Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeModeling Chaotic Behavior of Stock Indices Using Intelligent Paradigms

May 05, 2004

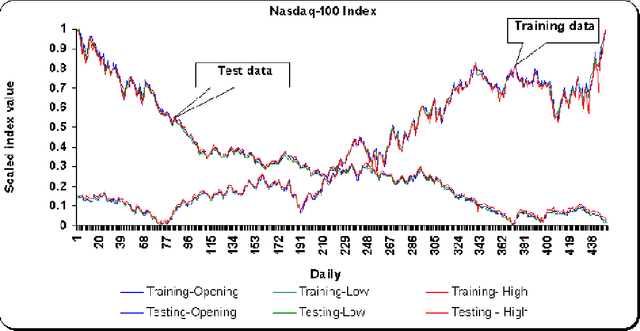

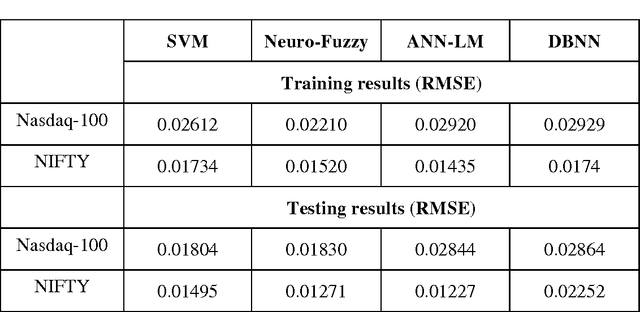

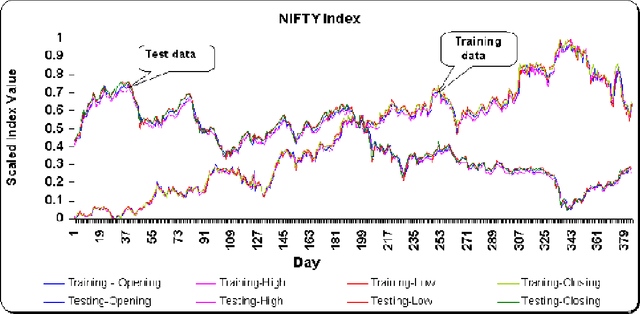

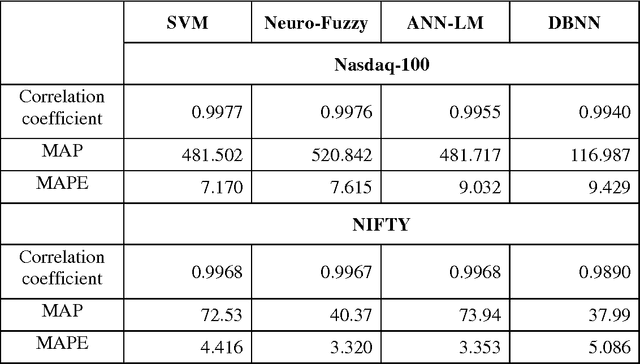

The use of intelligent systems for stock market predictions has been widely established. In this paper, we investigate how the seemingly chaotic behavior of stock markets could be well represented using several connectionist paradigms and soft computing techniques. To demonstrate the different techniques, we considered Nasdaq-100 index of Nasdaq Stock MarketS and the S&P CNX NIFTY stock index. We analyzed 7 year's Nasdaq 100 main index values and 4 year's NIFTY index values. This paper investigates the development of a reliable and efficient technique to model the seemingly chaotic behavior of stock markets. We considered an artificial neural network trained using Levenberg-Marquardt algorithm, Support Vector Machine (SVM), Takagi-Sugeno neuro-fuzzy model and a Difference Boosting Neural Network (DBNN). This paper briefly explains how the different connectionist paradigms could be formulated using different learning methods and then investigates whether they can provide the required level of performance, which are sufficiently good and robust so as to provide a reliable forecast model for stock market indices. Experiment results reveal that all the connectionist paradigms considered could represent the stock indices behavior very accurately.