Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeDirectional FDR Control for Sub-Gaussian Sparse GLMs

Paper and Code

May 02, 2021

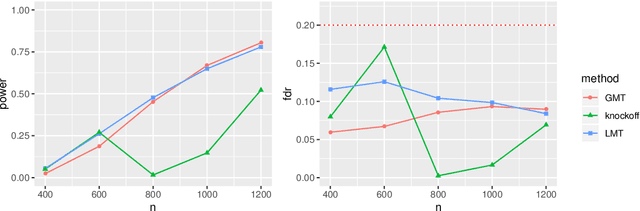

High-dimensional sparse generalized linear models (GLMs) have emerged in the setting that the number of samples and the dimension of variables are large, and even the dimension of variables grows faster than the number of samples. False discovery rate (FDR) control aims to identify some small number of statistically significantly nonzero results after getting the sparse penalized estimation of GLMs. Using the CLIME method for precision matrix estimations, we construct the debiased-Lasso estimator and prove the asymptotical normality by minimax-rate oracle inequalities for sparse GLMs. In practice, it is often needed to accurately judge each regression coefficient's positivity and negativity, which determines whether the predictor variable is positively or negatively related to the response variable conditionally on the rest variables. Using the debiased estimator, we establish multiple testing procedures. Under mild conditions, we show that the proposed debiased statistics can asymptotically control the directional (sign) FDR and directional false discovery variables at a pre-specified significance level. Moreover, it can be shown that our multiple testing procedure can approximately achieve a statistical power of 1. We also extend our methods to the two-sample problems and propose the two-sample test statistics. Under suitable conditions, we can asymptotically achieve directional FDR control and directional FDV control at the specified significance level for two-sample problems. Some numerical simulations have successfully verified the FDR control effects of our proposed testing procedures, which sometimes outperforms the classical knockoff method.