Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeNoise Regularization for Conditional Density Estimation

Jul 21, 2019

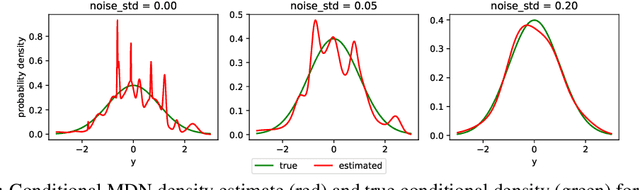

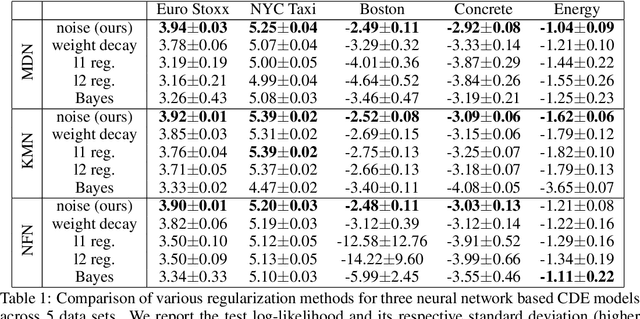

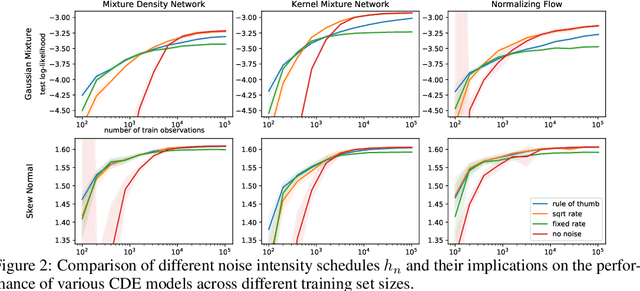

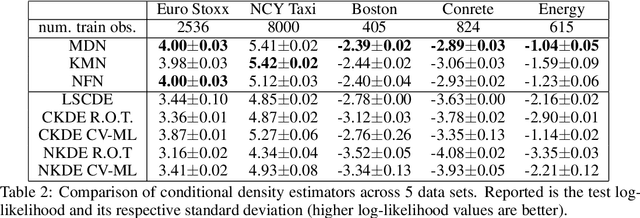

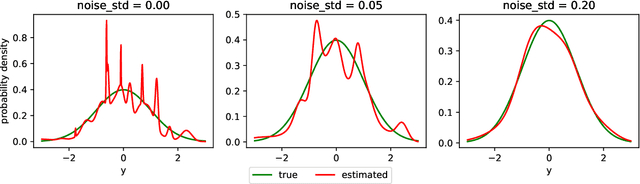

Modelling statistical relationships beyond the conditional mean is crucial in many settings. Conditional density estimation (CDE) aims to learn the full conditional probability density from data. Though highly expressive, neural network based CDE models can suffer from severe over-fitting when trained with the maximum likelihood objective. Due to the inherent structure of such models, classical regularization approaches in the parameter space are rendered ineffective. To address this issue, we develop a model-agnostic noise regularization method for CDE that adds random perturbations to the data during training. We demonstrate that the proposed approach corresponds to a smoothness regularization and prove its asymptotic consistency. In our experiments, noise regularization significantly and consistently outperforms other regularization methods across seven data sets and three CDE models. The effectiveness of noise regularization makes neural network based CDE the preferable method over previous non- and semi-parametric approaches, even when training data is scarce.

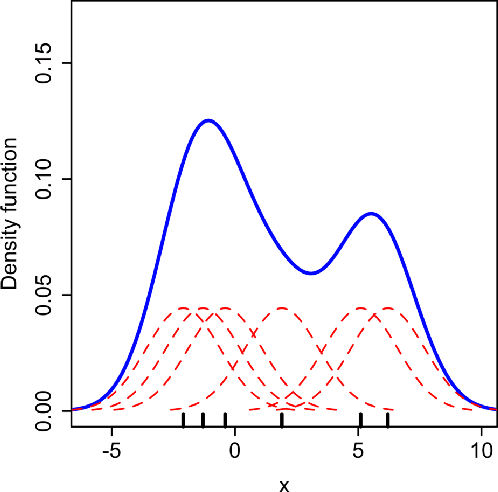

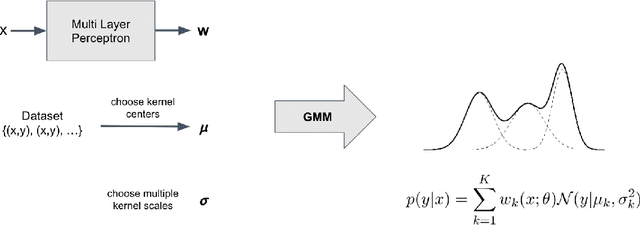

Conditional Density Estimation with Neural Networks: Best Practices and Benchmarks

Apr 13, 2019

Given a set of empirical observations, conditional density estimation aims to capture the statistical relationship between a conditional variable $\mathbf{x}$ and a dependent variable $\mathbf{y}$ by modeling their conditional probability $p(\mathbf{y}|\mathbf{x})$. The paper develops best practices for conditional density estimation for finance applications with neural networks, grounded on mathematical insights and empirical evaluations. In particular, we introduce a noise regularization and data normalization scheme, alleviating problems with over-fitting, initialization and hyper-parameter sensitivity of such estimators. We compare our proposed methodology with popular semi- and non-parametric density estimators, underpin its effectiveness in various benchmarks on simulated and Euro Stoxx 50 data and show its superior performance. Our methodology allows to obtain high-quality estimators for statistical expectations of higher moments, quantiles and non-linear return transformations, with very little assumptions about the return dynamic.