Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeOn self-play computation of equilibrium in poker

May 23, 2018

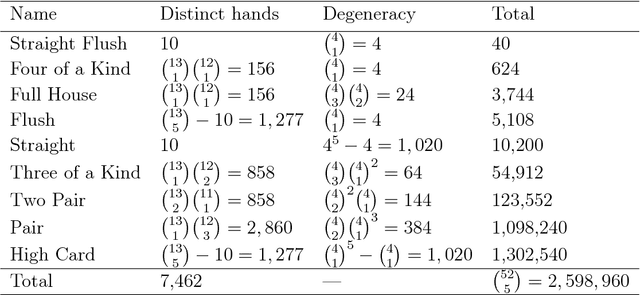

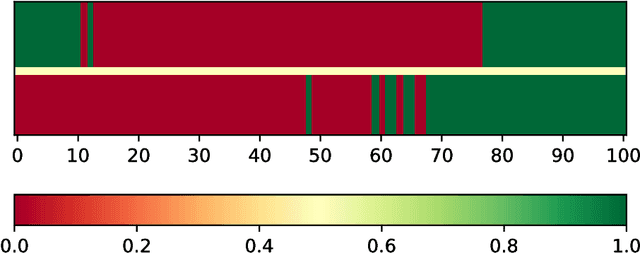

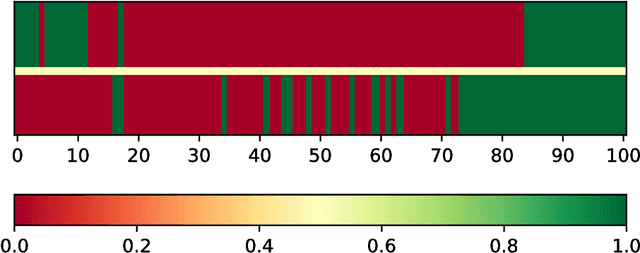

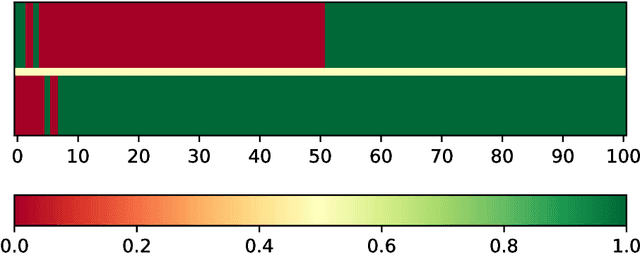

We compare performance of the genetic algorithm and the counterfactual regret minimization algorithm in computing the near-equilibrium strategies in the simplified poker games. We focus on the von Neumann poker and the simplified version of the Texas Hold'Em poker, and test outputs of the considered algorithms against analytical expressions defining the Nash equilibrium strategies. We comment on the performance of the studied algorithms against opponents deviating from equilibrium.

