Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeEvolutionary Optimization for Decision Making under Uncertainty

Jan 19, 2014

Optimizing decision problems under uncertainty can be done using a variety of solution methods. Soft computing and heuristic approaches tend to be powerful for solving such problems. In this overview article, we survey Evolutionary Optimization techniques to solve Stochastic Programming problems - both for the single-stage and multi-stage case.

* Keynote talk at the MENDEL 2011

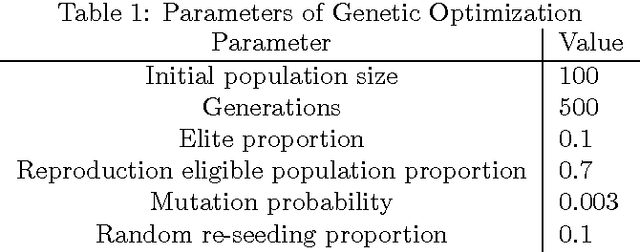

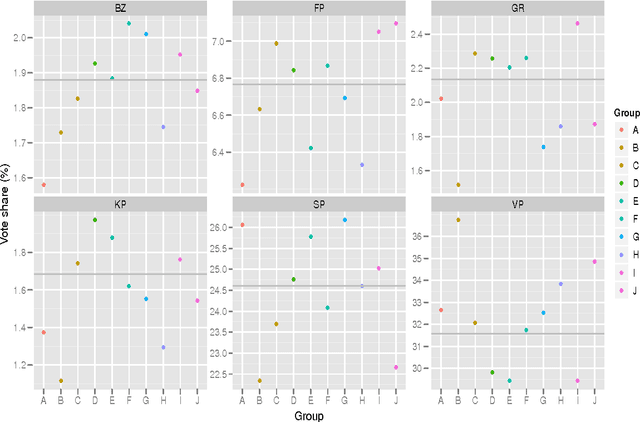

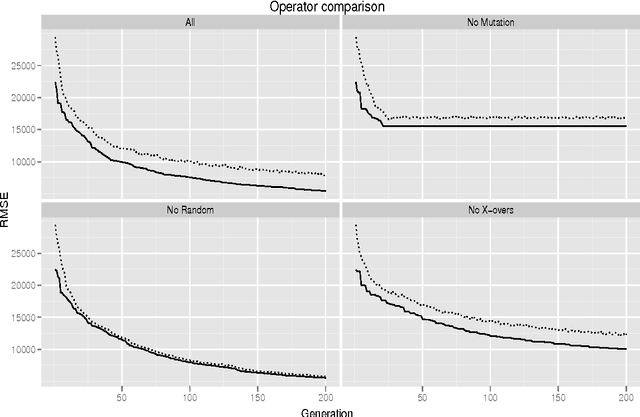

Evolving Accuracy: A Genetic Algorithm to Improve Election Night Forecasts

Jan 19, 2014

In this paper, we apply genetic algorithms to the field of electoral studies. Forecasting election results is one of the most exciting and demanding tasks in the area of market research, especially due to the fact that decisions have to be made within seconds on live television. We show that the proposed method outperforms currently applied approaches and thereby provide an argument to tighten the intersection between computer science and social science, especially political science, further. We scrutinize the performance of our algorithm's runtime behavior to evaluate its applicability in the field. Numerical results with real data from a local election in the Austrian province of Styria from 2010 substantiate the applicability of the proposed approach.

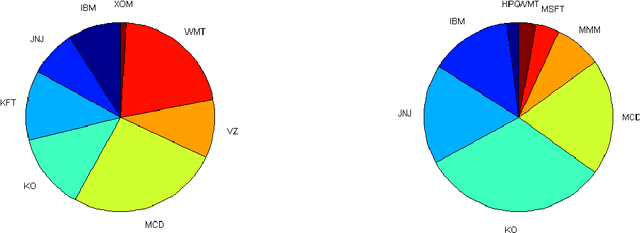

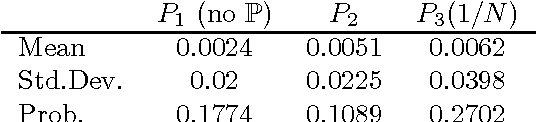

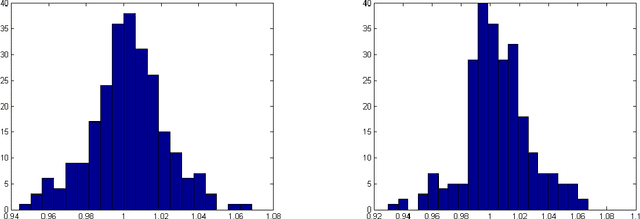

A note on evolutionary stochastic portfolio optimization and probabilistic constraints

Jan 29, 2010

In this note, we extend an evolutionary stochastic portfolio optimization framework to include probabilistic constraints. Both the stochastic programming-based modeling environment as well as the evolutionary optimization environment are ideally suited for an integration of various types of probabilistic constraints. We show an approach on how to integrate these constraints. Numerical results using recent financial data substantiate the applicability of the presented approach.

