Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to Edge100x Cost & Latency Reduction: Performance Analysis of AI Query Approximation using Lightweight Proxy Models

Mar 16, 2026Several data warehouse and database providers have recently introduced extensions to SQL called AI Queries, enabling users to specify functions and conditions in SQL that are evaluated by LLMs, thereby broadening significantly the kinds of queries one can express over the combination of structured and unstructured data. LLMs offer remarkable semantic reasoning capabilities, making them an essential tool for complex and nuanced queries that blend structured and unstructured data. While extremely powerful, these AI queries can become prohibitively costly when invoked thousands of times. This paper provides an extensive evaluation of a recent AI query approximation approach that enables low cost analytics and database applications to benefit from AI queries. The approach delivers >100x cost and latency reduction for the semantic filter (AI.IF) operator and also important gains for semantic ranking (AI.RANK). The cost and performance gains come from utilizing cheap and accurate proxy models over embedding vectors. We show that despite the massive gains in latency and cost, these proxy models preserve accuracy and occasionally improve accuracy across various benchmark datasets, including the extended Amazon reviews benchmark that has 10M rows. We present an OLAP-friendly architecture within Google \textit{BigQuery} for this approach for purely online (ad hoc) queries, and a low-latency HTAP database-friendly architecture in \textit{AlloyDB} that could further improve the latency by moving the proxy model training offline. We present techniques that accelerate the proxy model training.

