDCA with a simple Derivative-Free Optimization (DFO) algorithm to force the stationarity (lack of descent direction) at the point obtained. The potential of this approach is illustrated through some computational experiments on a Minimum-Sum-of-Squares problem. Our numerical results demonstrate that the new method provides better solutions while still remains faster than DCA in the majority of test cases.

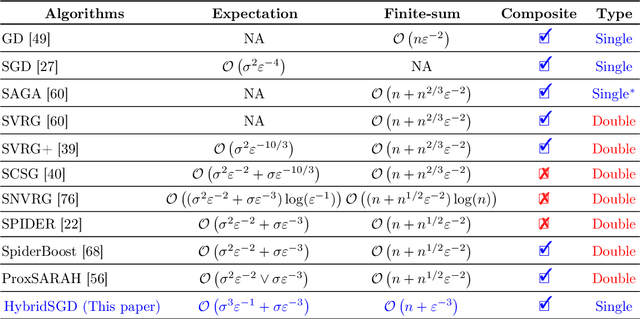

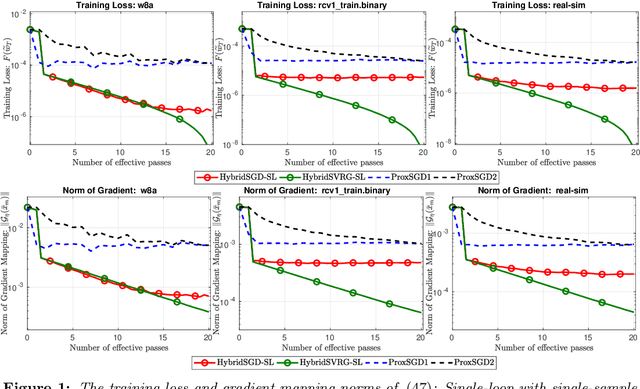

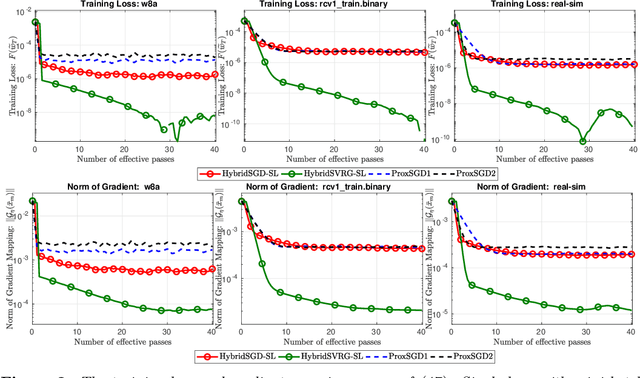

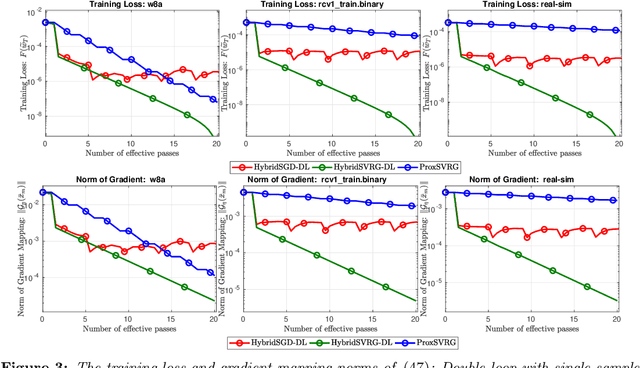

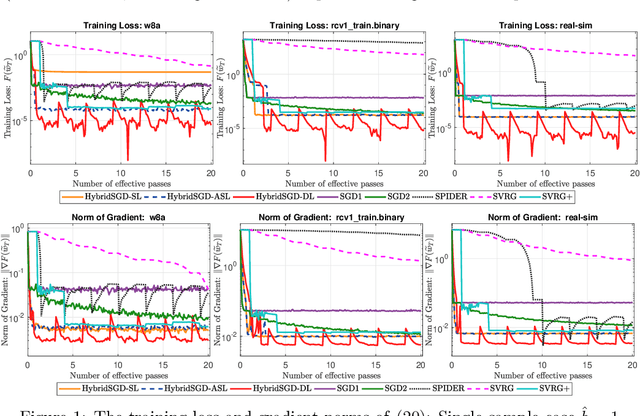

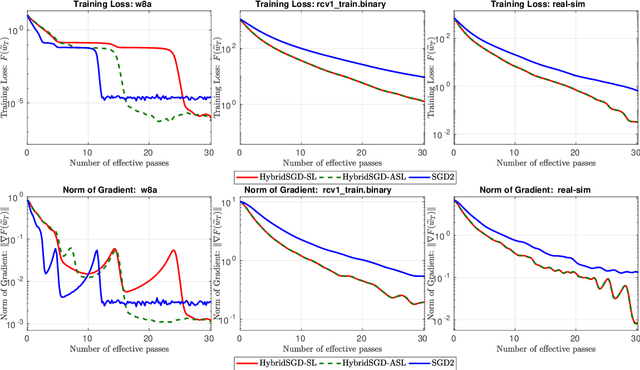

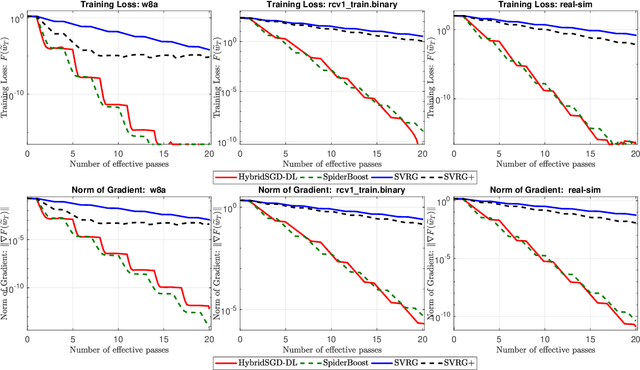

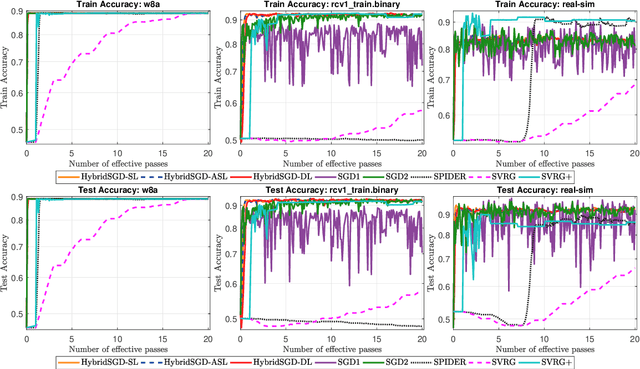

A Hybrid Stochastic Optimization Framework for Stochastic Composite Nonconvex Optimization

Jul 08, 2019

In this paper, we introduce a new approach to develop stochastic optimization algorithms for solving stochastic composite and possibly nonconvex optimization problems. The main idea is to combine two stochastic estimators to form a new hybrid one. We first introduce our hybrid estimator and then investigate its fundamental properties to form a foundation theory for algorithmic development. Next, we apply our theory to develop several variants of stochastic gradient methods to solve both expectation and finite-sum composite optimization problems. Our first algorithm can be viewed as a variant of proximal stochastic gradient methods with a single-loop, but can achieve $\mathcal{O}(\sigma^3\varepsilon^{-1} + \sigma\varepsilon^{-3})$ complexity bound that is significantly better than the $\mathcal{O}(\sigma^2\varepsilon^{-4})$-complexity in state-of-the-art stochastic gradient methods, where $\sigma$ is the variance and $\varepsilon$ is a desired accuracy. Then, we consider two different variants of our method: adaptive step-size and double-loop schemes that have the same theoretical guarantees as in our first algorithm. We also study two mini-batch variants and develop two hybrid SARAH-SVRG algorithms to solve the finite-sum problems. In all cases, we achieve the best-known complexity bounds under standard assumptions. We test our methods on several numerical examples with real datasets and compare them with state-of-the-arts. Our numerical experiments show that the new methods are comparable and, in many cases, outperform their competitors.