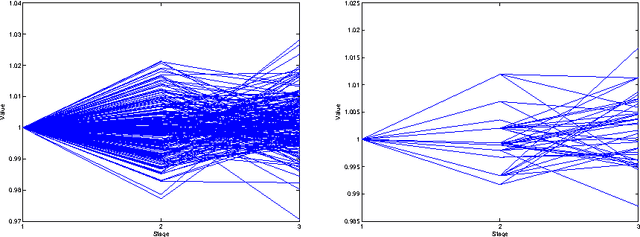

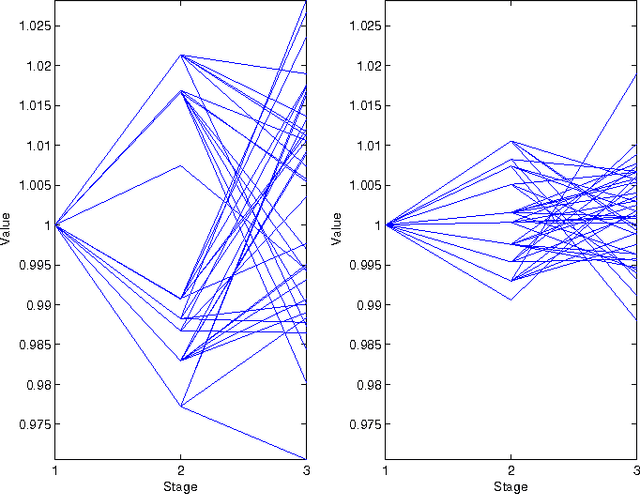

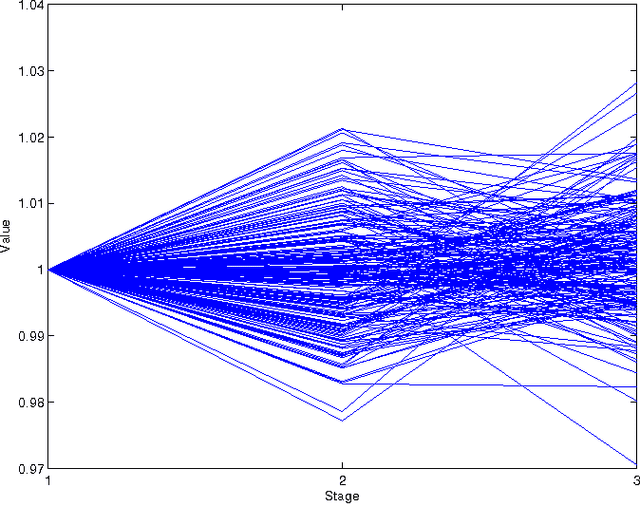

Evolutionary multi-stage financial scenario tree generation

Jan 18, 2010

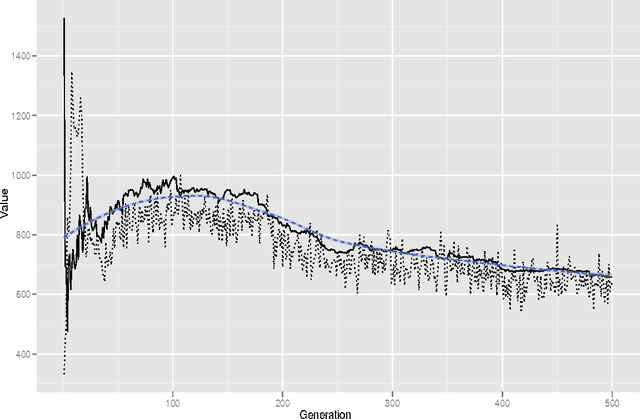

Multi-stage financial decision optimization under uncertainty depends on a careful numerical approximation of the underlying stochastic process, which describes the future returns of the selected assets or asset categories. Various approaches towards an optimal generation of discrete-time, discrete-state approximations (represented as scenario trees) have been suggested in the literature. In this paper, a new evolutionary algorithm to create scenario trees for multi-stage financial optimization models will be presented. Numerical results and implementation details conclude the paper.

