Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeA parallel-network continuous quantitative trading model with GARCH and PPO

May 21, 2021

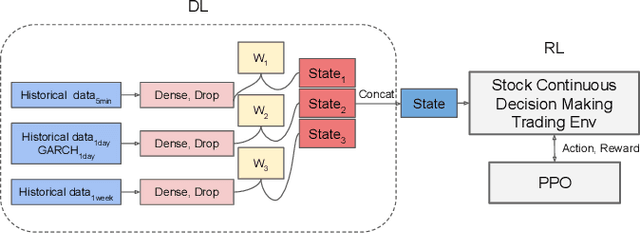

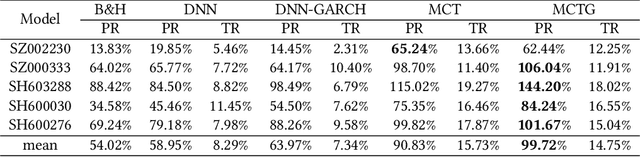

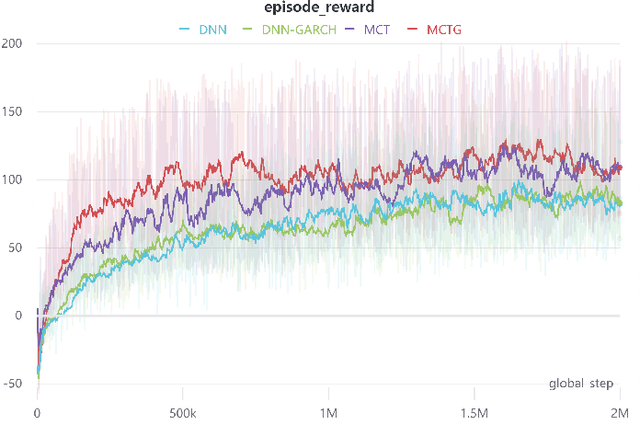

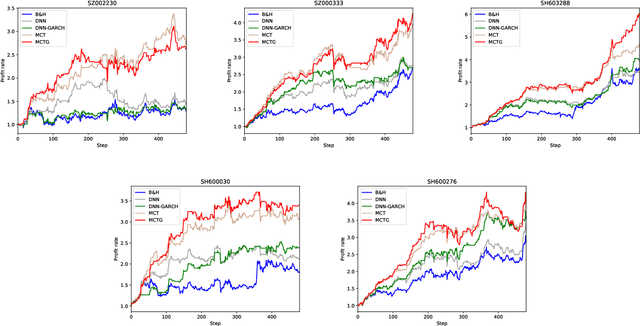

It is a difficult task for both professional investors and individual traders continuously making profit in stock market. With the development of computer science and deep reinforcement learning, Buy\&Hold (B\&H) has been oversteped by many artificial intelligence trading algorithms. However, the information and process are not enough, which limit the performance of reinforcement learning algorithms. Thus, we propose a parallel-network continuous quantitative trading model with GARCH and PPO to enrich the basical deep reinforcement learning model, where the deep learning parallel network layers deal with 3 different frequencies data (including GARCH information) and proximal policy optimization (PPO) algorithm interacts actions and rewards with stock trading environment. Experiments in 5 stocks from Chinese stock market show our method achieves more extra profit comparing with basical reinforcement learning methods and bench models.