Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeBrownian ReLU(Br-ReLU): A New Activation Function for a Long-Short Term Memory (LSTM) Network

Jan 23, 2026Deep learning models are effective for sequential data modeling, yet commonly used activation functions such as ReLU, LeakyReLU, and PReLU often exhibit gradient instability when applied to noisy, non-stationary financial time series. This study introduces BrownianReLU, a stochastic activation function induced by Brownian motion that enhances gradient propagation and learning stability in Long Short-Term Memory (LSTM) networks. Using Monte Carlo simulation, BrownianReLU provides a smooth, adaptive response for negative inputs, mitigating the dying ReLU problem. The proposed activation is evaluated on financial time series from Apple, GCB, and the S&P 500, as well as LendingClub loan data for classification. Results show consistently lower Mean Squared Error and higher $R^2$ values, indicating improved predictive accuracy and generalization. Although ROC-AUC metric is limited in classification tasks, activation choice significantly affects the trade-off between accuracy and sensitivity, with Brownian ReLU and the selected activation functions yielding practically meaningful performance.

Are Bitcoins price predictable? Evidence from machine learning techniques using technical indicators

Sep 03, 2019

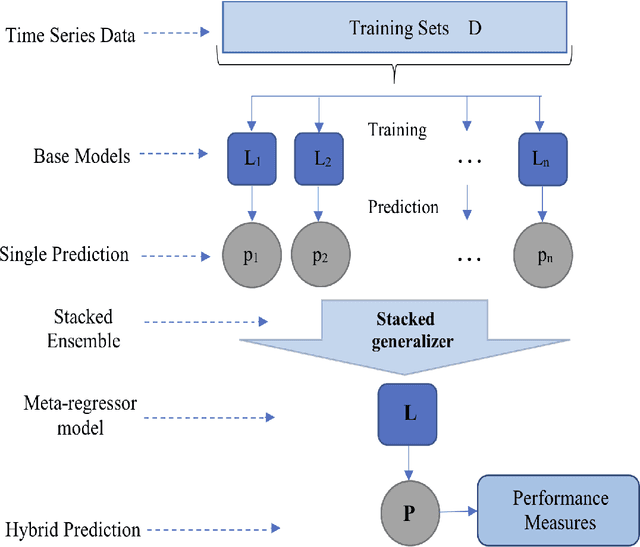

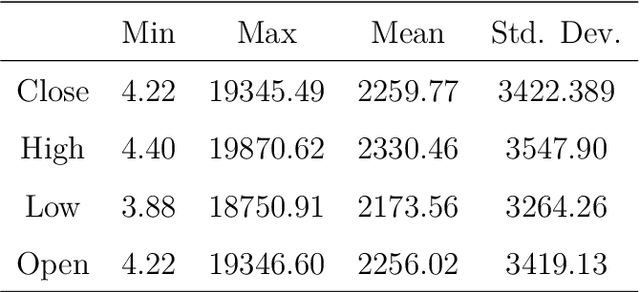

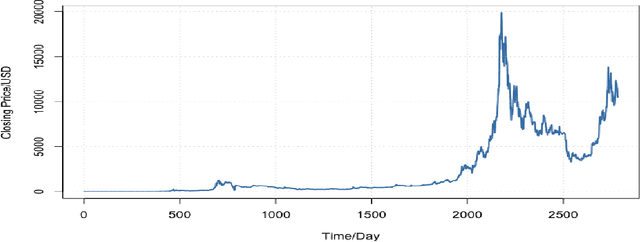

The uncertainties in future Bitcoin price make it difficult to accurately predict the price of Bitcoin. Accurately predicting the price for Bitcoin is therefore important for decision-making process of investors and market players in the cryptocurrency market. Using historical data from 01/01/2012 to 16/08/2019, machine learning techniques (Generalized linear model via penalized maximum likelihood, random forest, support vector regression with linear kernel, and stacking ensemble) were used to forecast the price of Bitcoin. The prediction models employed key and high dimensional technical indicators as the predictors. The performance of these techniques were evaluated using mean absolute percentage error (MAPE), root mean square error (RMSE), mean absolute error (MAE), and coefficient of determination (R-squared). The performance metrics revealed that the stacking ensemble model with two base learner (random forest and generalized linear model via penalized maximum likelihood) and support vector regression with linear kernel as meta-learner was the optimal model for forecasting Bitcoin price. The MAPE, RMSE, MAE, and R-squared values for the stacking ensemble model were 0.0191%, 15.5331 USD, 124.5508 USD, and 0.9967 respectively. These values show a high degree of reliability in predicting the price of Bitcoin using the stacking ensemble model. Accurately predicting the future price of Bitcoin will yield significant returns for investors and market players in the cryptocurrency market.

