Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeRating Triggers for Collateral-Inclusive XVA via Machine Learning and SDEs on Lie Groups

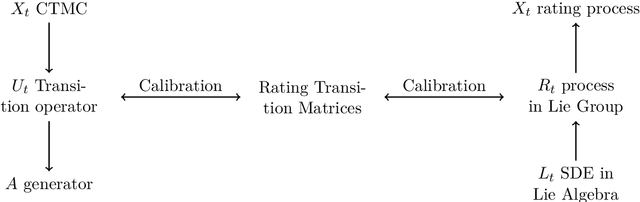

Nov 01, 2022In this paper, we model the rating process of an entity by using a geometrical approach. We model rating transitions as an SDE on a Lie group. Specifically, we focus on calibrating the model to both historical data (rating transition matrices) and market data (CDS quotes) and compare the most popular choices of changes of measure to switch from the historical probability to the risk-neutral one. For this, we show how the classical Girsanov theorem can be applied in the Lie group setting. Moreover, we overcome some of the imperfections of rating matrices published by rating agencies, which are computed with the cohort method, by using a novel Deep Learning approach. This leads to an improvement of the entire scheme and makes the model more robust for applications. We apply our model to compute bilateral credit and debit valuation adjustments of a netting set under a CSA with thresholds depending on ratings of the two parties.

A novel approach to rating transition modelling via Machine Learning and SDEs on Lie groups

May 31, 2022

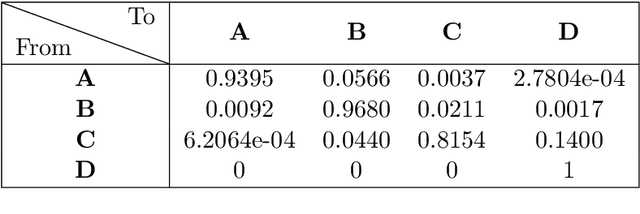

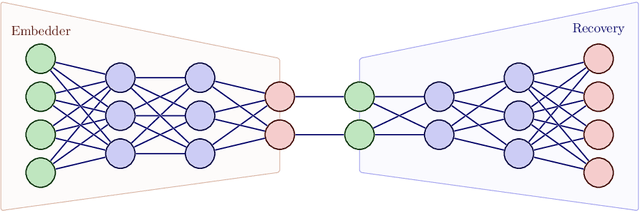

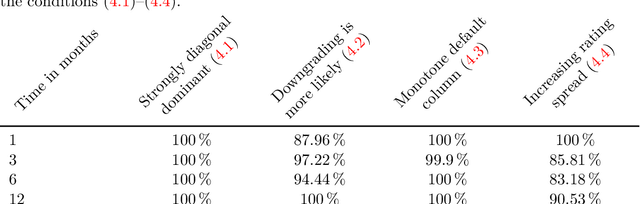

In this paper, we introduce a novel methodology to model rating transitions with a stochastic process. To introduce stochastic processes, whose values are valid rating matrices, we noticed the geometric properties of stochastic matrices and its link to matrix Lie groups. We give a gentle introduction to this topic and demonstrate how It\^o-SDEs in R will generate the desired model for rating transitions. To calibrate the rating model to historical data, we use a Deep-Neural-Network (DNN) called TimeGAN to learn the features of a time series of historical rating matrices. Then, we use this DNN to generate synthetic rating transition matrices. Afterwards, we fit the moments of the generated rating matrices and the rating process at specific time points, which results in a good fit. After calibration, we discuss the quality of the calibrated rating transition process by examining some properties that a time series of rating matrices should satisfy, and we will see that this geometric approach works very well.