Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeHigh-Dimensional Multivariate Forecasting with Low-Rank Gaussian Copula Processes

Paper and Code

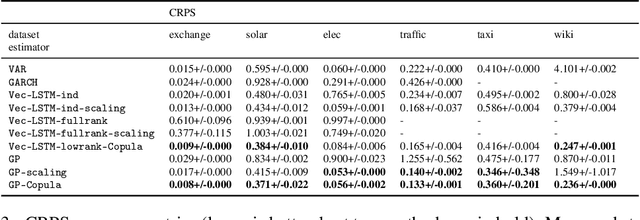

Predicting the dependencies between observations from multiple time series is critical for applications such as anomaly detection, financial risk management, causal analysis, or demand forecasting. However, the computational and numerical difficulties of estimating time-varying and high-dimensional covariance matrices often limits existing methods to handling at most a few hundred dimensions or requires making strong assumptions on the dependence between series. We propose to combine an RNN-based time series model with a Gaussian copula process output model with a low-rank covariance structure to reduce the computational complexity and handle non-Gaussian marginal distributions. This permits to drastically reduce the number of parameters and consequently allows the modeling of time-varying correlations of thousands of time series. We show on several real-world datasets that our method provides significant accuracy improvements over state-of-the-art baselines and perform an ablation study analyzing the contributions of the different components of our model.