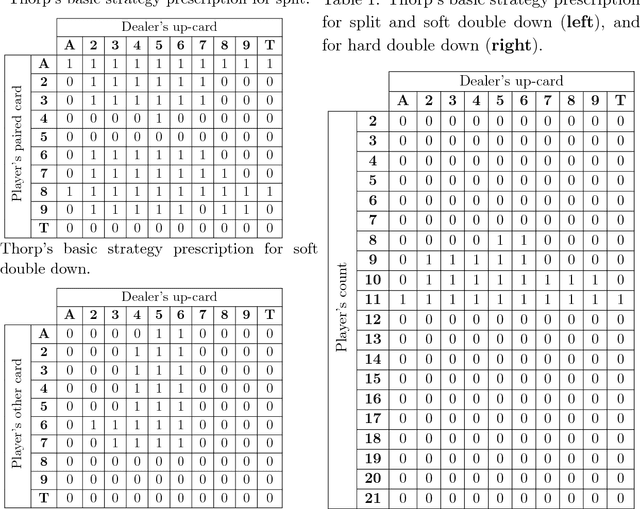

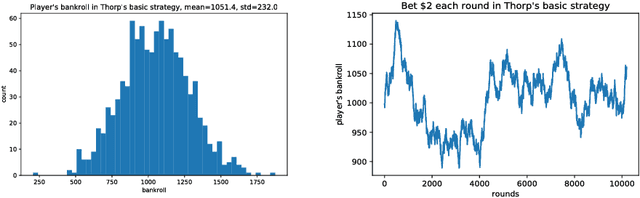

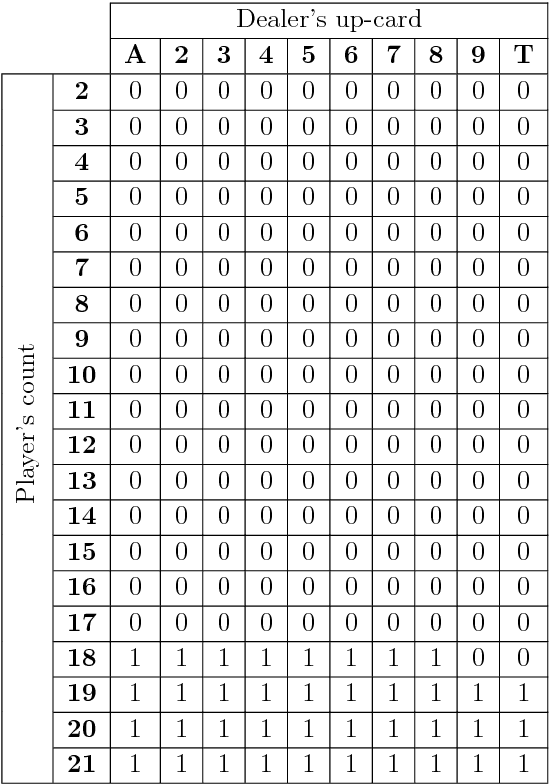

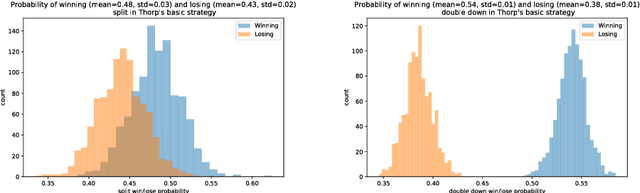

On evolutionary selection of blackjack strategies

Nov 16, 2017

We apply the approach of evolutionary programming to the problem of optimization of the blackjack basic strategy. We demonstrate that the population of initially random blackjack strategies evolves and saturates to a profitable performance in about one hundred generations. The resulting strategy resembles the known blackjack basic strategies in the specifics of its prescriptions, and has a similar performance. We also study evolution of the population of strategies initialized to the Thorp's basic strategy.

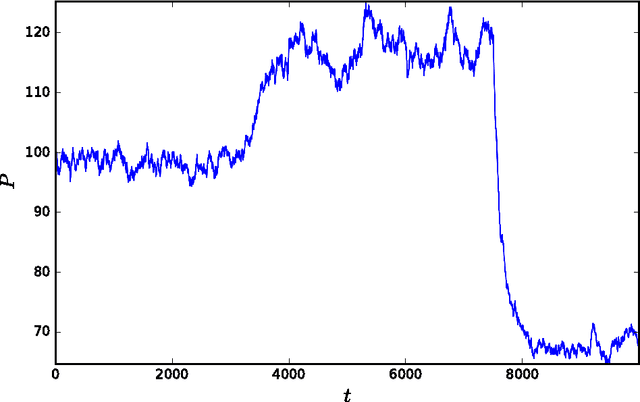

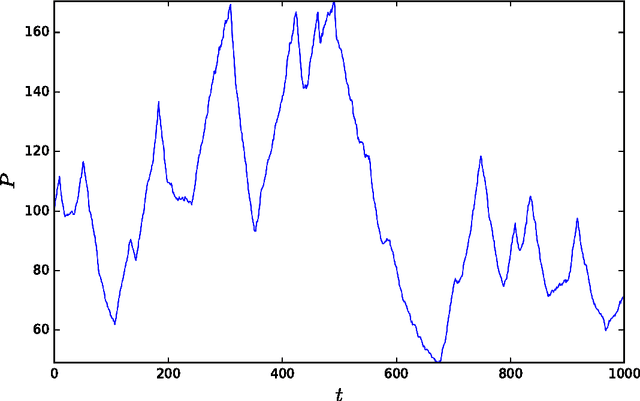

Machine learning in sentiment reconstruction of the simulated stock market

Aug 06, 2017

In this paper we continue the study of the simulated stock market framework defined by the driving sentiment processes. We focus on the market environment driven by the buy/sell trading sentiment process of the Markov chain type. We apply the methodology of the Hidden Markov Models and the Recurrent Neural Networks to reconstruct the transition probabilities matrix of the Markov sentiment process and recover the underlying sentiment states from the observed stock price behavior.