Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeInterpretable Distribution Features with Maximum Testing Power

Oct 28, 2016

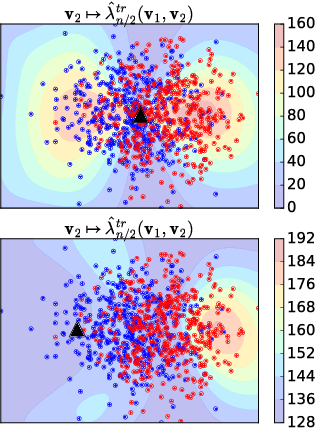

Two semimetrics on probability distributions are proposed, given as the sum of differences of expectations of analytic functions evaluated at spatial or frequency locations (i.e, features). The features are chosen so as to maximize the distinguishability of the distributions, by optimizing a lower bound on test power for a statistical test using these features. The result is a parsimonious and interpretable indication of how and where two distributions differ locally. An empirical estimate of the test power criterion converges with increasing sample size, ensuring the quality of the returned features. In real-world benchmarks on high-dimensional text and image data, linear-time tests using the proposed semimetrics achieve comparable performance to the state-of-the-art quadratic-time maximum mean discrepancy test, while returning human-interpretable features that explain the test results.

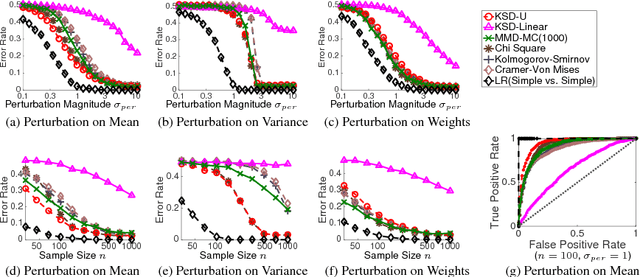

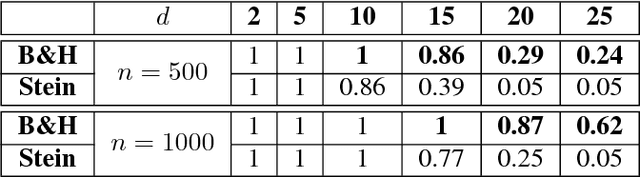

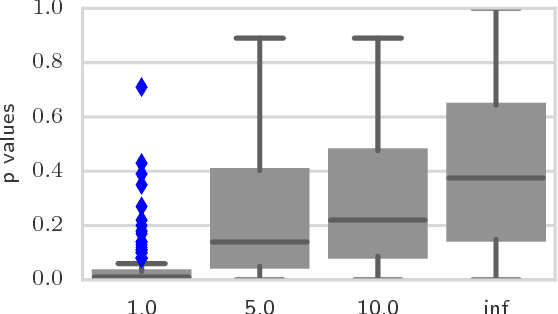

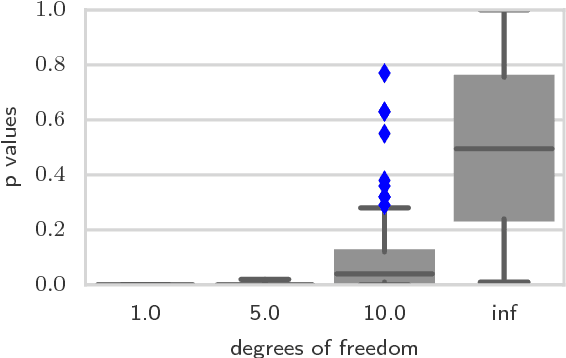

A Kernel Test of Goodness of Fit

Sep 27, 2016

We propose a nonparametric statistical test for goodness-of-fit: given a set of samples, the test determines how likely it is that these were generated from a target density function. The measure of goodness-of-fit is a divergence constructed via Stein's method using functions from a Reproducing Kernel Hilbert Space. Our test statistic is based on an empirical estimate of this divergence, taking the form of a V-statistic in terms of the log gradients of the target density and the kernel. We derive a statistical test, both for i.i.d. and non-i.i.d. samples, where we estimate the null distribution quantiles using a wild bootstrap procedure. We apply our test to quantifying convergence of approximate Markov Chain Monte Carlo methods, statistical model criticism, and evaluating quality of fit vs model complexity in nonparametric density estimation.

