Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeHardML: A Benchmark For Evaluating Data Science And Machine Learning knowledge and reasoning in AI

Jan 26, 2025

We present HardML, a benchmark designed to evaluate the knowledge and reasoning abilities in the fields of data science and machine learning. HardML comprises a diverse set of 100 challenging multiple-choice questions, handcrafted over a period of 6 months, covering the most popular and modern branches of data science and machine learning. These questions are challenging even for a typical Senior Machine Learning Engineer to answer correctly. To minimize the risk of data contamination, HardML uses mostly original content devised by the author. Current state of the art AI models achieve a 30% error rate on this benchmark, which is about 3 times larger than the one achieved on the equivalent, well known MMLU ML. While HardML is limited in scope and not aiming to push the frontier, primarily due to its multiple choice nature, it serves as a rigorous and modern testbed to quantify and track the progress of top AI. While plenty benchmarks and experimentation in LLM evaluation exist in other STEM fields like mathematics, physics and chemistry, the subfields of data science and machine learning remain fairly underexplored.

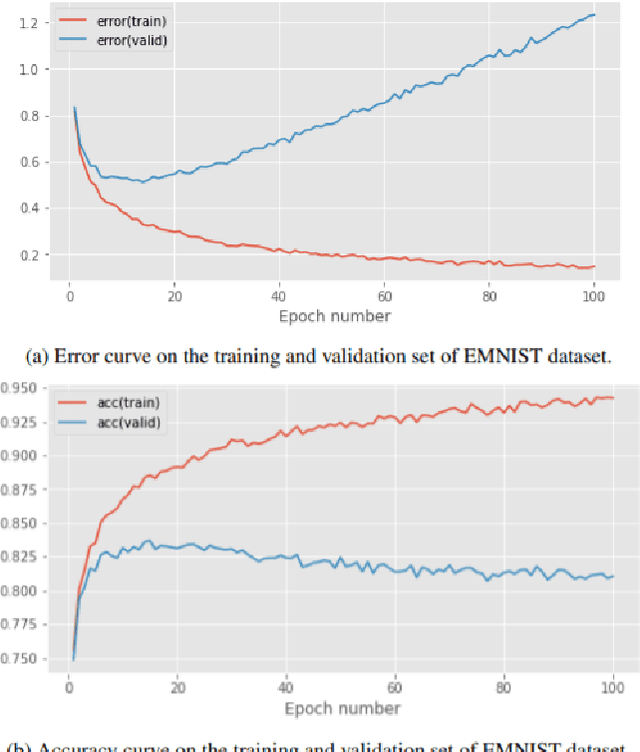

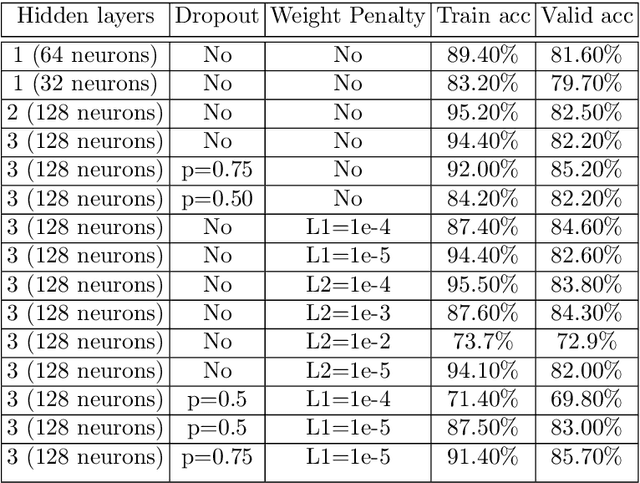

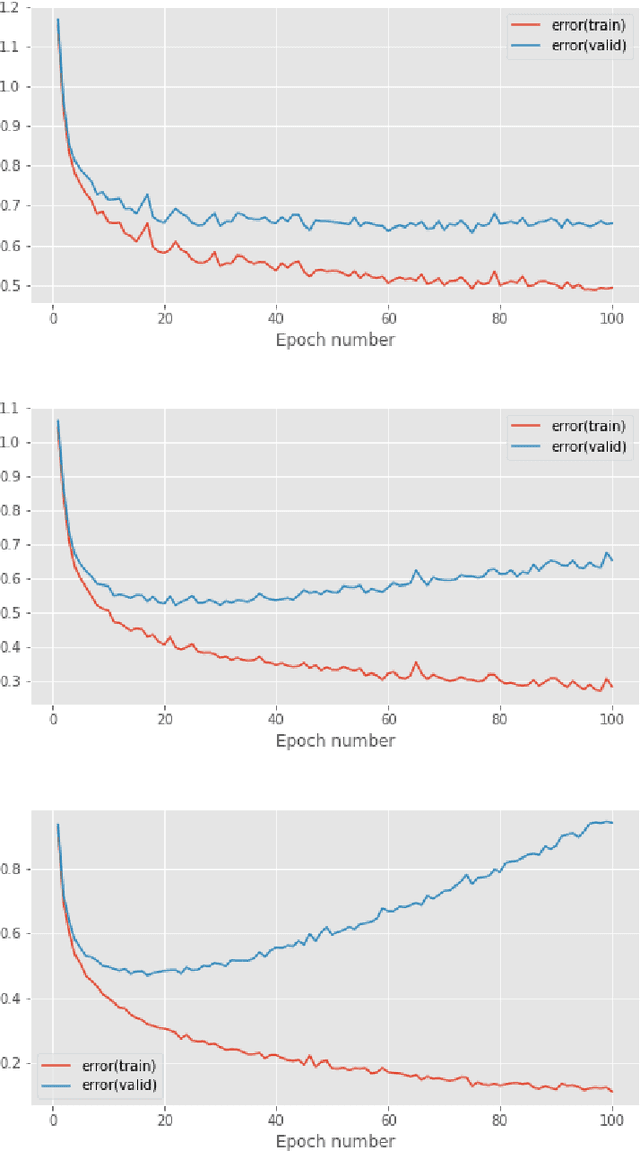

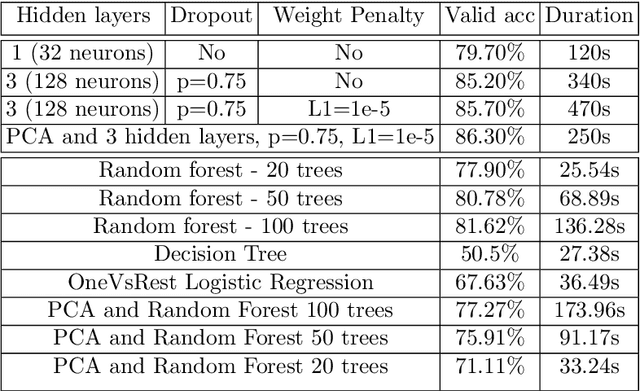

A contextual analysis of multi-layer perceptron models in classifying hand-written digits and letters: limited resources

Jul 05, 2021

Classifying hand-written digits and letters has taken a big leap with the introduction of ConvNets. However, on very constrained hardware the time necessary to train such models would be high. Our main contribution is twofold. First, we extensively test an end-to-end vanilla neural network (MLP) approach in pure numpy without any pre-processing or feature extraction done beforehand. Second, we show that basic data mining operations can significantly improve the performance of the models in terms of computational time, without sacrificing much accuracy. We illustrate our claims on a simpler variant of the Extended MNIST dataset, called Balanced EMNIST dataset. Our experiments show that, without any data mining, we get increased generalization performance when using more hidden layers and regularization techniques, the best model achieving 84.83% accuracy on a test dataset. Using dimensionality reduction done by PCA we were able to increase that figure to 85.08% with only 10% of the original feature space, reducing the memory size needed by 64%. Finally, adding methods to remove possibly harmful training samples like deviation from the mean helped us to still achieve over 84% test accuracy but with only 32.8% of the original memory size for the training set. This compares favorably to the majority of literature results obtained through similar architectures. Although this approach gets outshined by state-of-the-art models, it does scale to some (AlexNet, VGGNet) trained on 50% of the same dataset.

