Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeUncertainty Quantification for Demand Prediction in Contextual Dynamic Pricing

Paper and Code

Mar 16, 2020

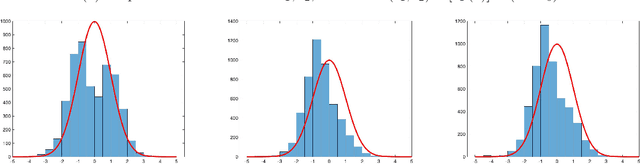

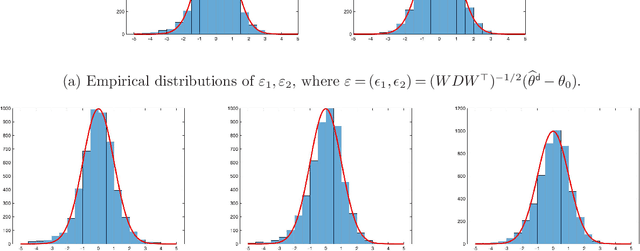

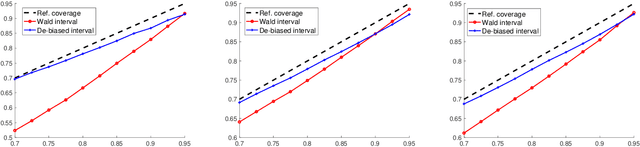

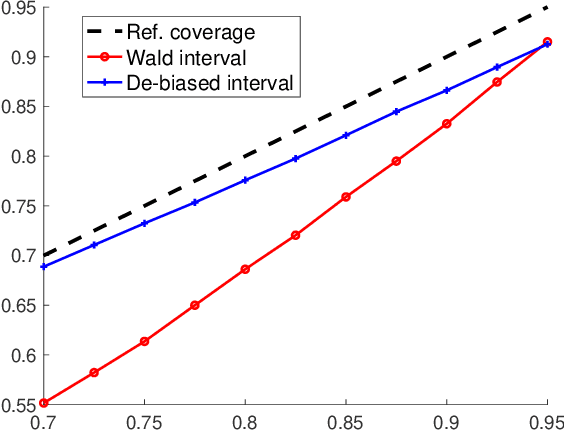

Data-driven sequential decision has found a wide range of applications in modern operations management, such as dynamic pricing, inventory control, and assortment optimization. Most existing research on data-driven sequential decision focuses on designing an online policy to maximize the revenue. However, the research on uncertainty quantification on the underlying true model function (e.g., demand function), a critical problem for practitioners, has not been well explored. In this paper, using the problem of demand function prediction in dynamic pricing as the motivating example, we study the problem of constructing accurate confidence intervals for the demand function. The main challenge is that sequentially collected data leads to significant distributional bias in the maximum likelihood estimator or the empirical risk minimization estimate, making classical statistics approaches such as the Wald's test no longer valid. We address this challenge by developing a debiased approach and provide the asymptotic normality guarantee of the debiased estimator. Based this the debiased estimator, we provide both point-wise and uniform confidence intervals of the demand function.