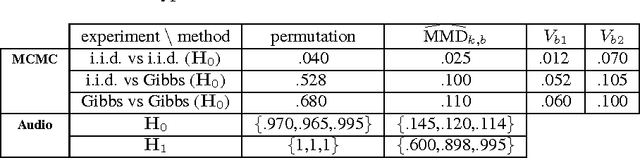

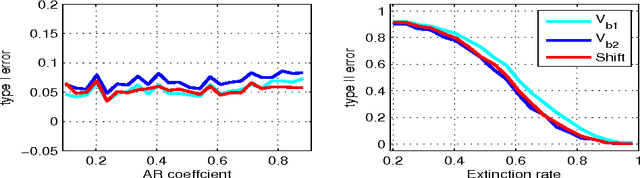

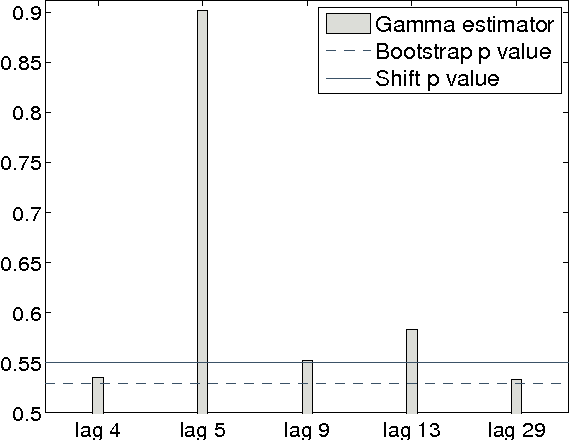

A Wild Bootstrap for Degenerate Kernel Tests

Sep 27, 2016

A wild bootstrap method for nonparametric hypothesis tests based on kernel distribution embeddings is proposed. This bootstrap method is used to construct provably consistent tests that apply to random processes, for which the naive permutation-based bootstrap fails. It applies to a large group of kernel tests based on V-statistics, which are degenerate under the null hypothesis, and non-degenerate elsewhere. To illustrate this approach, we construct a two-sample test, an instantaneous independence test and a multiple lag independence test for time series. In experiments, the wild bootstrap gives strong performance on synthetic examples, on audio data, and in performance benchmarking for the Gibbs sampler.

