Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeIdentifying Pairs in Simulated Bio-Medical Time-Series

May 12, 2013

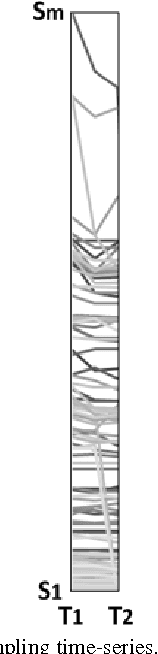

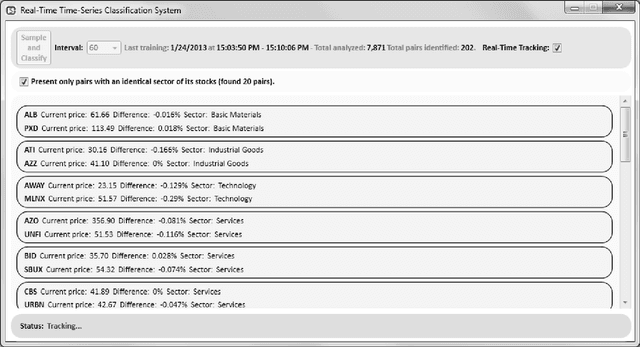

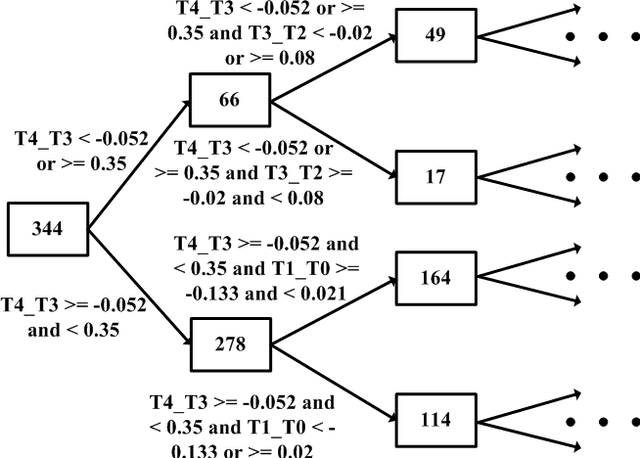

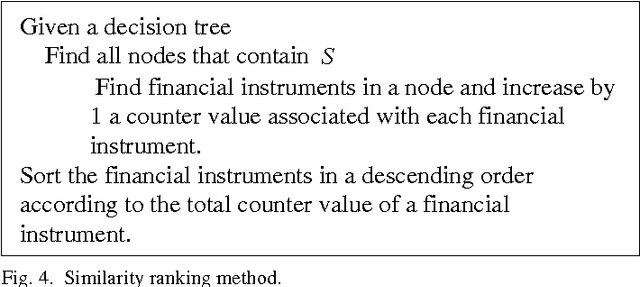

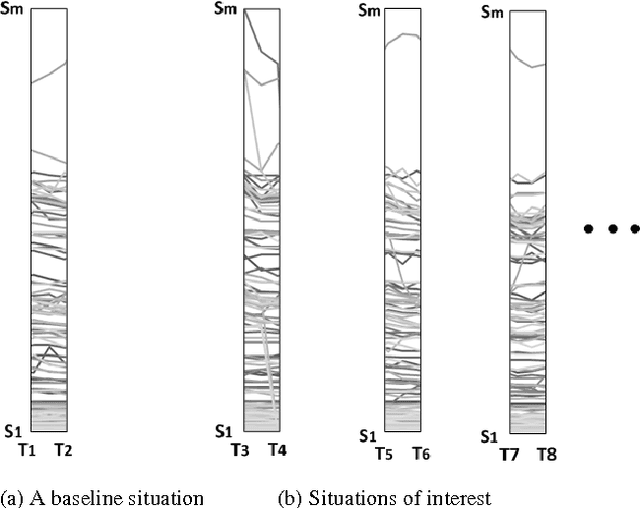

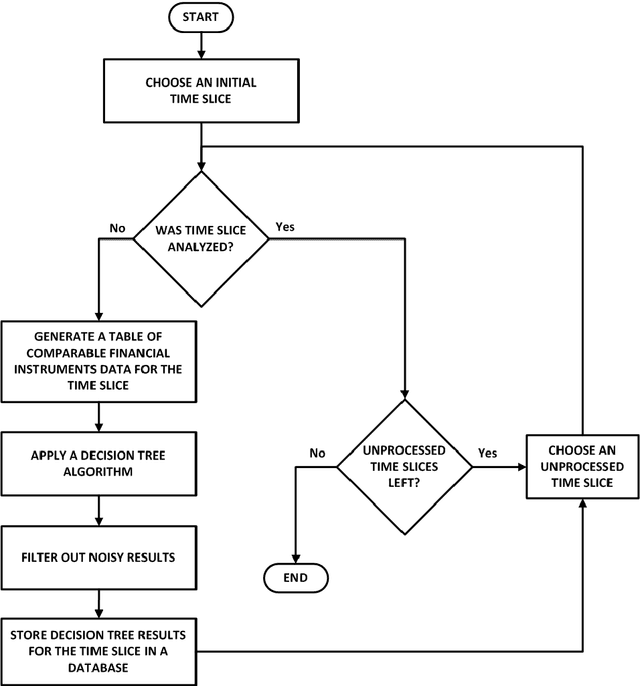

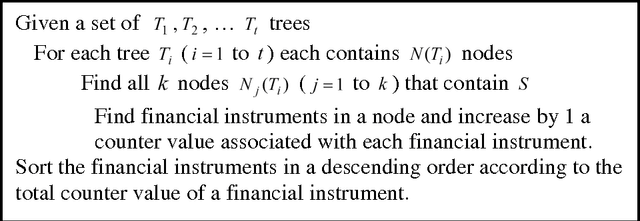

The paper presents a time-series-based classification approach to identify similarities in pairs of simulated human-generated patterns. An example for a pattern is a time-series representing a heart rate during a specific time-range, wherein the time-series is a sequence of data points that represent the changes in the heart rate values. A bio-medical simulator system was developed to acquire a collection of 7,871 price patterns of financial instruments. The financial instruments traded in real-time on three American stock exchanges, NASDAQ, NYSE, and AMEX, simulate bio-medical measurements. The system simulates a human in which each price pattern represents one bio-medical sensor. Data provided during trading hours from the stock exchanges allowed real-time classification. Classification is based on new machine learning techniques: self-labeling, which allows the application of supervised learning methods on unlabeled time-series and similarity ranking, which applied on a decision tree learning algorithm to classify time-series regardless of type and quantity.