LeanML: A Design Pattern To Slash Avoidable Wastes in Machine Learning Projects

Aug 12, 2021

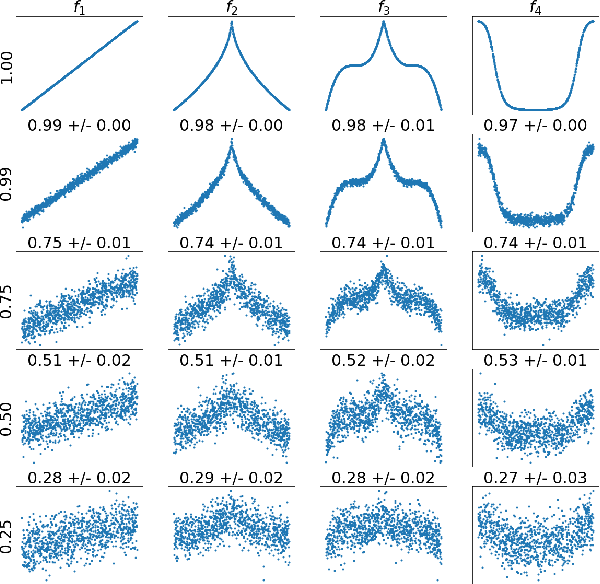

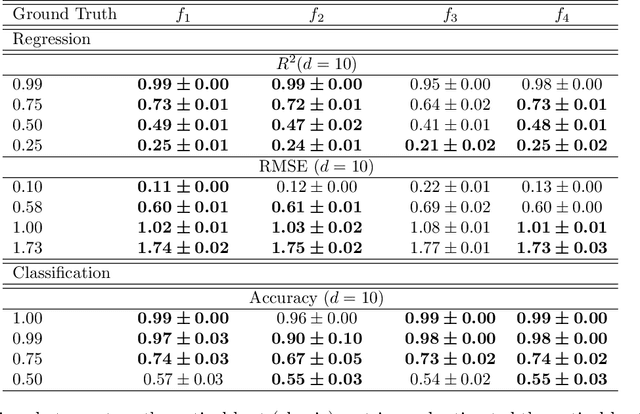

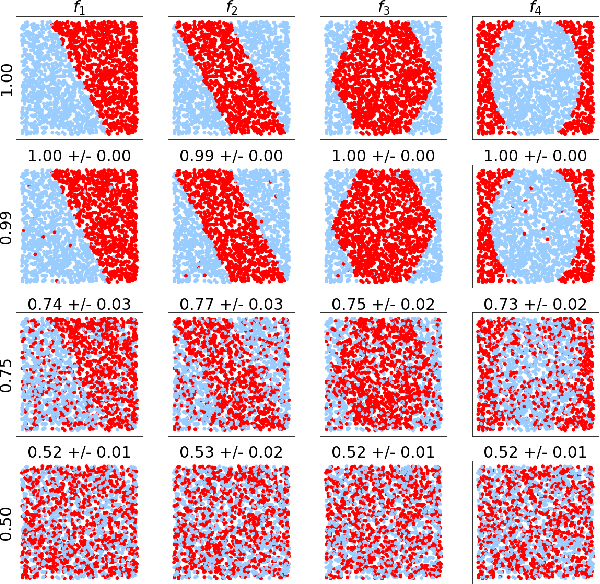

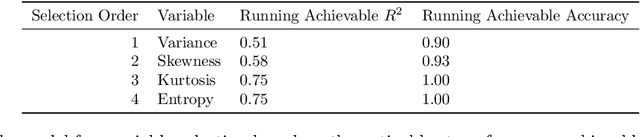

We introduce the first application of the lean methodology to machine learning projects. Similar to lean startups and lean manufacturing, we argue that lean machine learning (LeanML) can drastically slash avoidable wastes in commercial machine learning projects, reduce the business risk in investing in machine learning capabilities and, in so doing, further democratize access to machine learning. The lean design pattern we propose in this paper is based on two realizations. First, it is possible to estimate the best performance one may achieve when predicting an outcome $y \in \mathcal{Y}$ using a given set of explanatory variables $x \in \mathcal{X}$, for a wide range of performance metrics, and without training any predictive model. Second, doing so is considerably easier, faster, and cheaper than learning the best predictive model. We derive formulae expressing the best $R^2$, MSE, classification accuracy, and log-likelihood per observation achievable when using $x$ to predict $y$ as a function of the mutual information $I\left(y; x\right)$, and possibly a measure of the variability of $y$ (e.g. its Shannon entropy in the case of classification accuracy, and its variance in the case regression MSE). We illustrate the efficacy of the LeanML design pattern on a wide range of regression and classification problems, synthetic and real-life.

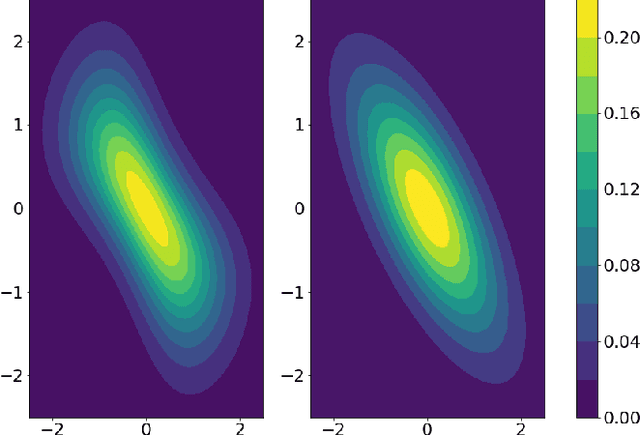

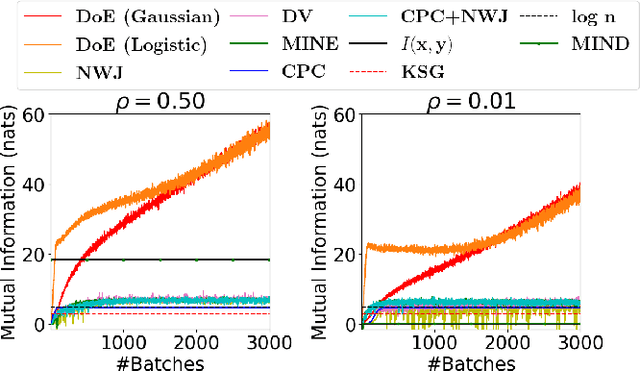

Inductive Mutual Information Estimation: A Convex Maximum-Entropy Copula Approach