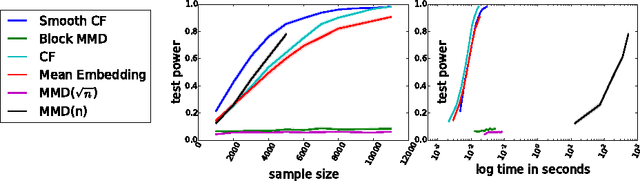

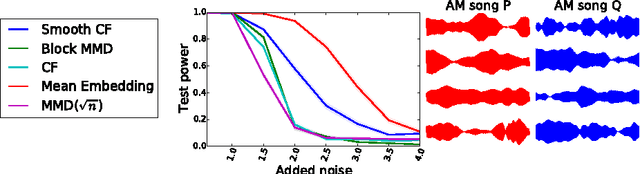

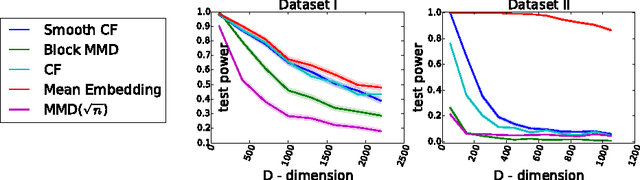

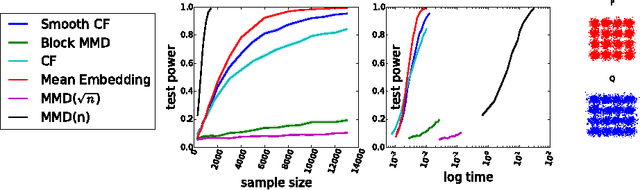

Fast Two-Sample Testing with Analytic Representations of Probability Measures

Jun 15, 2015

We propose a class of nonparametric two-sample tests with a cost linear in the sample size. Two tests are given, both based on an ensemble of distances between analytic functions representing each of the distributions. The first test uses smoothed empirical characteristic functions to represent the distributions, the second uses distribution embeddings in a reproducing kernel Hilbert space. Analyticity implies that differences in the distributions may be detected almost surely at a finite number of randomly chosen locations/frequencies. The new tests are consistent against a larger class of alternatives than the previous linear-time tests based on the (non-smoothed) empirical characteristic functions, while being much faster than the current state-of-the-art quadratic-time kernel-based or energy distance-based tests. Experiments on artificial benchmarks and on challenging real-world testing problems demonstrate that our tests give a better power/time tradeoff than competing approaches, and in some cases, better outright power than even the most expensive quadratic-time tests. This performance advantage is retained even in high dimensions, and in cases where the difference in distributions is not observable with low order statistics.

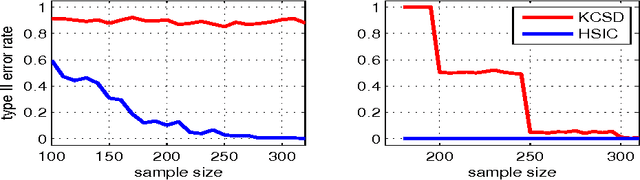

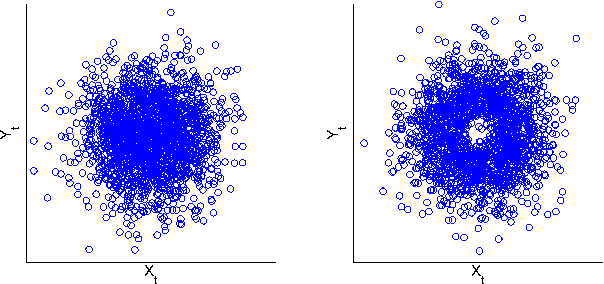

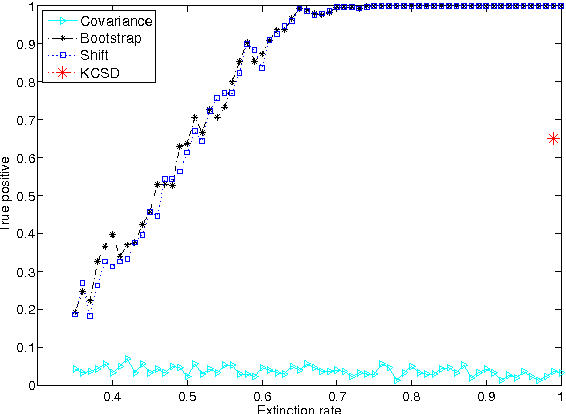

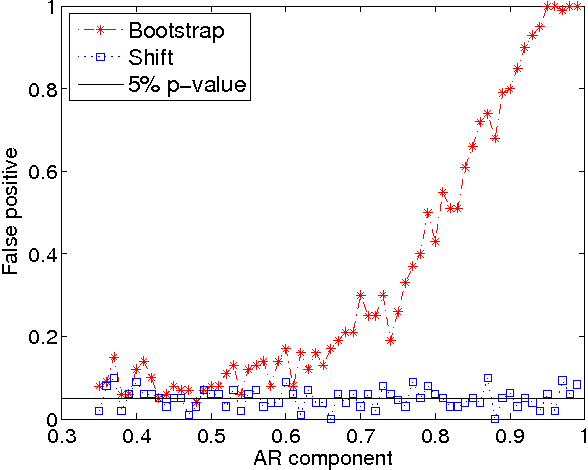

A Kernel Independence Test for Random Processes

Jun 17, 2014

A new non parametric approach to the problem of testing the independence of two random process is developed. The test statistic is the Hilbert Schmidt Independence Criterion (HSIC), which was used previously in testing independence for i.i.d pairs of variables. The asymptotic behaviour of HSIC is established when computed from samples drawn from random processes. It is shown that earlier bootstrap procedures which worked in the i.i.d. case will fail for random processes, and an alternative consistent estimate of the p-values is proposed. Tests on artificial data and real-world Forex data indicate that the new test procedure discovers dependence which is missed by linear approaches, while the earlier bootstrap procedure returns an elevated number of false positives. The code is available online: https://github.com/kacperChwialkowski/HSIC .