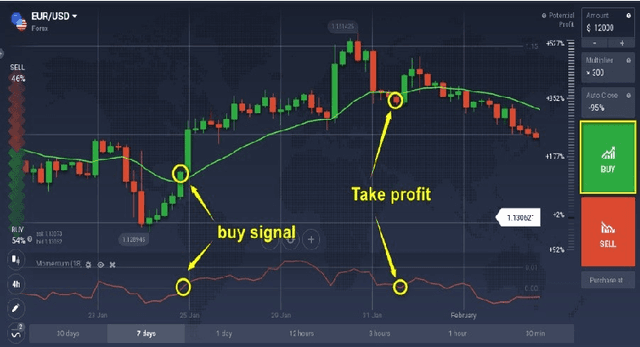

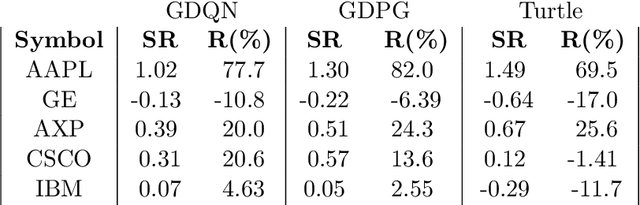

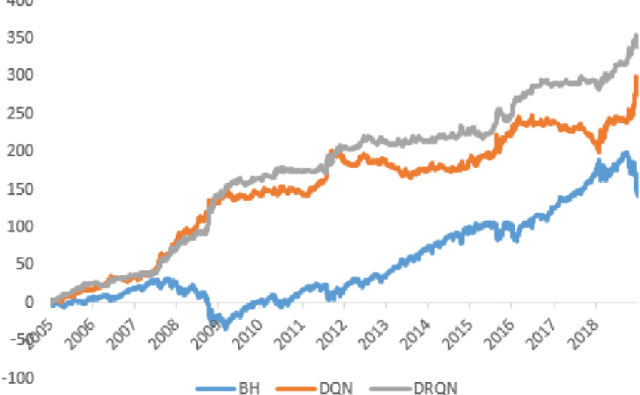

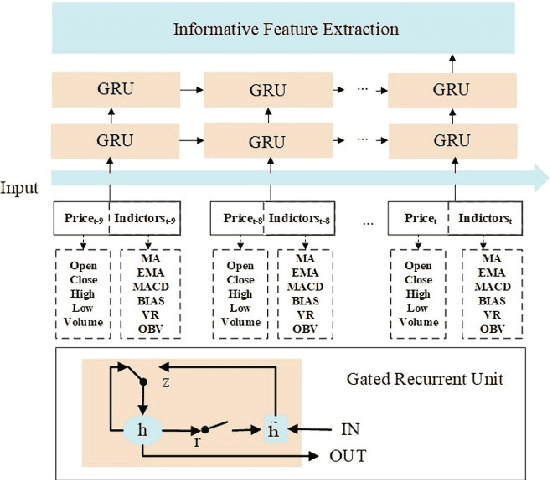

Deep Reinforcement Learning in Quantitative Algorithmic Trading: A Review

May 31, 2021

Algorithmic stock trading has become a staple in today's financial market, the majority of trades being now fully automated. Deep Reinforcement Learning (DRL) agents proved to be to a force to be reckon with in many complex games like Chess and Go. We can look at the stock market historical price series and movements as a complex imperfect information environment in which we try to maximize return - profit and minimize risk. This paper reviews the progress made so far with deep reinforcement learning in the subdomain of AI in finance, more precisely, automated low-frequency quantitative stock trading. Many of the reviewed studies had only proof-of-concept ideals with experiments conducted in unrealistic settings and no real-time trading applications. For the majority of the works, despite all showing statistically significant improvements in performance compared to established baseline strategies, no decent profitability level was obtained. Furthermore, there is a lack of experimental testing in real-time, online trading platforms and a lack of meaningful comparisons between agents built on different types of DRL or human traders. We conclude that DRL in stock trading has showed huge applicability potential rivalling professional traders under strong assumptions, but the research is still in the very early stages of development.