Feb 25, 2021

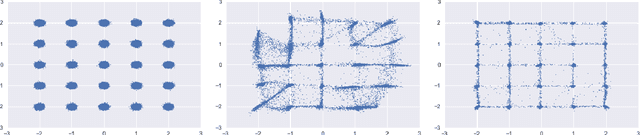

We propose a novel estimator of the mutual information between two ordinal vectors $x$ and $y$. Our approach is inductive (as opposed to deductive) in that it depends on the data generating distribution solely through some nonparametric properties revealing associations in the data, and does not require having enough data to fully characterize the true joint distributions $P_{x, y}$. Specifically, our approach consists of (i) noting that $I\left(y; x\right) = I\left(u_y; u_x\right)$ where $u_y$ and $u_x$ are the \emph{copula-uniform dual representations} of $y$ and $x$ (i.e. their images under the probability integral transform), and (ii) estimating the copula entropies $h\left(u_y\right)$, $h\left(u_x\right)$ and $h\left(u_y, u_x\right)$ by solving a maximum-entropy problem over the space of copula densities under a constraint of the type $\alpha_m = E\left[\phi_m(u_y, u_x)\right]$. We prove that, so long as the constraint is feasible, this problem admits a unique solution, it is in the exponential family, and it can be learned by solving a convex optimization problem. The resulting estimator, which we denote MIND, is marginal-invariant, always non-negative, unbounded for any sample size $n$, consistent, has MSE rate $O(1/n)$, and is more data-efficient than competing approaches. Beyond mutual information estimation, we illustrate that our approach may be used to mitigate mode collapse in GANs by maximizing the entropy of the copula of fake samples, a model we refer to as Copula Entropy Regularized GAN (CER-GAN).

