Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeRmd: Robust Modal Decomposition with Constrained Bandwidth

Oct 27, 2025Modal decomposition techniques, such as Empirical Mode Decomposition (EMD), Variational Mode Decomposition (VMD), and Singular Spectrum Analysis (SSA), have advanced time-frequency signal analysis since the early 21st century. These methods are generally classified into two categories: numerical optimization-based methods (EMD, VMD) and spectral decomposition methods (SSA) that consider the physical meaning of signals. The former can produce spurious modes due to the lack of physical constraints, while the latter is more sensitive to noise and struggles with nonlinear signals. Despite continuous improvements in these methods, a modal decomposition approach that effectively combines the strengths of both categories remains elusive. This paper thus proposes a Robust Modal Decomposition (RMD) method with constrained bandwidth, which preserves the intrinsic structure of the signal by mapping the time series into its trajectory-GRAM matrix in phase space. Moreover, the method incorporates bandwidth constraints during the decomposition process, enhancing noise resistance. Extensive experiments on synthetic and real-world datasets, including millimeter-wave radar echoes, electrocardiogram (ECG), phonocardiogram (PCG), and bearing fault detection data, demonstrate the method's effectiveness and versatility. All code and dataset samples are available on GitHub: https://github.com/Einstein-sworder/RMD.

A new hybrid approach for crude oil price forecasting: Evidence from multi-scale data

Feb 22, 2020

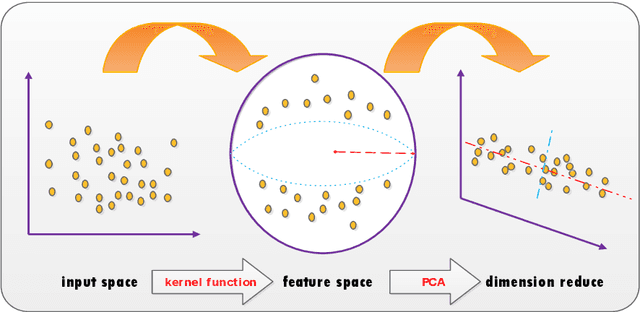

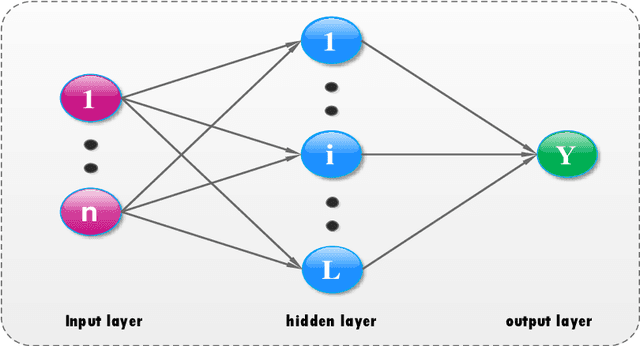

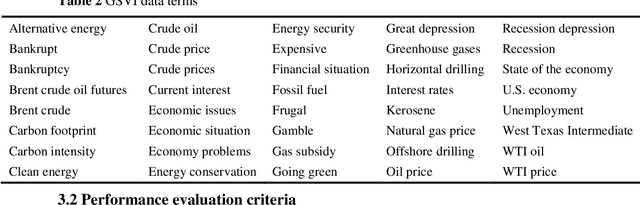

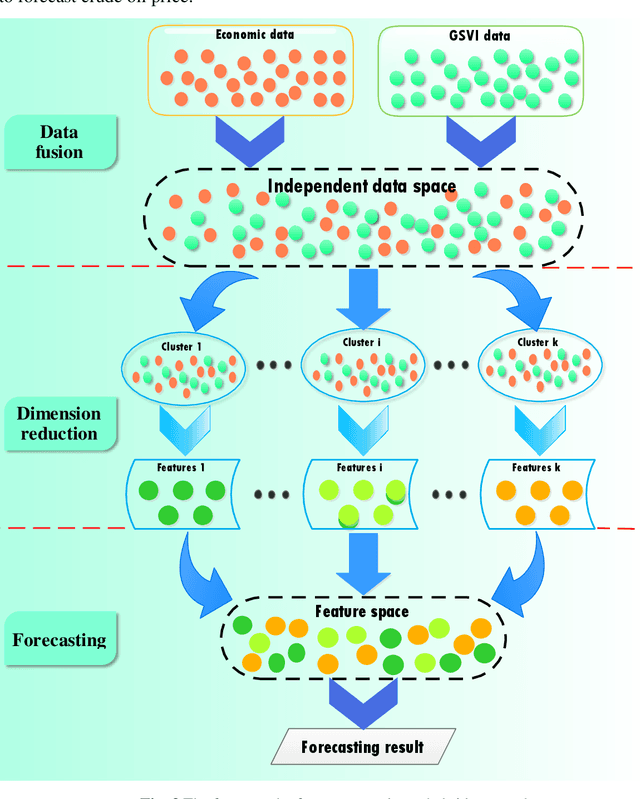

Faced with the growing research towards crude oil price fluctuations influential factors following the accelerated development of Internet technology, accessible data such as Google search volume index are increasingly quantified and incorporated into forecasting approaches. In this paper, we apply multi-scale data that including both GSVI data and traditional economic data related to crude oil price as independent variables and propose a new hybrid approach for monthly crude oil price forecasting. This hybrid approach, based on divide and conquer strategy, consists of K-means method, kernel principal component analysis and kernel extreme learning machine , where K-means method is adopted to divide input data into certain clusters, KPCA is applied to reduce dimension, and KELM is employed for final crude oil price forecasting. The empirical result can be analyzed from data and method levels. At the data level, GSVI data perform better than economic data in level forecasting accuracy but with opposite performance in directional forecasting accuracy because of Herd Behavior, while hybrid data combined their advantages and obtain best forecasting performance in both level and directional accuracy. At the method level, the approaches with K-means perform better than those without K-means, which demonstrates that divide and conquer strategy can effectively improve the forecasting performance.