Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeConditional Versus Adversarial Euler-based Generators For Time Series

Paper and Code

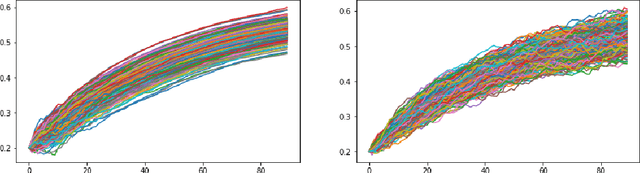

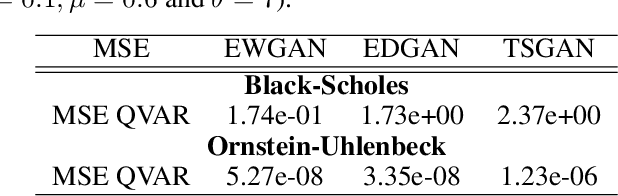

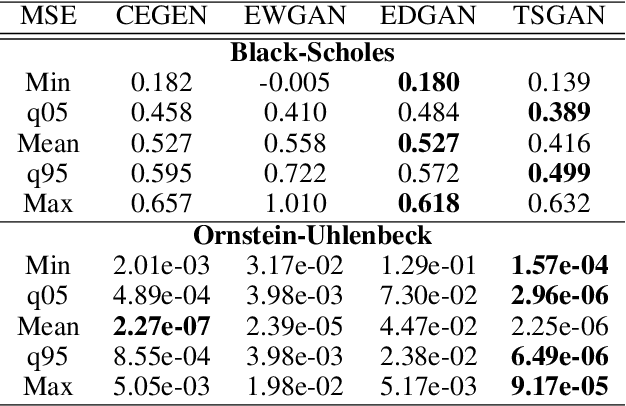

We introduce new generative models for time series based on Euler discretization that do not require any pre-stationarization procedure. Specifically, we develop two GAN based methods, relying on the adaptation of Wasserstein GANs (Arjovsky et al., 2017) and DVD GANs (Clark et al., 2019b) to time series. Alternatively, we consider a conditional Euler Generator (CEGEN) minimizing a distance between the induced conditional densities. In the context of It\^o processes, we theoretically validate this approach and demonstrate using the Bures metric that reaching a low loss level provides accurate estimations for both the drift and the volatility terms of the underlying process. Tests on simple models show how the Euler discretization and the use of Wasserstein distance allow the proposed GANs and (more considerably) CEGEN to outperform state-of-the-art Time Series GAN generation( Yoon et al., 2019b) on time structure metrics. In higher dimensions we observe that CEGEN manages to get the correct covariance structures. Finally we illustrate how our model can be combined to a Monte Carlo simulator in a low data context by using a transfer learning technique