Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeConditional Density Estimation with Neural Networks: Best Practices and Benchmarks

Paper and Code

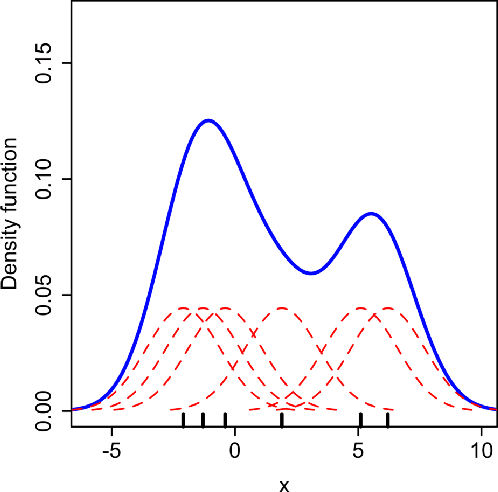

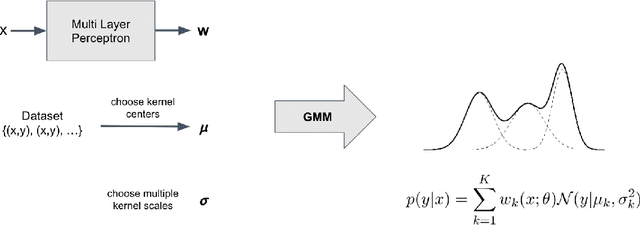

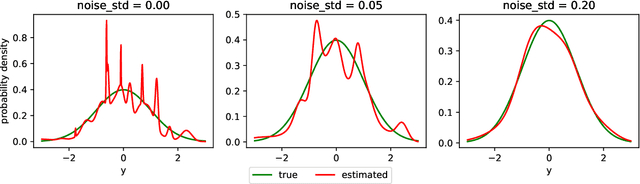

Given a set of empirical observations, conditional density estimation aims to capture the statistical relationship between a conditional variable $\mathbf{x}$ and a dependent variable $\mathbf{y}$ by modeling their conditional probability $p(\mathbf{y}|\mathbf{x})$. The paper develops best practices for conditional density estimation for finance applications with neural networks, grounded on mathematical insights and empirical evaluations. In particular, we introduce a noise regularization and data normalization scheme, alleviating problems with over-fitting, initialization and hyper-parameter sensitivity of such estimators. We compare our proposed methodology with popular semi- and non-parametric density estimators, underpin its effectiveness in various benchmarks on simulated and Euro Stoxx 50 data and show its superior performance. Our methodology allows to obtain high-quality estimators for statistical expectations of higher moments, quantiles and non-linear return transformations, with very little assumptions about the return dynamic.