Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgePrescribing net demand for electricity market clearing

Aug 02, 2021

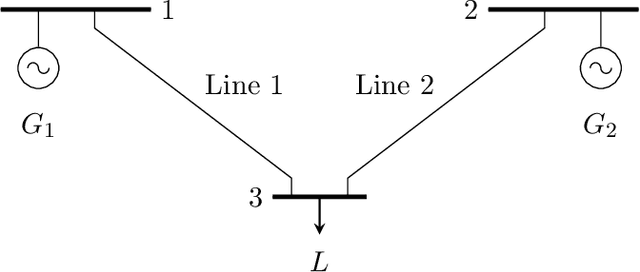

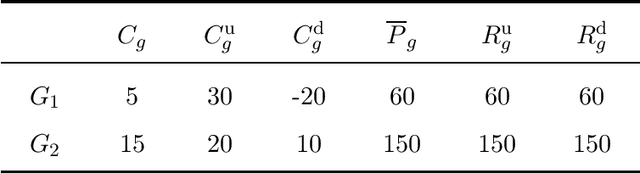

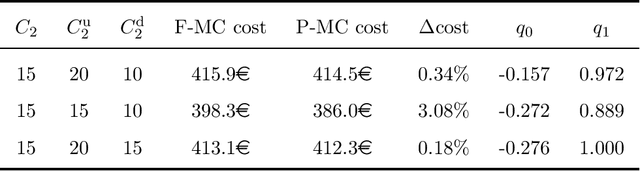

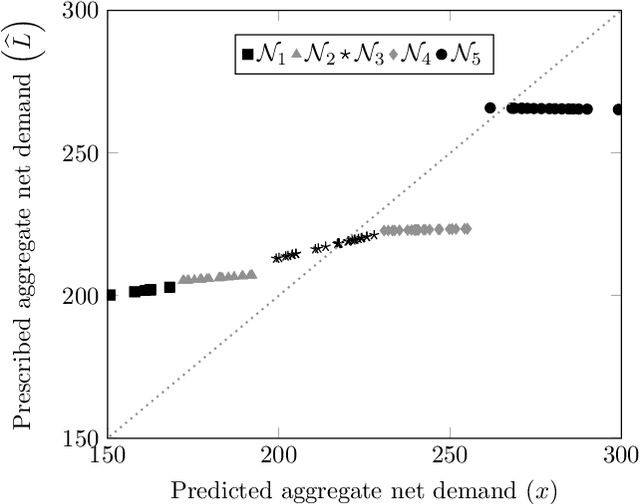

We consider a two-stage electricity market comprising a forward and a real-time settlement. The former pre-dispatches the power system following a least-cost merit order and facing an uncertain net demand, while the latter copes with the plausible deviations with respect to the forward schedule by making use of power regulation during the actual operation of the system. Standard industry practice deals with the uncertain net demand in the forward stage by replacing it with a good estimate of its conditional expectation (usually referred to as a point forecast), so as to minimize the need for power regulation in real time. However, it is well known that the cost structure of a power system is highly asymmetric and dependent on its operating point, with the result that minimizing the amount of power imbalances is not necessarily aligned with minimizing operating costs. In this paper, we propose a mixed-integer program to construct, from the available historical data, an alternative estimate of the net demand that accounts for the power system's cost asymmetry. Furthermore, to accommodate the strong dependence of this cost on the power system's operating point, we use clustering to tailor the proposed estimate to the foreseen net-demand regime. By way of an illustrative example and a more realistic case study based on the European power system, we show that our approach leads to substantial cost savings compared to the customary way of doing.

