Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeCHERRY: Compressed Hierarchical Experts with Recurrent Representational Yield

Jun 30, 2026We study three complementary techniques for training compute-efficient language models. (1) Selective supervision and per-token efficiency. Selective Ground Truth Token Training (SGT) concentrates supervision on the ~15% of output tokens that carry semantic payload. Through positive gradient coupling in position-shared transformer weights -- a token-level instance of auxiliary-task transfer -- the remaining 85% of unsupervised tokens still improve substantially, giving a 4.5x per-supervised-token efficiency (at the step-100 eval optimum, ~67% of the full-sequence loss reduction is recovered from 15% of the supervision). We prove that this improvement on unsupervised tokens is guaranteed whenever the gradient coupling coefficient gamma-bar = 0.72 is positive (Theorem 1), and show the effect is a property of natural-language structure: it collapses on shuffled text. (2) Depth compression with recurrent recovery. A 48-layer, 1B-parameter transformer is compressed to 6 layers (227M) by averaging adjacent layers and restored through learned recurrent unrolling. With 34 effective recurrent layers it reaches a held-out loss of 2.934, within measurement noise of a 566M dense model at 2.926 -- a 2.5x reduction in parameters. (3) Fusion of compressed experts. Assembling several compressed models as a Mixture of Efficient Experts (MoEE) with multi-token prediction improves over each single expert at comparable active parameters: a 2-expert MoEE reaches loss 2.789 versus 2.926 for the best single compressed model. We validate these techniques on CHERRY-1.8B, a Korean foundation model whose every trainable parameter derives from our own training runs. We are explicit throughout about the scope of the evidence (one model family, Korean data, loss-based metrics) and about which claims are established versus prospective.

Improved Predictive Deep Temporal Neural Networks with Trend Filtering

Oct 16, 2020

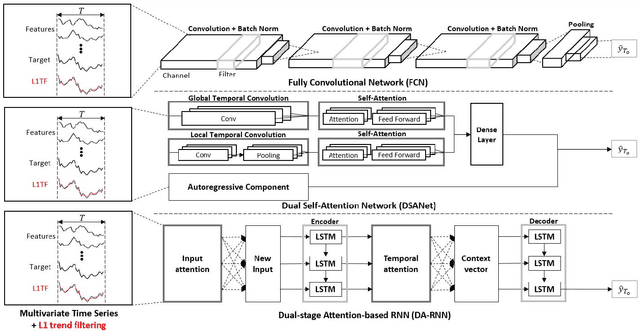

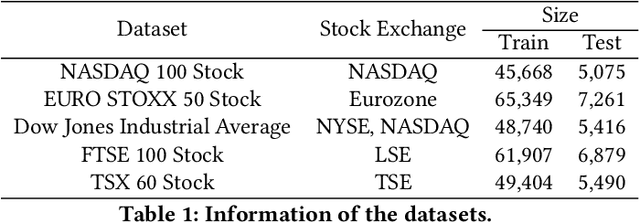

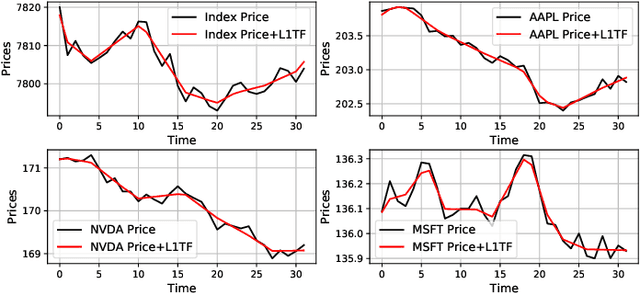

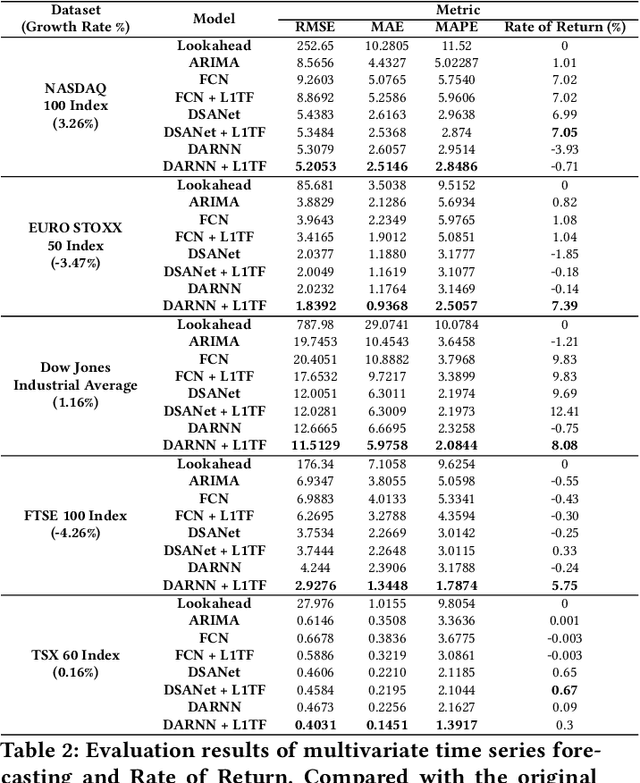

Forecasting with multivariate time series, which aims to predict future values given previous and current several univariate time series data, has been studied for decades, with one example being ARIMA. Because it is difficult to measure the extent to which noise is mixed with informative signals within rapidly fluctuating financial time series data, designing a good predictive model is not a simple task. Recently, many researchers have become interested in recurrent neural networks and attention-based neural networks, applying them in financial forecasting. There have been many attempts to utilize these methods for the capturing of long-term temporal dependencies and to select more important features in multivariate time series data in order to make accurate predictions. In this paper, we propose a new prediction framework based on deep neural networks and a trend filtering, which converts noisy time series data into a piecewise linear fashion. We reveal that the predictive performance of deep temporal neural networks improves when the training data is temporally processed by a trend filtering. To verify the effect of our framework, three deep temporal neural networks, state of the art models for predictions in time series finance data, are used and compared with models that contain trend filtering as an input feature. Extensive experiments on real-world multivariate time series data show that the proposed method is effective and significantly better than existing baseline methods.

* 8 pages, 4 figures, 3 tables, ICAIF 2020: ACM International Conference on AI in Finance