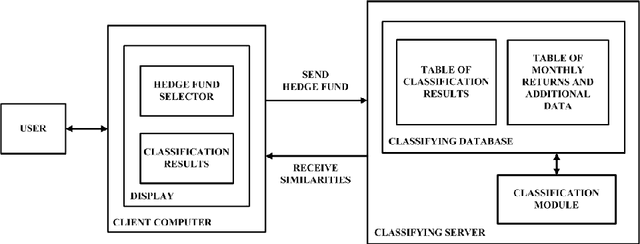

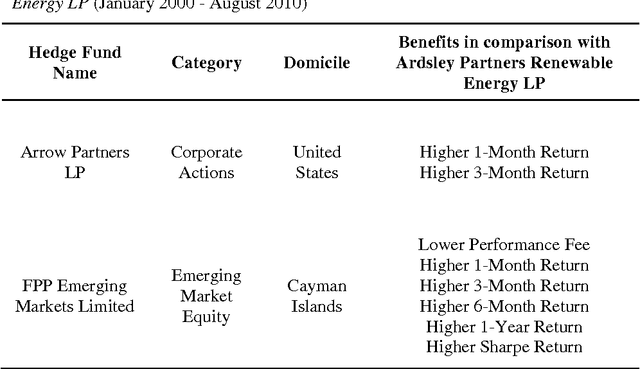

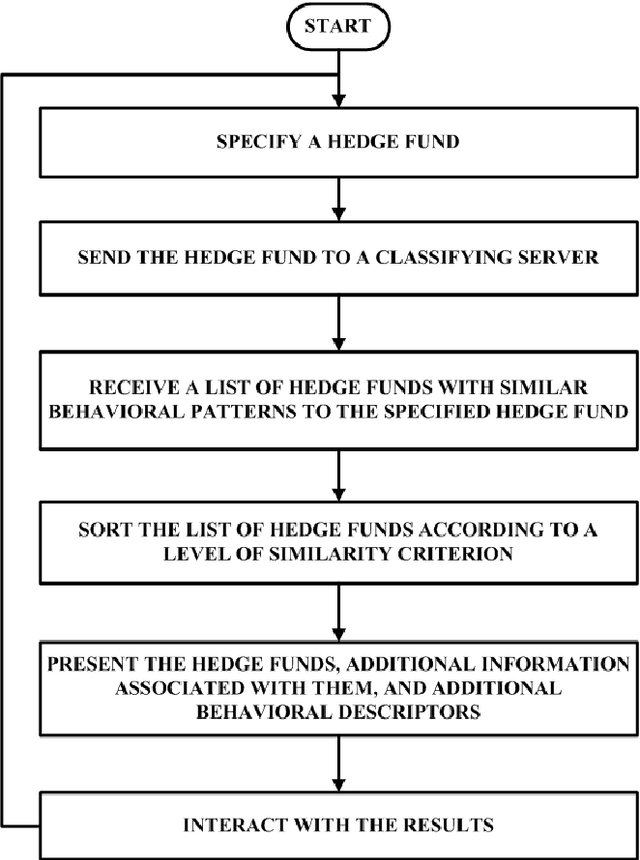

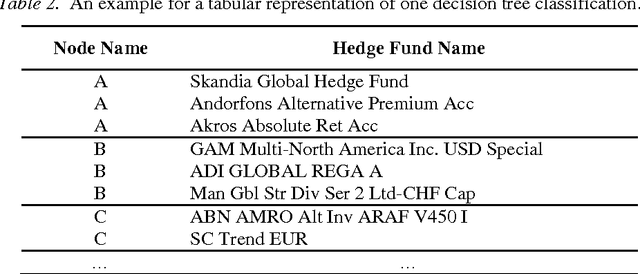

A Method for Comparing Hedge Funds

Mar 19, 2013

The paper presents new machine learning methods: signal composition, which classifies time-series regardless of length, type, and quantity; and self-labeling, a supervised-learning enhancement. The paper describes further the implementation of the methods on a financial search engine system to identify behavioral similarities among time-series representing monthly returns of 11,312 hedge funds operated during approximately one decade (2000 - 2010). The presented approach of cross-category and cross-location classification assists the investor to identify alternative investments.

Bio-Signals-based Situation Comparison Approach to Predict Pain

Mar 19, 2013

This paper describes a time-series-based classification approach to identify similarities between bio-medical-based situations. The proposed approach allows classifying collections of time-series representing bio-medical measurements, i.e., situations, regardless of the type, the length and the quantity of the time-series a situation comprised of.

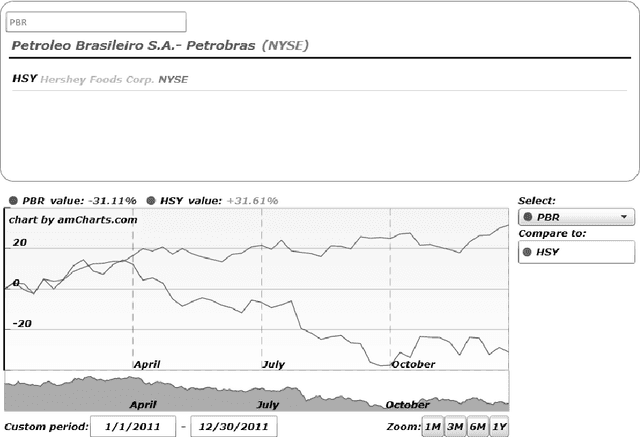

Inverse Signal Classification for Financial Instruments

Mar 19, 2013

The paper presents new machine learning methods: signal composition, which classifies time-series regardless of length, type, and quantity; and self-labeling, a supervised-learning enhancement. The paper describes further the implementation of the methods on a financial search engine system using a collection of 7,881 financial instruments traded during 2011 to identify inverse behavior among the time-series.