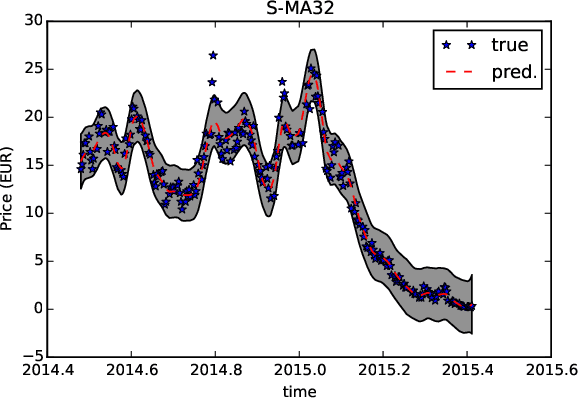

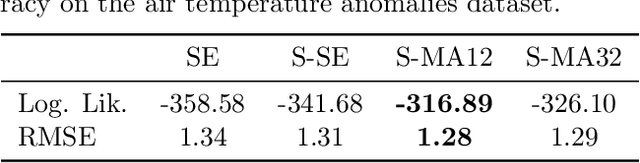

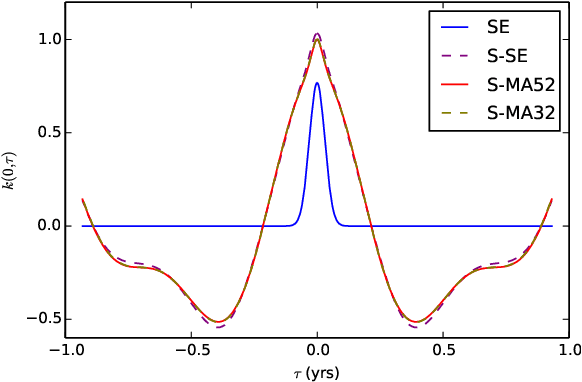

String and Membrane Gaussian Processes

Aug 19, 2016

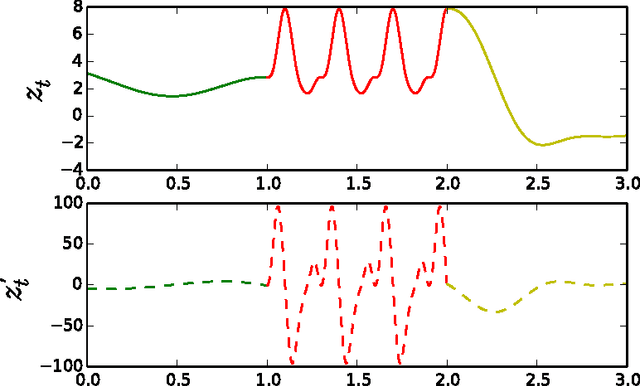

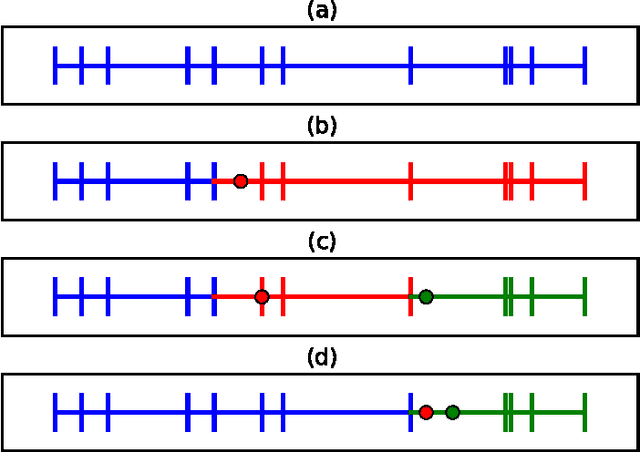

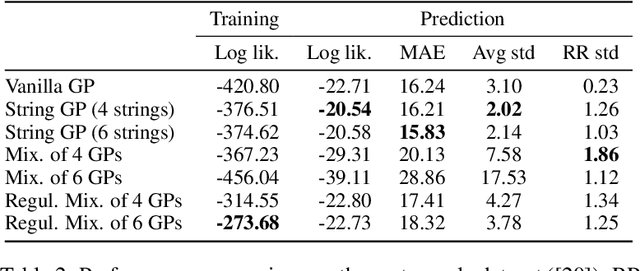

In this paper we introduce a novel framework for making exact nonparametric Bayesian inference on latent functions, that is particularly suitable for Big Data tasks. Firstly, we introduce a class of stochastic processes we refer to as string Gaussian processes (string GPs), which are not to be mistaken for Gaussian processes operating on text. We construct string GPs so that their finite-dimensional marginals exhibit suitable local conditional independence structures, which allow for scalable, distributed, and flexible nonparametric Bayesian inference, without resorting to approximations, and while ensuring some mild global regularity constraints. Furthermore, string GP priors naturally cope with heterogeneous input data, and the gradient of the learned latent function is readily available for explanatory analysis. Secondly, we provide some theoretical results relating our approach to the standard GP paradigm. In particular, we prove that some string GPs are Gaussian processes, which provides a complementary global perspective on our framework. Finally, we derive a scalable and distributed MCMC scheme for supervised learning tasks under string GP priors. The proposed MCMC scheme has computational time complexity $\mathcal{O}(N)$ and memory requirement $\mathcal{O}(dN)$, where $N$ is the data size and $d$ the dimension of the input space. We illustrate the efficacy of the proposed approach on several synthetic and real-world datasets, including a dataset with $6$ millions input points and $8$ attributes.

