Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeElliptical slice sampling

Mar 19, 2010

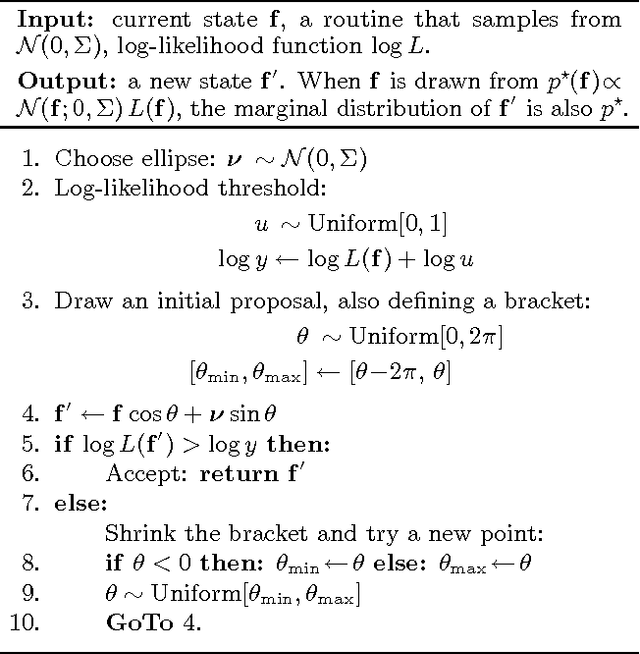

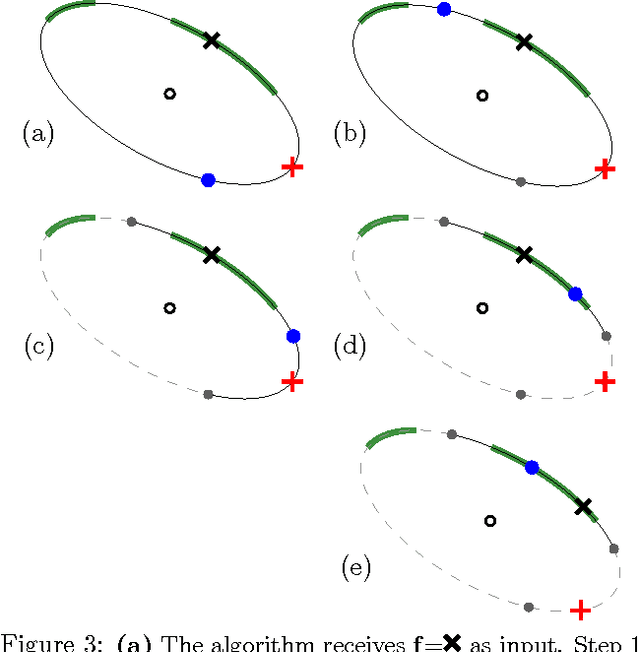

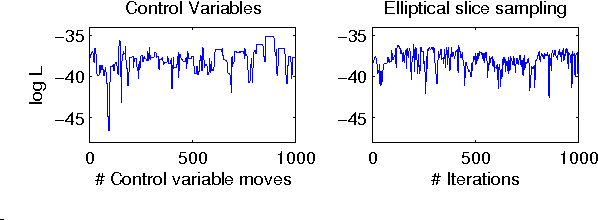

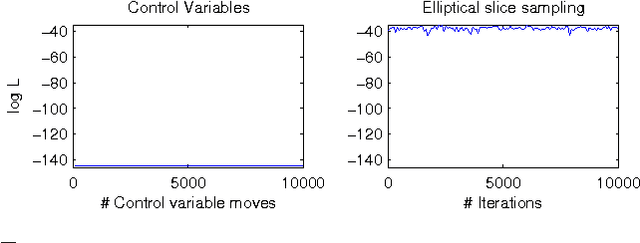

Many probabilistic models introduce strong dependencies between variables using a latent multivariate Gaussian distribution or a Gaussian process. We present a new Markov chain Monte Carlo algorithm for performing inference in models with multivariate Gaussian priors. Its key properties are: 1) it has simple, generic code applicable to many models, 2) it has no free parameters, 3) it works well for a variety of Gaussian process based models. These properties make our method ideal for use while model building, removing the need to spend time deriving and tuning updates for more complex algorithms.