Hybrid Stochastic Gradient Descent Algorithms for Stochastic Nonconvex Optimization

May 15, 2019

We introduce a hybrid stochastic estimator to design stochastic gradient algorithms for solving stochastic optimization problems. Such a hybrid estimator is a convex combination of two existing biased and unbiased estimators and leads to some useful property on its variance. We limit our consideration to a hybrid SARAH-SGD for nonconvex expectation problems. However, our idea can be extended to handle a broader class of estimators in both convex and nonconvex settings. We propose a new single-loop stochastic gradient descent algorithm that can achieve $O(\max\{\sigma^3\varepsilon^{-1},\sigma\varepsilon^{-3}\})$-complexity bound to obtain an $\varepsilon$-stationary point under smoothness and $\sigma^2$-bounded variance assumptions. This complexity is better than $O(\sigma^2\varepsilon^{-4})$ often obtained in state-of-the-art SGDs when $\sigma < O(\varepsilon^{-3})$. We also consider different extensions of our method, including constant and adaptive step-size with single-loop, double-loop, and mini-batch variants. We compare our algorithms with existing methods on several datasets using two nonconvex models.

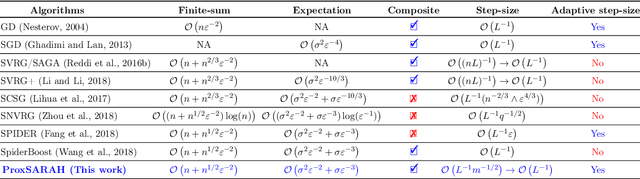

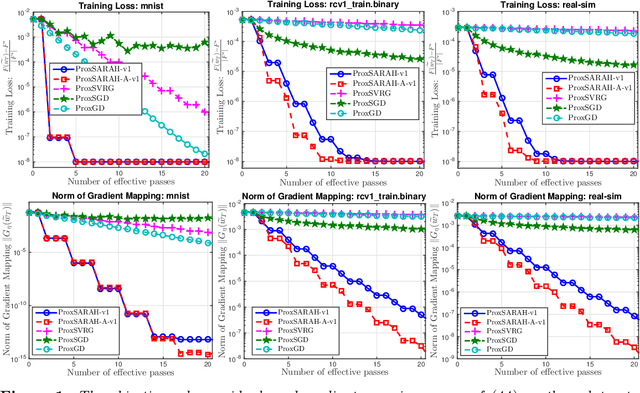

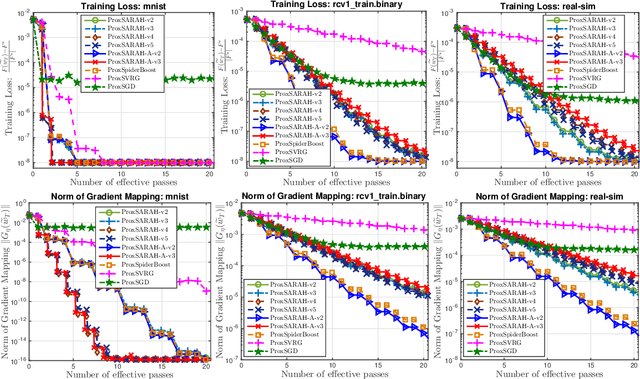

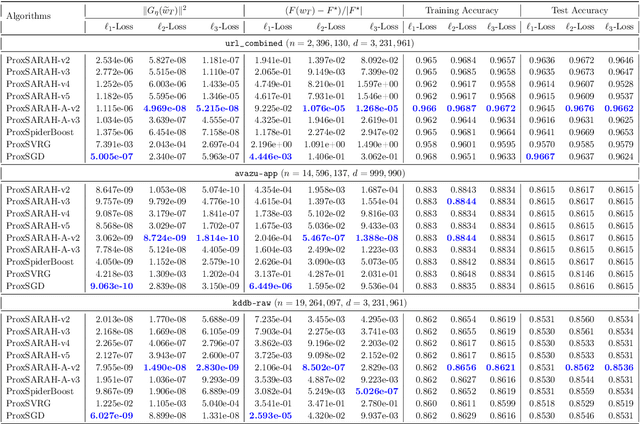

ProxSARAH: An Efficient Algorithmic Framework for Stochastic Composite Nonconvex Optimization

Mar 29, 2019

We propose a new stochastic first-order algorithmic framework to solve stochastic composite nonconvex optimization problems that covers both finite-sum and expectation settings. Our algorithms rely on the SARAH estimator introduced in (Nguyen et al, 2017) and consist of two steps: a proximal gradient and an averaging step making them different from existing nonconvex proximal-type algorithms. The algorithms only require an average smoothness assumption of the nonconvex objective