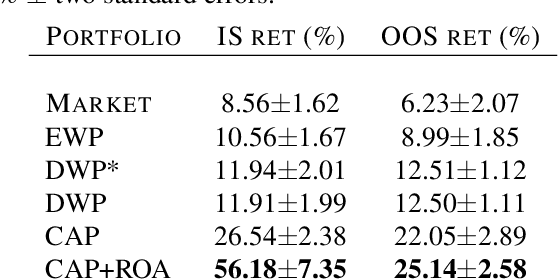

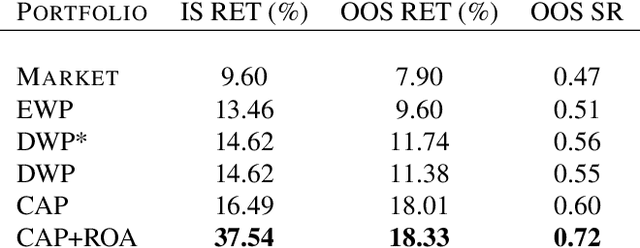

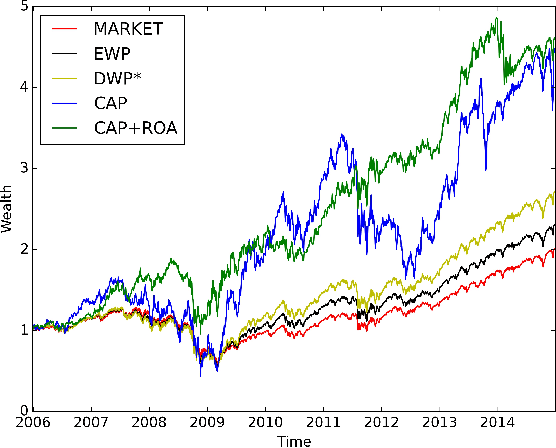

Stochastic Portfolio Theory: A Machine Learning Perspective

May 09, 2016

In this paper we propose a novel application of Gaussian processes (GPs) to financial asset allocation. Our approach is deeply rooted in Stochastic Portfolio Theory (SPT), a stochastic analysis framework introduced by Robert Fernholz that aims at flexibly analysing the performance of certain investment strategies in stock markets relative to benchmark indices. In particular, SPT has exhibited some investment strategies based on company sizes that, under realistic assumptions, outperform benchmark indices with probability 1 over certain time horizons. Galvanised by this result, we consider the inverse problem that consists of learning (from historical data) an optimal investment strategy based on any given set of trading characteristics, and using a user-specified optimality criterion that may go beyond outperforming a benchmark index. Although this inverse problem is of the utmost interest to investment management practitioners, it can hardly be tackled using the SPT framework. We show that our machine learning approach learns investment strategies that considerably outperform existing SPT strategies in the US stock market.

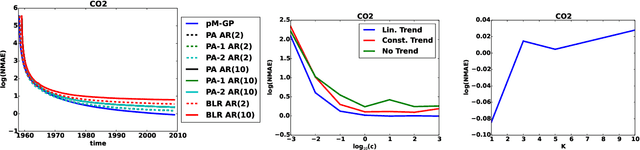

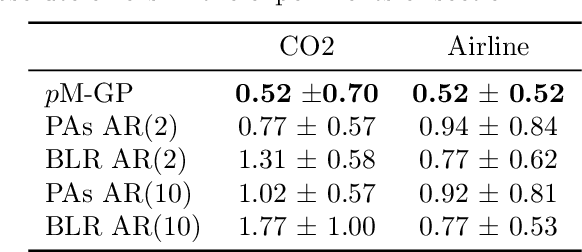

p-Markov Gaussian Processes for Scalable and Expressive Online Bayesian Nonparametric Time Series Forecasting

Oct 09, 2015

In this paper we introduce a novel online time series forecasting model we refer to as the pM-GP filter. We show that our model is equivalent to Gaussian process regression, with the advantage that both online forecasting and online learning of the hyper-parameters have a constant (rather than cubic) time complexity and a constant (rather than squared) memory requirement in the number of observations, without resorting to approximations. Moreover, the proposed model is expressive in that the family of covariance functions of the implied latent process, namely the spectral Matern kernels, have recently been proven to be capable of approximating arbitrarily well any translation-invariant covariance function. The benefit of our approach compared to competing models is demonstrated using experiments on several real-life datasets.