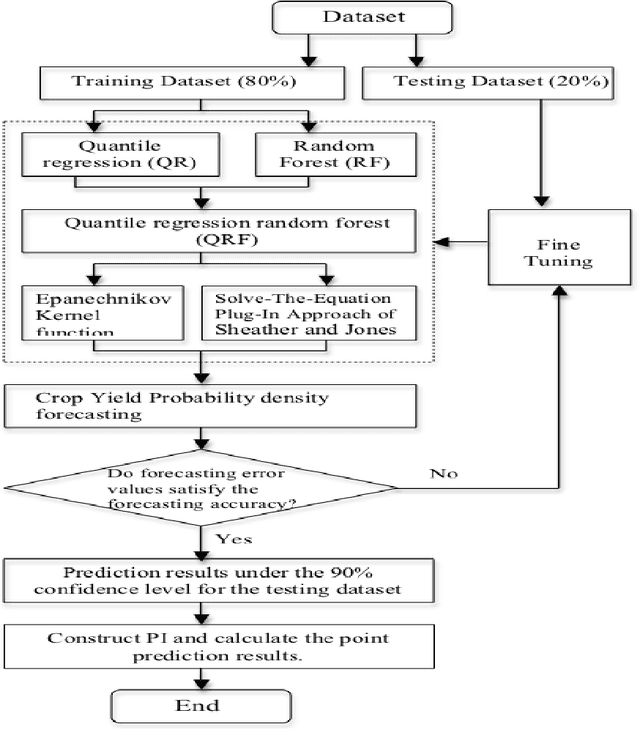

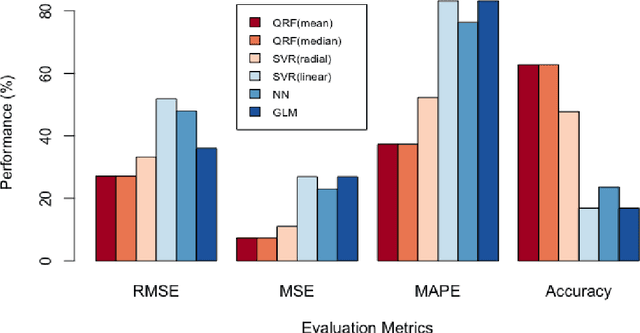

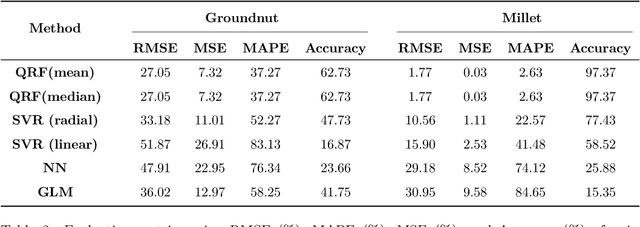

Crop yield probability density forecasting via quantile random forest and Epanechnikov Kernel function

Apr 23, 2019

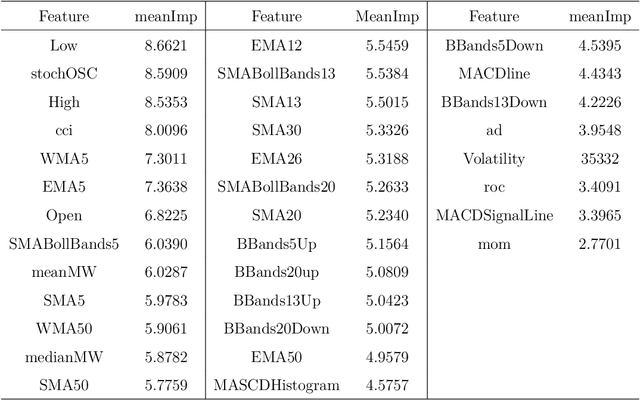

A reliable and accurate forecasting method for crop yields is very important for the farmer, the economy of a country, and the agricultural stakeholders. However, due to weather extremes and uncertainties as a result of increasing climate change, most crop yield forecasting models are not reliable and accurate. In this paper, a hybrid crop yield probability density forecasting method via quantile regression forest and Epanechnikov kernel function (QRF-SJ) is proposed to capture the uncertainties and extremes of weather in crop yield forecasting. By assigning probability to possible crop yield values, probability density forecast gives a complete description of the yield of crops. A case study using the annual crop yield of groundnut and millet in Ghana is presented to illustrate the efficiency and robustness of the proposed technique. The proposed model is able to capture the nonlinearity between crop yield and the weather variables via random forest. The values of prediction interval coverage probability and prediction interval normalized average width for the two crops show that the constructed prediction intervals cover the target values with perfect probability. The probability density curves show that QRF-SJ method has a very high ability to forecast quality prediction intervals with a higher coverage probability. The feature importance gave a score of the importance of each weather variable in building the quantile regression forest model. The farmer and other stakeholders are able to realize the specific weather variable that affect the yield of a selected crop through feature importance. The proposed method and its application on crop yield dataset is the first of its kind in literature.