term and additional bounded variance assumption if applied to expectation problems. They work with both constant and adaptive step-sizes, while allowing single sample and mini-batches. In all these cases, we prove that our algorithms can achieve the best-known complexity bounds. One key step of our methods is new constant and adaptive step-sizes that help to achieve desired complexity bounds while improving practical performance. Our constant step-size is much larger than existing methods including proximal SVRG schemes in the single sample case. We also specify the algorithm to the non-composite case that covers existing state-of-the-arts in terms of complexity bounds. Our update also allows one to trade-off between step-sizes and mini-batch sizes to improve performance. We test the proposed algorithms on two composite nonconvex problems and neural networks using several well-known datasets.

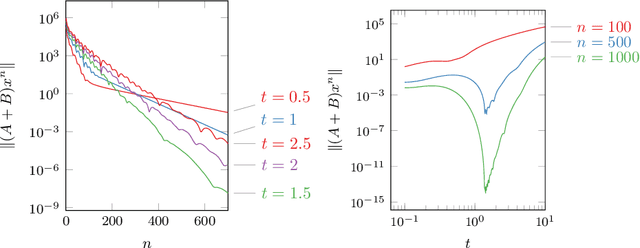

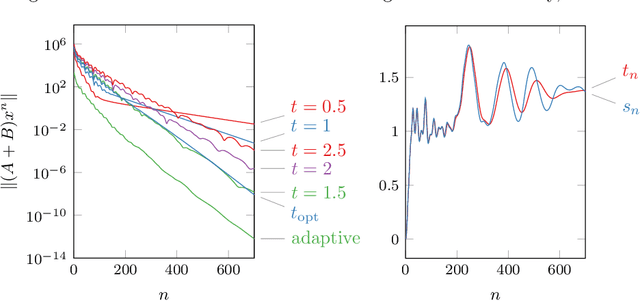

Non-stationary Douglas-Rachford and alternating direction method of multipliers: adaptive stepsizes and convergence

Sep 27, 2018

We revisit the classical Douglas-Rachford (DR) method for finding a zero of the sum of two maximal monotone operators. Since the practical performance of the DR method crucially depends on the stepsizes, we aim at developing an adaptive stepsize rule. To that end, we take a closer look at a linear case of the problem and use our findings to develop a stepsize strategy that eliminates the need for stepsize tuning. We analyze a general non-stationary DR scheme and prove its convergence for a convergent sequence of stepsizes with summable increments. This, in turn, proves the convergence of the method with the new adaptive stepsize rule. We also derive the related non-stationary alternating direction method of multipliers (ADMM) from such a non-stationary DR method. We illustrate the efficiency of the proposed methods on several numerical examples.