Generalized Spectral Kernels

Oct 09, 2015

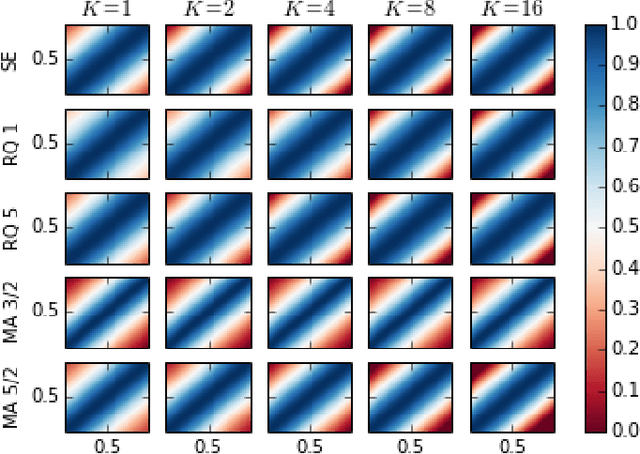

In this paper we propose a family of tractable kernels that is dense in the family of bounded positive semi-definite functions (i.e. can approximate any bounded kernel with arbitrary precision). We start by discussing the case of stationary kernels, and propose a family of spectral kernels that extends existing approaches such as spectral mixture kernels and sparse spectrum kernels. Our extension has two primary advantages. Firstly, unlike existing spectral approaches that yield infinite differentiability, the kernels we introduce allow learning the degree of differentiability of the latent function in Gaussian process (GP) models and functions in the reproducing kernel Hilbert space (RKHS) in other kernel methods. Secondly, we show that some of the kernels we propose require fewer parameters than existing spectral kernels for the same accuracy, thereby leading to faster and more robust inference. Finally, we generalize our approach and propose a flexible and tractable family of spectral kernels that we prove can approximate any continuous bounded nonstationary kernel.

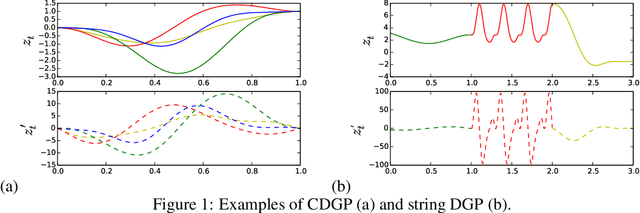

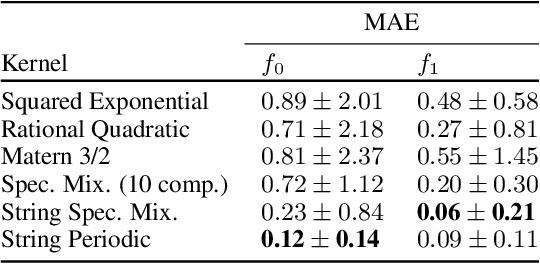

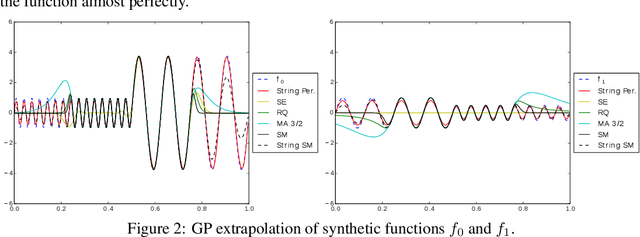

String Gaussian Process Kernels

Jun 07, 2015

We introduce a new class of nonstationary kernels, which we derive as covariance functions of a novel family of stochastic processes we refer to as string Gaussian processes (string GPs). We construct string GPs to allow for multiple types of local patterns in the data, while ensuring a mild global regularity condition. In this paper, we illustrate the efficacy of the approach using synthetic data and demonstrate that the model outperforms competing approaches on well studied, real-life datasets that exhibit nonstationary features.

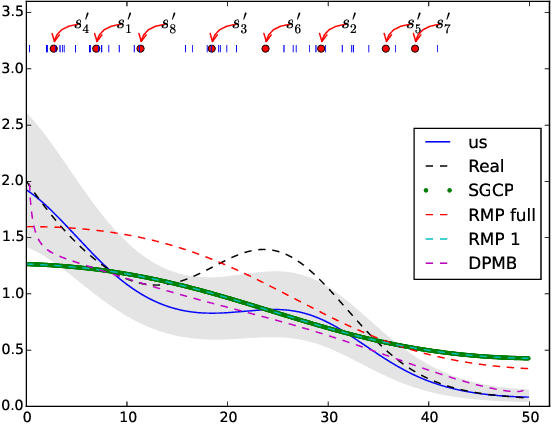

Scalable Nonparametric Bayesian Inference on Point Processes with Gaussian Processes

May 09, 2015

In this paper we propose the first non-parametric Bayesian model using Gaussian Processes to make inference on Poisson Point Processes without resorting to gridding the domain or to introducing latent thinning points. Unlike competing models that scale cubically and have a squared memory requirement in the number of data points, our model has a linear complexity and memory requirement. We propose an MCMC sampler and show that our model is faster, more accurate and generates less correlated samples than competing models on both synthetic and real-life data. Finally, we show that our model easily handles data sizes not considered thus far by alternate approaches.

* To appear at the International Conference on Machine Learning (ICML), 2015