A novel embedded min-max approach for feature selection in nonlinear Support Vector Machine classification

Apr 22, 2020

In recent years, feature selection has become a challenging problem in several machine learning fields, particularly in classification problems. Support Vector Machine (SVM) is a well-known technique applied in (nonlinear) classification. Various methodologies have been proposed in the literature to select the most relevant features in SVM. Unfortunately, all of them either deal with the feature selection problem in the linear classification setting or propose ad-hoc approaches that are difficult to implement in practice. In contrast, we propose an embedded feature selection method based on a min-max optimization problem, where a trade-off between model complexity and classification accuracy is sought. By leveraging duality theory, we equivalently reformulate the min-max problem and solve it without further ado using off-the-shelf software for nonlinear optimization. The efficiency and usefulness of our approach are tested on several benchmark data sets in terms of accuracy, number of selected features and interpretability.

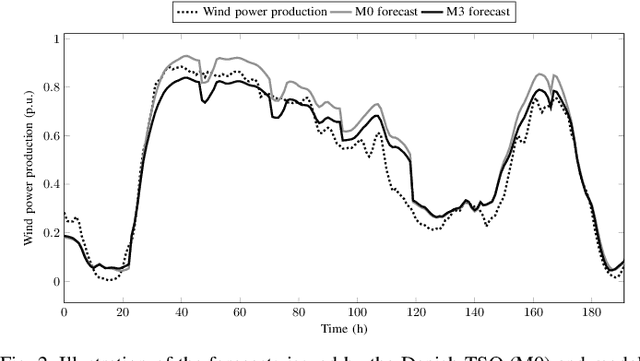

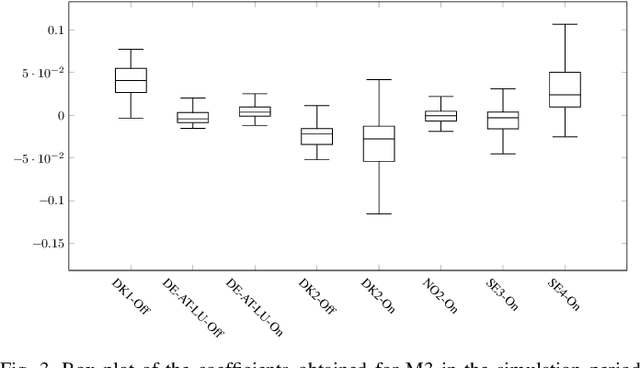

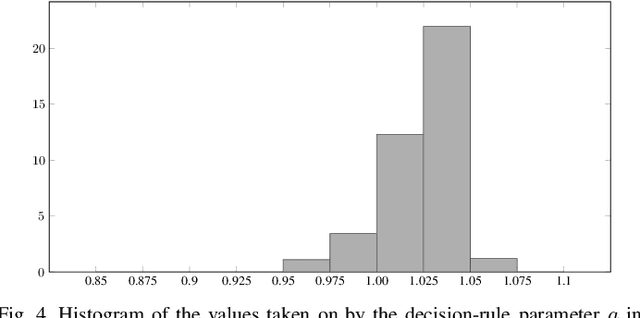

Feature-driven Improvement of Renewable Energy Forecasting and Trading

Jul 17, 2019

Inspired from recent insights into the common ground of machine learning, optimization and decision-making, this paper proposes an easy-to-implement, but effective procedure to enhance both the quality of renewable energy forecasts and the competitive edge of renewable energy producers in electricity markets with a dual-price settlement of imbalances. The quality and economic gains brought by the proposed procedure essentially stem from the utilization of valuable predictors (also known as features) in a data-driven newsvendor model that renders a computationally inexpensive linear program. We illustrate the proposed procedure and numerically assess its benefits on a realistic case study that considers the aggregate wind power production in the Danish DK1 bidding zone as the variable to be predicted and traded. Within this context, our procedure leverages, among others, spatial information in the form of wind power forecasts issued by transmission system operators (TSO) in surrounding bidding zones and publicly available in online platforms. We show that our method is able to improve the quality of the wind power forecast issued by the Danish TSO by several percentage points (when measured in terms of the mean absolute or the root mean square error) and to significantly reduce the balancing costs incurred by the wind power producer.