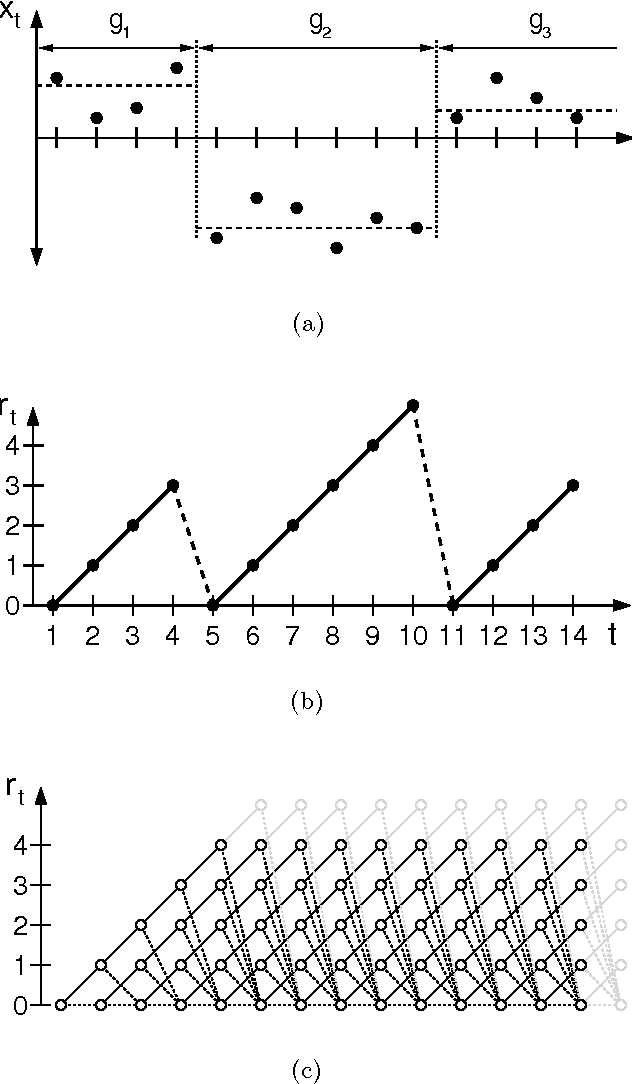

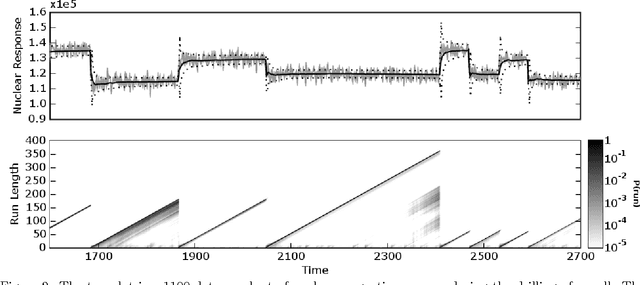

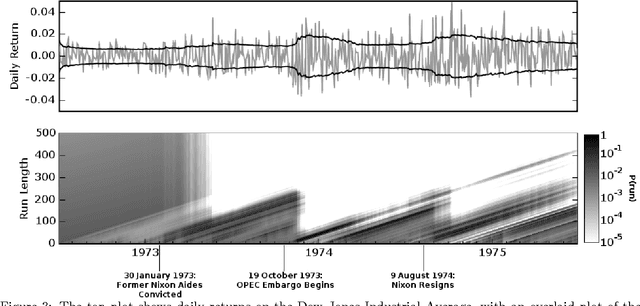

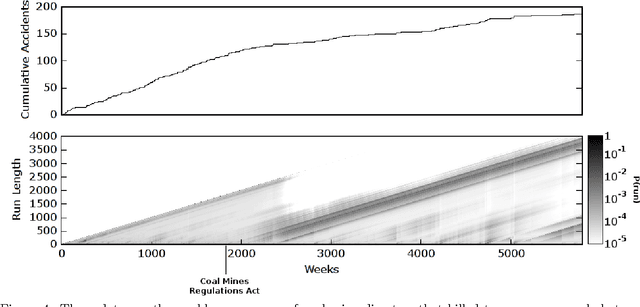

Bayesian Online Changepoint Detection

Oct 19, 2007

Changepoints are abrupt variations in the generative parameters of a data sequence. Online detection of changepoints is useful in modelling and prediction of time series in application areas such as finance, biometrics, and robotics. While frequentist methods have yielded online filtering and prediction techniques, most Bayesian papers have focused on the retrospective segmentation problem. Here we examine the case where the model parameters before and after the changepoint are independent and we derive an online algorithm for exact inference of the most recent changepoint. We compute the probability distribution of the length of the current ``run,'' or time since the last changepoint, using a simple message-passing algorithm. Our implementation is highly modular so that the algorithm may be applied to a variety of types of data. We illustrate this modularity by demonstrating the algorithm on three different real-world data sets.