Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeFinancial Time Series Data Augmentation with Generative Adversarial Networks and Extended Intertemporal Return Plots

May 19, 2022

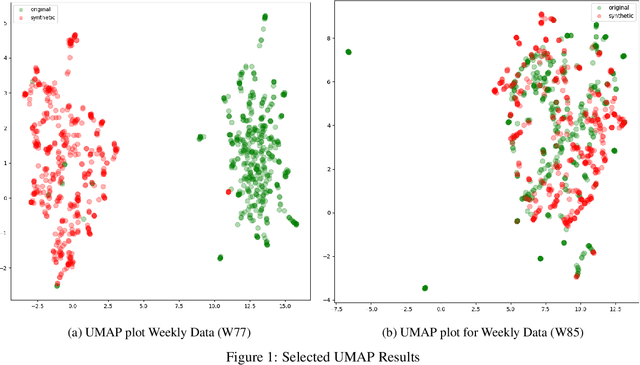

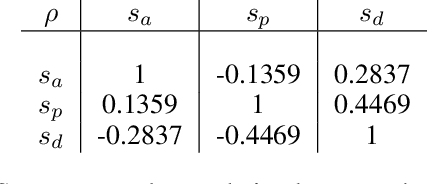

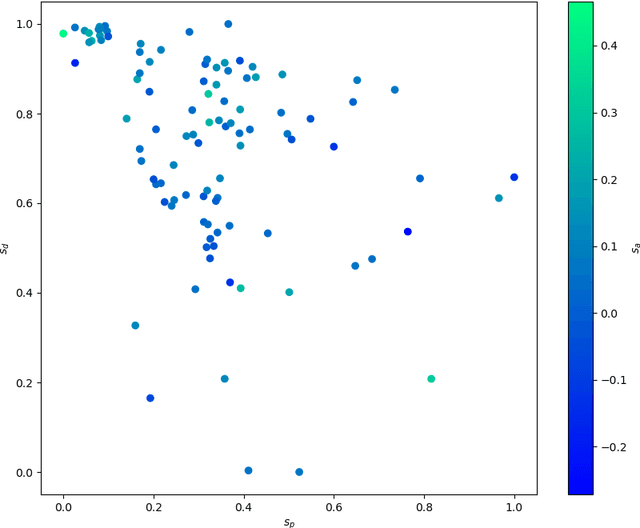

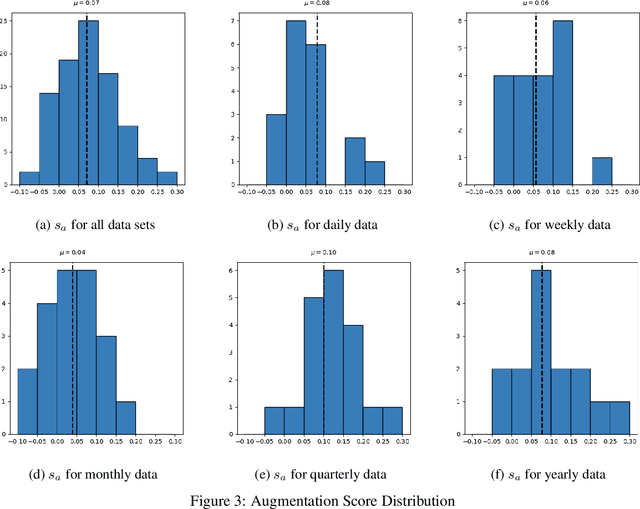

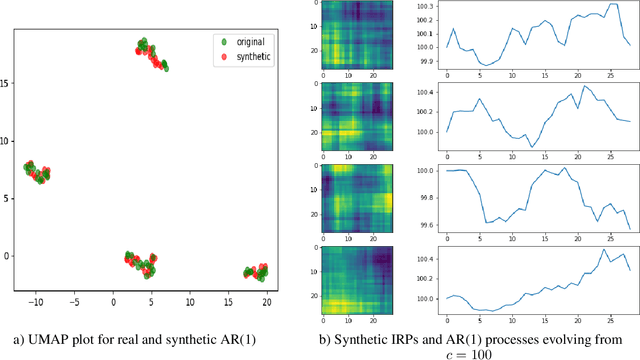

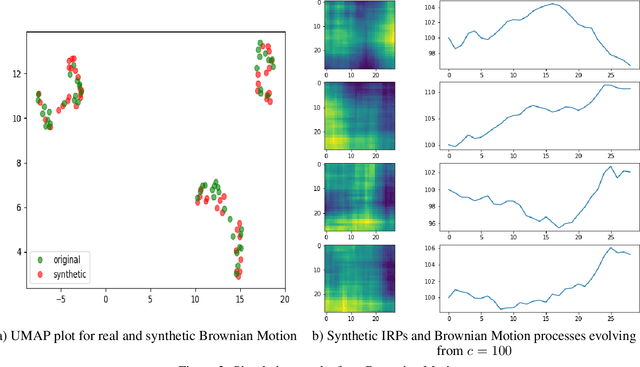

Data augmentation is a key regularization method to support the forecast and classification performance of highly parameterized models in computer vision. In the time series domain however, regularization in terms of augmentation is not equally common even though these methods have proven to mitigate effects from small sample size or non-stationarity. In this paper we apply state-of-the art image-based generative models for the task of data augmentation and introduce the extended intertemporal return plot (XIRP), a new image representation for time series. Multiple tests are conducted to assess the quality of the augmentation technique regarding its ability to synthesize time series effectively and improve forecast results on a subset of the M4 competition. We further investigate the relationship between data set characteristics and sampling results via Shapley values for feature attribution on the performance metrics and the optimal ratio of augmented data. Over all data sets, our approach proves to be effective in reducing the return forecast error by 7% on 79% of the financial data sets with varying statistical properties and frequencies.

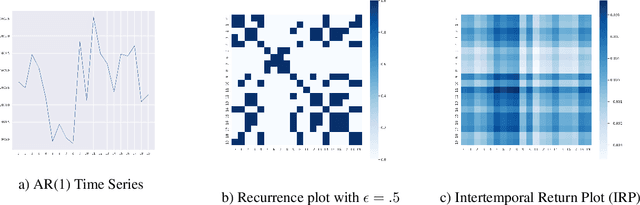

Leveraging Image-based Generative Adversarial Networks for Time Series Generation

Dec 15, 2021

Generative models synthesize image data with great success regarding sampling quality, diversity and feature disentanglement. Generative models for time series lack these benefits due to a missing representation, which captures temporal dynamics and allows inversion for sampling. The paper proposes the intertemporal return plot (IRP) representation to facilitate the use of image-based generative adversarial networks for time series generation. The representation proves effective in capturing time series characteristics and, compared to alternative representations, benefits from invertibility and scale-invariance. Empirical benchmarks confirm these features and demonstrate that the IRP enables an off-the-shelf Wasserstein GAN with gradient penalty to sample realistic time series, which outperform a specialized RNN-based GAN, while simultaneously reducing model complexity.