Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeAdaptive Reduced Rank Regression

May 28, 2019

Low rank regression has proven to be useful in a wide range of forecasting problems. However, in settings with a low signal-to-noise ratio, it is known to suffer from severe overfitting. This paper studies the reduced rank regression problem and presents algorithms with provable generalization guarantees. We use adaptive hard rank-thresholding in two different parts of the data analysis pipeline. First, we consider a low rank projection of the data to eliminate the components that are most likely to be noisy. Second, we perform a standard multivariate linear regression estimator on the data obtained in the first step, and subsequently consider a low-rank projection of the obtained regression matrix. Both thresholding is performed in a data-driven manner and is required to prevent severe overfitting as our lower bounds show. Experimental results show that our approach either outperforms or is competitive with existing baselines.

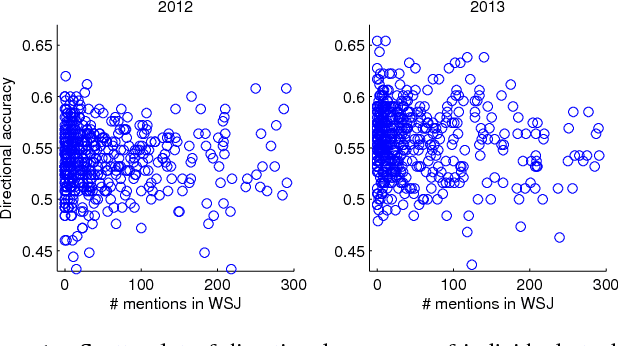

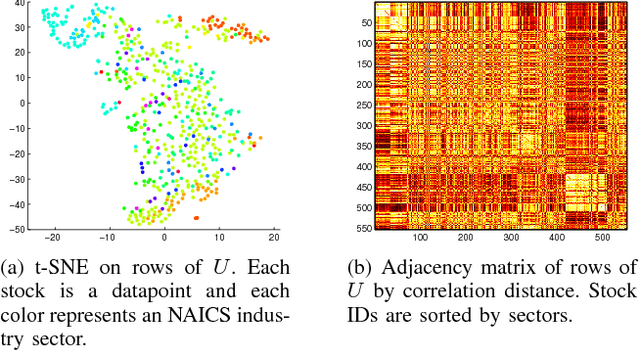

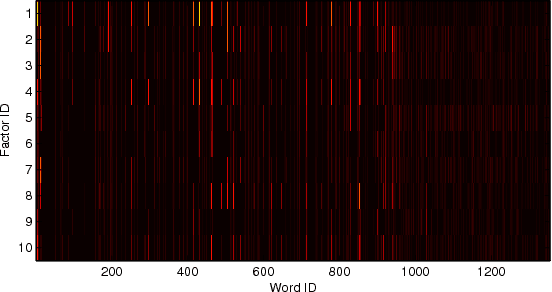

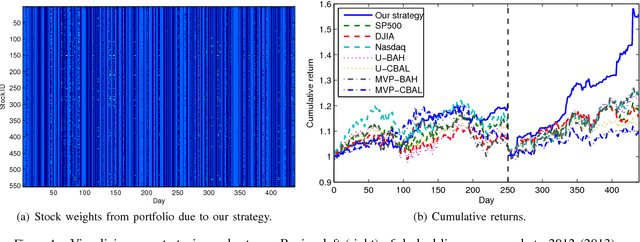

Stock Market Prediction from WSJ: Text Mining via Sparse Matrix Factorization

Jun 27, 2014

We revisit the problem of predicting directional movements of stock prices based on news articles: here our algorithm uses daily articles from The Wall Street Journal to predict the closing stock prices on the same day. We propose a unified latent space model to characterize the "co-movements" between stock prices and news articles. Unlike many existing approaches, our new model is able to simultaneously leverage the correlations: (a) among stock prices, (b) among news articles, and (c) between stock prices and news articles. Thus, our model is able to make daily predictions on more than 500 stocks (most of which are not even mentioned in any news article) while having low complexity. We carry out extensive backtesting on trading strategies based on our algorithm. The result shows that our model has substantially better accuracy rate (55.7%) compared to many widely used algorithms. The return (56%) and Sharpe ratio due to a trading strategy based on our model are also much higher than baseline indices.