Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeRealized Volatility Forecasting for New Issues and Spin-Offs using Multi-Source Transfer Learning

Mar 16, 2025Forecasting the volatility of financial assets is essential for various financial applications. This paper addresses the challenging task of forecasting the volatility of financial assets with limited historical data, such as new issues or spin-offs, by proposing a multi-source transfer learning approach. Specifically, we exploit complementary source data of assets with a substantial historical data record by selecting source time series instances that are most similar to the limited target data of the new issue/spin-off. Based on these instances and the target data, we estimate linear and non-linear realized volatility models and compare their forecasting performance to forecasts of models trained exclusively on the target data, and models trained on the entire source and target data. The results show that our transfer learning approach outperforms the alternative models and that the integration of complementary data is also beneficial immediately after the initial trading day of the new issue/spin-off.

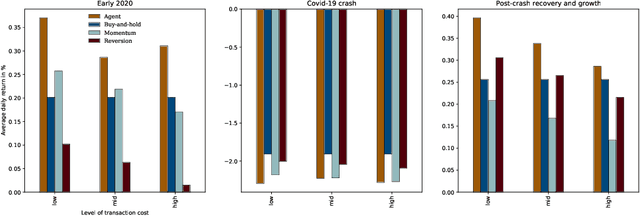

High-Dimensional Stock Portfolio Trading with Deep Reinforcement Learning

Dec 09, 2021

This paper proposes a Deep Reinforcement Learning algorithm for financial portfolio trading based on Deep Q-learning. The algorithm is capable of trading high-dimensional portfolios from cross-sectional datasets of any size which may include data gaps and non-unique history lengths in the assets. We sequentially set up environments by sampling one asset for each environment while rewarding investments with the resulting asset's return and cash reservation with the average return of the set of assets. This enforces the agent to strategically assign capital to assets that it predicts to perform above-average. We apply our methodology in an out-of-sample analysis to 48 US stock portfolio setups, varying in the number of stocks from ten up to 500 stocks, in the selection criteria and in the level of transaction costs. The algorithm on average outperforms all considered passive and active benchmark investment strategies by a large margin using only one hyperparameter setup for all portfolios.