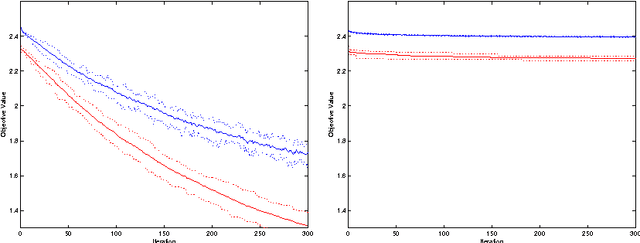

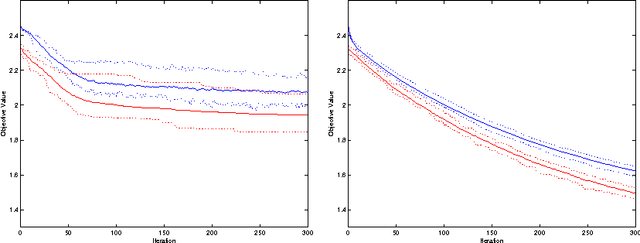

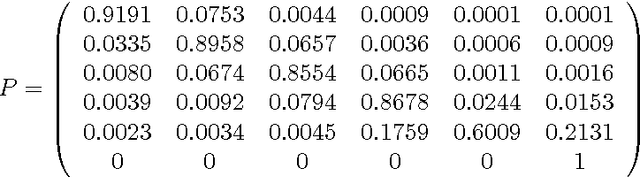

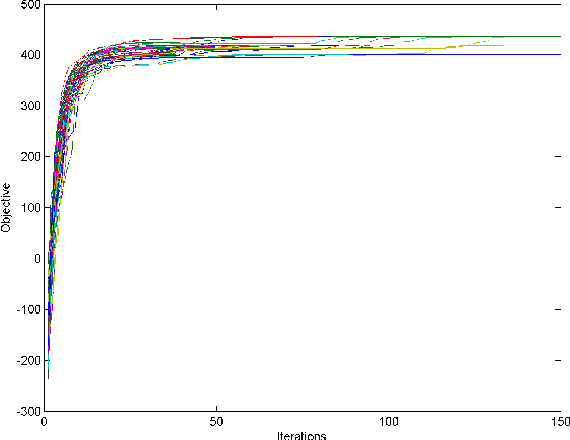

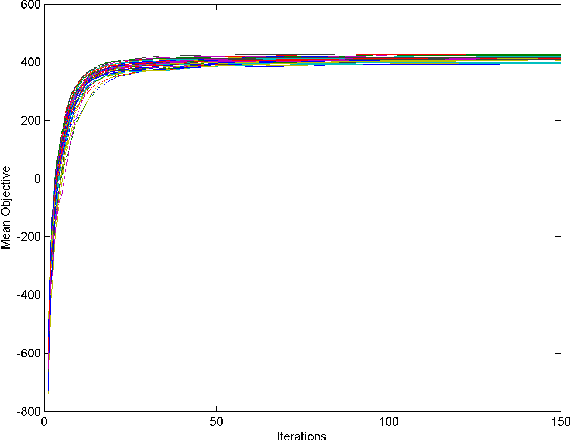

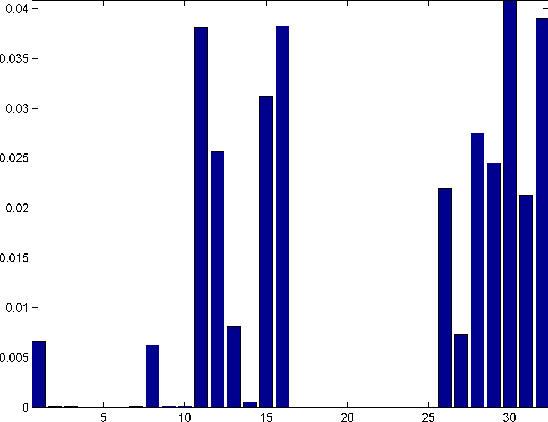

Evolutionary estimation of a Coupled Markov Chain credit risk model

Nov 19, 2009

There exists a range of different models for estimating and simulating credit risk transitions to optimally manage credit risk portfolios and products. In this chapter we present a Coupled Markov Chain approach to model rating transitions and thereby default probabilities of companies. As the likelihood of the model turns out to be a non-convex function of the parameters to be estimated, we apply heuristics to find the ML estimators. To this extent, we outline the model and its likelihood function, and present both a Particle Swarm Optimization algorithm, as well as an Evolutionary Optimization algorithm to maximize the likelihood function. Numerical results are shown which suggest a further application of evolutionary optimization techniques for credit risk management.