Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeHigh-Quality Synthetic Financial Time-Series using a GAN-Diffusion Framework

May 26, 2026In recent years, financial institutions and firms have increasingly adopted synthetic data to address data scarcity and to generate counterfactual market scenarios. However, reproducing all the statistical properties of financial time series, commonly known as stylized facts, remains an open challenge for many existing general-purpose architectures. In this paper, we present a quality-aware generative framework that combines two classes of generative methods, demonstrating how their integration addresses existing limitations while enhancing the realism of synthetic data. Specifically, we first introduce CoMeTS-GAN (Correlated Multivariate Time Series GAN), a Conditional Generative Adversarial Network (C-GAN) designed to jointly generate mid-price and volume time-series for correlated stocks. We then show how our GAN architecture can be incorporated into state-of-the-art diffusion models to enhance the quality of generated correlation structures. Specifically, the GAN's Critic serves as a quality evaluation module that guides the diffusion process, enforcing learned correlation structures in the generated time-series. Our framework offers a lightweight and responsive solution for realistic stock market simulation, explicitly modeling inter-asset correlation structures. We experimentally validate our framework against leading generative architectures, showing that it more effectively captures the stylized facts of stock markets and models inter-asset correlations.

Robust Causal Discovery in Real-World Time Series with Power-Laws

Jul 16, 2025Exploring causal relationships in stochastic time series is a challenging yet crucial task with a vast range of applications, including finance, economics, neuroscience, and climate science. Many algorithms for Causal Discovery (CD) have been proposed, but they often exhibit a high sensitivity to noise, resulting in misleading causal inferences when applied to real data. In this paper, we observe that the frequency spectra of typical real-world time series follow a power-law distribution, notably due to an inherent self-organizing behavior. Leveraging this insight, we build a robust CD method based on the extraction of power -law spectral features that amplify genuine causal signals. Our method consistently outperforms state-of-the-art alternatives on both synthetic benchmarks and real-world datasets with known causal structures, demonstrating its robustness and practical relevance.

Towards Realistic Market Simulations: a Generative Adversarial Networks Approach

Oct 25, 2021

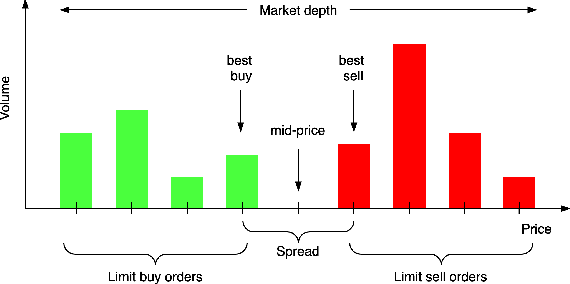

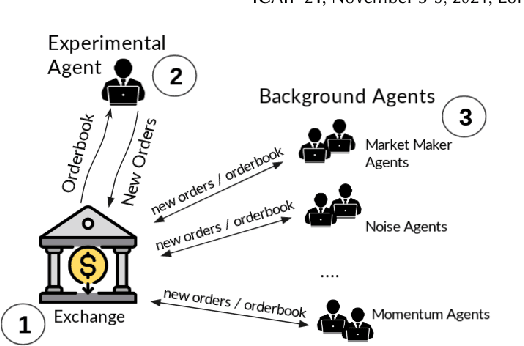

Simulated environments are increasingly used by trading firms and investment banks to evaluate trading strategies before approaching real markets. Backtesting, a widely used approach, consists of simulating experimental strategies while replaying historical market scenarios. Unfortunately, this approach does not capture the market response to the experimental agents' actions. In contrast, multi-agent simulation presents a natural bottom-up approach to emulating agent interaction in financial markets. It allows to set up pools of traders with diverse strategies to mimic the financial market trader population, and test the performance of new experimental strategies. Since individual agent-level historical data is typically proprietary and not available for public use, it is difficult to calibrate multiple market agents to obtain the realism required for testing trading strategies. To addresses this challenge we propose a synthetic market generator based on Conditional Generative Adversarial Networks (CGANs) trained on real aggregate-level historical data. A CGAN-based "world" agent can generate meaningful orders in response to an experimental agent. We integrate our synthetic market generator into ABIDES, an open source simulator of financial markets. By means of extensive simulations we show that our proposal outperforms previous work in terms of stylized facts reflecting market responsiveness and realism.