Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeImproving Portfolio Optimization Results with Bandit Networks

Oct 05, 2024

In Reinforcement Learning (RL), multi-armed Bandit (MAB) problems have found applications across diverse domains such as recommender systems, healthcare, and finance. Traditional MAB algorithms typically assume stationary reward distributions, which limits their effectiveness in real-world scenarios characterized by non-stationary dynamics. This paper addresses this limitation by introducing and evaluating novel Bandit algorithms designed for non-stationary environments. First, we present the \textit{Adaptive Discounted Thompson Sampling} (ADTS) algorithm, which enhances adaptability through relaxed discounting and sliding window mechanisms to better respond to changes in reward distributions. We then extend this approach to the Portfolio Optimization problem by introducing the \textit{Combinatorial Adaptive Discounted Thompson Sampling} (CADTS) algorithm, which addresses computational challenges within Combinatorial Bandits and improves dynamic asset allocation. Additionally, we propose a novel architecture called Bandit Networks, which integrates the outputs of ADTS and CADTS, thereby mitigating computational limitations in stock selection. Through extensive experiments using real financial market data, we demonstrate the potential of these algorithms and architectures in adapting to dynamic environments and optimizing decision-making processes. For instance, the proposed bandit network instances present superior performance when compared to classic portfolio optimization approaches, such as capital asset pricing model, equal weights, risk parity, and Markovitz, with the best network presenting an out-of-sample Sharpe Ratio 20\% higher than the best performing classical model.

A Methodology for Questionnaire Analysis: Insights through Cluster Analysis of an Investor Competition Data

Feb 09, 2024In this paper, we propose a methodology for the analysis of questionnaire data along with its application on discovering insights from investor data motivated by a day trading competition. The questionnaire includes categorical questions, which are reduced to binary questions, 'yes' or 'no'. The methodology reduces dimensionality by grouping questions and participants with similar responses using clustering analysis. Rule discovery was performed by using a conversion rate metric. Innovative visual representations were proposed to validate the cluster analysis and the relation discovery between questions. When crossing with financial data, additional insights were revealed related to the recognized clusters.

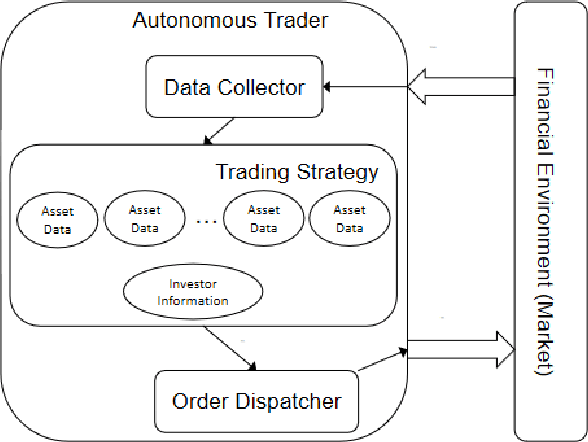

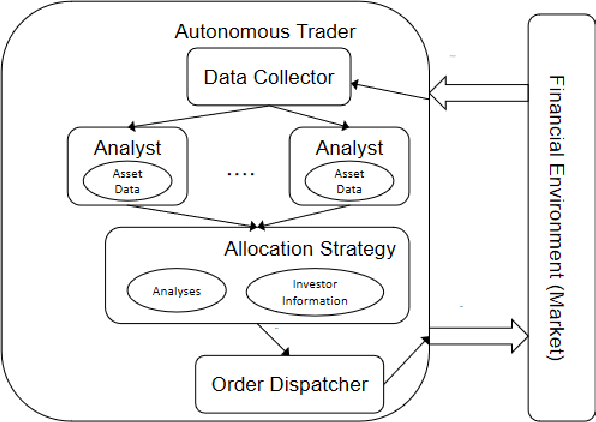

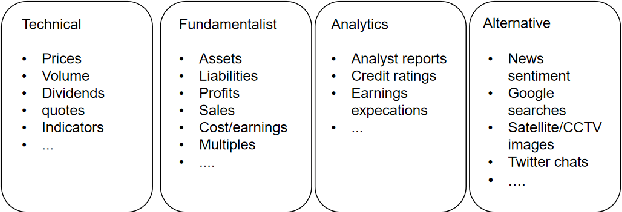

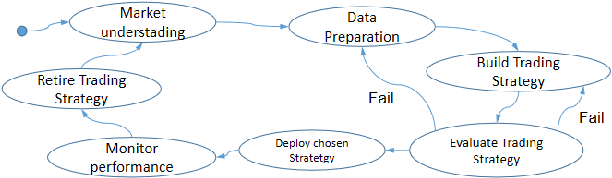

mt5b3: A Framework for Building AutonomousTraders

Jan 20, 2021

Autonomous trading robots have been studied in ar-tificial intelligence area for quite some time. Many AI techniqueshave been tested in finance field including recent approaches likeconvolutional neural networks and deep reinforcement learning.There are many reported cases, where the developers are suc-cessful in creating robots with great performance when executingwith historical price series, so called backtesting. However, whenthese robots are used in real markets or data not used intheir training or evaluation frequently they present very poorperformance in terms of risks and return. In this paper, wediscussed some fundamental aspects of modelling autonomoustraders and the complex environment that is the financialworld. Furthermore, we presented a framework that helps thedevelopment and testing of autonomous traders. It may also beused in real or simulated operation in financial markets. Finally,we discussed some open problems in the area and pointed outsome interesting technologies that may contribute to advancein such task. We believe that mt5b3 may also contribute todevelopment of new autonomous traders.