Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeVolterra Generative Models

Jun 16, 2026Score-based diffusion models typically use Brownian perturbations, which provide tractable reverse-time dynamics but impose memoryless noising. We introduce Volterra generative models, a continuous-time score-based framework whose forward process injects path-dependent noise through fractional kernels. To handle the non-Markovian and non-semimartingale dynamics, we construct finite-dimensional Markovian lifts using Gaussian quadrature in both regimes and a hybrid finite-difference exponential approximation in the smooth regime. We prove squared error bounds, derive an augmented linear-Gaussian forward process, and show that the learning can remain data-dimensional by considering residual states and analytic auxiliary Gaussian scores. We also identify covariance and reverse-time degeneracies caused by shared Brownian factors and signed smooth-regime weights. The degeneracy motivates stabilized conditioning and, for stiff larger lifts, a Gaussian-bridge reconstruction sampler. Experiments on MNIST and CIFAR-10 show that persistent fractional perturbations with small Markovian lifts can improve score-based generation on MNIST and provide a promising extension to natural images, while the bridge sampler provides a stability mechanism for larger lifts.

Continuous-time Online Learning via Mean-Field Neural Networks: Regret Analysis in Diffusion Environments

Apr 13, 2026We study continuous-time online learning where data are generated by a diffusion process with unknown coefficients. The learner employs a two-layer neural network, continuously updating its parameters in a non-anticipative manner. The mean-field limit of the learning dynamics corresponds to a stochastic Wasserstein gradient flow adapted to the data filtration. We establish regret bounds for both the mean-field limit and finite-particle system. Our analysis leverages the logarithmic Sobolev inequality, Polyak-Lojasiewicz condition, Malliavin calculus, and uniform-in-time propagation of chaos. Under displacement convexity, we obtain a constant static regret bound. In the general non-convex setting, we derive explicit linear regret bounds characterizing the effects of data variation, entropic exploration, and quadratic regularization. Finally, our simulations demonstrate the outperformance of the online approach and the impact of network width and regularization parameters.

Fitted Value Iteration Methods for Bicausal Optimal Transport

Jun 22, 2023We develop a fitted value iteration (FVI) method to compute bicausal optimal transport (OT) where couplings have an adapted structure. Based on the dynamic programming formulation, FVI adopts a function class to approximate the value functions in bicausal OT. Under the concentrability condition and approximate completeness assumption, we prove the sample complexity using (local) Rademacher complexity. Furthermore, we demonstrate that multilayer neural networks with appropriate structures satisfy the crucial assumptions required in sample complexity proofs. Numerical experiments reveal that FVI outperforms linear programming and adapted Sinkhorn methods in scalability as the time horizon increases, while still maintaining acceptable accuracy.

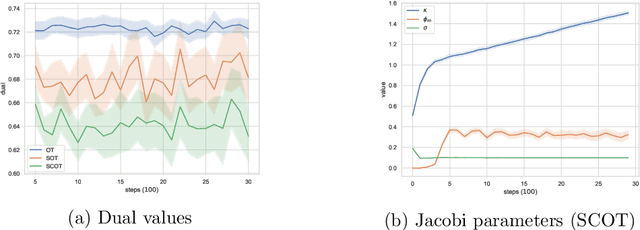

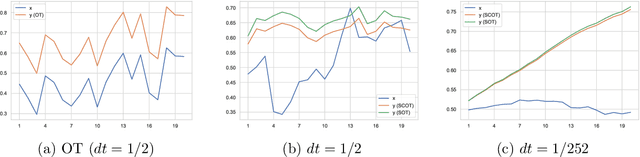

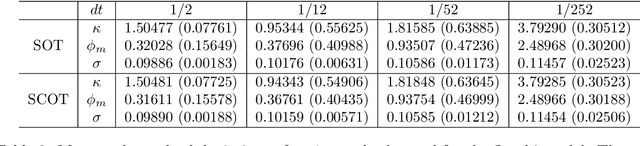

Distributionally robust risk evaluation with causality constraint and structural information

Mar 20, 2022

This work studies distributionally robust evaluation of expected function values over temporal data. A set of alternative measures is characterized by the causal optimal transport. We prove the strong duality and recast the causality constraint as minimization over an infinite-dimensional test function space. We approximate test functions by neural networks and prove the sample complexity with Rademacher complexity. Moreover, when structural information is available to further restrict the ambiguity set, we prove the dual formulation and provide efficient optimization methods. Simulation on stochastic volatility and empirical analysis on stock indices demonstrate that our framework offers an attractive alternative to the classic optimal transport formulation.

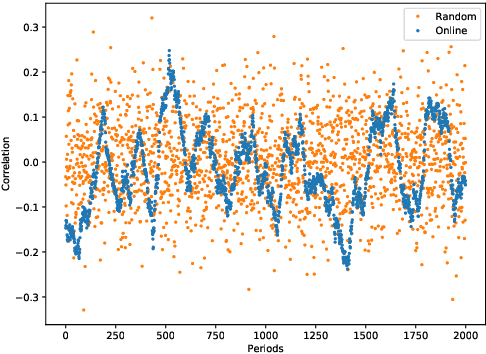

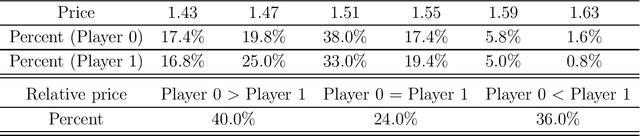

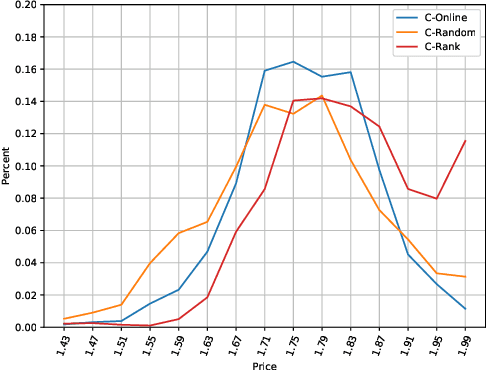

Understanding algorithmic collusion with experience replay

Feb 18, 2021

In an infinitely repeated pricing game, pricing algorithms based on artificial intelligence (Q-learning) may consistently learn to charge supra-competitive prices even without communication. Although concerns on algorithmic collusion have arisen, little is known on underlying factors. In this work, we experimentally analyze the dynamics of algorithms with three variants of experience replay. Algorithmic collusion still has roots in human preferences. Randomizing experience yields prices close to the static Bertrand equilibrium and higher prices are easily restored by favoring the latest experience. Moreover, relative performance concerns also stabilize the collusion. Finally, we investigate the scenarios with heterogeneous agents and test robustness on various factors.